YWR: Trying to be more like Australia Dave.

Disclosure: These are personal views, not investment recommendations to buy or sell a security. For investment advice seek professional help.

“Please take a seat sir. Someone will take you up shortly.”

He was standing behind a marble counter in the lobby of One Taikoo Place, Swire’s new flagship tower in Hong Kong. The thick neck, buzzcut and earpiece said I should take his advice.

I walked over to several semi-reclined leather chairs where others were waiting for their hosts. The chairs faced a wall of glass panels looking out over Hong Kong harbour below. The harbour was bustling as usual. I loved the energy of it. I watched the large boats and imagined where they were going with their containers. San Francisco or LA perhaps. I also reflected on why I was here.

It had started with the YWR readers. They were sharp. After all the bullish China posts I’d sent out (The #1 Trade, Surprise Market for 2024) they had messaged me that while they liked the Chinese tech stock idea (Unleash the Cash Dragons), it was a bit tame.

‘China tech is fine, and we’ll buy some, but if this non-consensus China call is going to work shouldn’t we buy something hated which will really move?’

They wanted a China property pick.

So I ran a China property screen to look for a stock which was beaten down (down over 50% from the 5-year highs), trading below 50% of book value (some distress), paying a dividend (some operational cash flows), and with low debt to equity (likely to survive). Out of 100 companies in the screen, Swire Properties (1972 HK) stood out. Big, liquid, 7% dividend yield, and only 15% debt/equity. Plus, I liked their properties and strategy. Which was what I was here to ask Tim about.

*Link to the full China Property screen at the bottom.

But sheesh. Did I really want to own a China property stock? The whole world says its a bad idea.

Then I would painfully remember Australia Dave and the Glimcher Realty Trade. This pain was why I’d forced myself on to a Cathay flight to see Tim Blackburn. I couldn’t bear to make the same mistake again.

I should explain.

First, The Glimcher Realty Trade: From 2013-2016 I’d lived in Scottsdale, AZ. On many weekends my two girls would get invited to birthday parties, which were often held at the Scottsdale Quarter, a high-end outdoor mall. It was a thing for parents to rent out the movie theatre there for birthday parties and watch Frozen (or whatever Disney animation was popular). The mall also had nice stores (Apple, Renovation Hardware) and trendy restaurants with outdoor seating. Overall, it was a popular place.

At these parties I would put on a smiling face for the other parents and do the birthday party thing, but inside I was in anguish. I hated the Scottsdale Quarter. Or more accurately, I hated what it reminded me of; the Glimcher Realty trade.

It was mid-2009 and I was running a global financials book for a hedge fund. We’d swung everything positive, but it felt terrible and we weren’t really sure if it was going to work. It felt like any day the floor was going to drop out and the market would crash again. There were still economic problems everywhere and the consensus view was that while the US economy was stabilising, it would likely double dip and crash again (like in 2008). That was the common sense view, and yet we were buying the riskiest stuff we could find in Europe and the US. It scared the hell out of me, but somehow it seemed right.

The head trader on our desk was Brian, a college quarterback, and former trader at SAC. Nicest guy, but more importantly, he had a nose for connecting the dots in the market and seeing great ideas. He did this intuitively, without spreadsheets or AI. Natural athlete, natural trader.

Now Brian was telling me I needed to take a meeting with a shopping mall company called Glimcher Realty, out of Columbus, OH that was doing a $100mn rights issue.

What??? A shopping mall company in Columbus needs money or they will collapse? And you think we should go in on the deal? Are you nuts? Don’t you know there is a financial crisis going on? Don’t you know it’s going to be an L-shaped recovery and the consumer will be dead for years? Why would I ever waste an hour with these guys, let alone go in on their deal?

But it was Brian, so I took the meeting.

Yes, Glimcher was based in Cleveland and owned a portfolio of 100 uninteresting mid-range shopping malls around the country, but they had an exciting new project. A project, which would soon be finished, in Scottsdale, Arizona. The pitch was that if Glimcher could just raise the $100mn, meet their near-term liquidity needs, and finish the Scottsdale project there was a lot of upside in the shares, which were priced for death. I found myself asking more about the Scottsdale project. I knew Scottsdale relatively well, my in-laws lived there and I visited frequently. I knew the location too.

As the meeting went on, and as I looked at the renderings of what the Scottsdale mall would look like when it was finished, I began to think it could be quite a good mall when it was done. I began to think maybe this wasn’t such a stupid deal after all.

So we went in for the deal, held it for 6 months and made 50%. Seemed good, but Glimcher Realty shares would keep going up for years and years. At one point in 2015 when I was living in Phoenix and couldn’t take it anymore, I checked the share price. Glimcher was +10x from when we’d bought it. The news said investors were particularly excited about their mall in Arizona, the Scottsdale Quarter. Crikey!!!!!

And so that is why it annoyed me so much to go to the Scottsdale Quarter and see how well it was doing.

In hindsight I’d underestimated how much the US economy would recover over time. And while the short-term 50% gain was nice, if I’d been patient I’d have been rewarded with a much bigger trade than I could have imagined.

Then there was Australia Dave: Australia Dave was a tall, good looking guy. He liked to race motorbikes and was married to a wealthy mom from our school. Our daughters were in the same class. Dave would come over in the afternoon to pick up his girls from play dates at my house and he would tell me about his real estate deals. It was 2009 and we both lived in Marin, but during the day Dave would driving out to Stockton to look at vacant homes which were being sold by the banks in bankruptcy auctions.

Every week San Joaquin County would publish a list of house addresses which were going to be auctioned at the courthouse. As soon as the lists came out Dave would drive around Stockton, or Sacramento, or wherever, and visit the properties. There was no-one to show you around, and no key, so Dave would just jump over the fence and look in the windows to get a general idea of the condition of the property. He wanted to see if it needed paint or new appliances. There were more properties than bidders so the deals were good. On the date of the auction you would show up at the courthouse and the auctioneer would go down the list of properties. You would yell out a price you would pay and it was yours.

So Dave was sitting in my living room telling me about these auctions and that I should do it too. And I told him how I thought it seemed risky and what if I couldn’t find people to rent out the properties later. I mean employment in California was 11% and if people didn’t have money for their mortgage maybe they wouldn’t have money for rent either. And I wasn’t good at fixing things up like him. Most likely Dave was going to be stuck with a portfolio of empty, worthless houses in Stockton for a long time.

Well, it didn’t turn out that way. In hindsight, the California property crisis of 2009 was a life changing opportunity….for Dave……

And that is why despite all the expert opinions to the contrary, I am drawn to the world’s biggest property crisis. I know they say there are millions of unsold homes, and it will take years to clear, and I’m sure the math makes sense, but it was the same logic in 2009. Same thing; L-shaped recovery, banks sitting on huge portfolios of properties which would take years to clear. It would be a lost decade. But they never factored in Australia Daves seizing the opportunity.

So this time I’m trying to be less chicken little and more like Australia Dave. It pays better.

Australia Dave would say property crashes are an opportunity. Especially one that has already been going on for 3 years and the government is finally starting to react.

Which was why I was sitting in Hong Kong waiting to see the CEO of one of the largest property companies in HK and China.

***********************************

Tim: ‘Erik! Please sit down. Li is bringing you a coffee. You like it strong with extra milk and sugar. Right? We’ve been reading YWR you see. I have to say, when you first reached out to us it was a surprise. We’ve never had an investor meeting with a Substack blogger, but then we thought ‘Why not?’

YWR readers are the best investors in the world. They’re experienced money makers who think for themselves. They’re exactly who we should be telling our story to. So actually, thank YOU, for coming to visit Swire and letting us tell your readers about our company and why it’s a good investment.

Tim was chatty. And the coffee had arrived. Thankfully.

Erik: Tim, thank you for the kind words. And I should explain more about why I’m here. At YWR we think investing in China right now is the biggest asset allocation decision large global funds can be making. But it’s controversial and understandably hard for portfolio managers with the media and the sell side research so persistently negative. To try and help we’ve been highlighting corporate CEO’s who know China, have operated there for years, and are taking the current downturn as an opportunity to increase their exposure.

For example, in April we met with Robert Goldstein at LVS. I don’t know if you follow LVS, but in 2022 they sold all of their US casinos to a PE firm for $6bn and have been ploughing the money into Macau and Singapore (The China Opportunity according to LVS). And the reason I wanted to speak to you is because I see Swire doing the same thing.

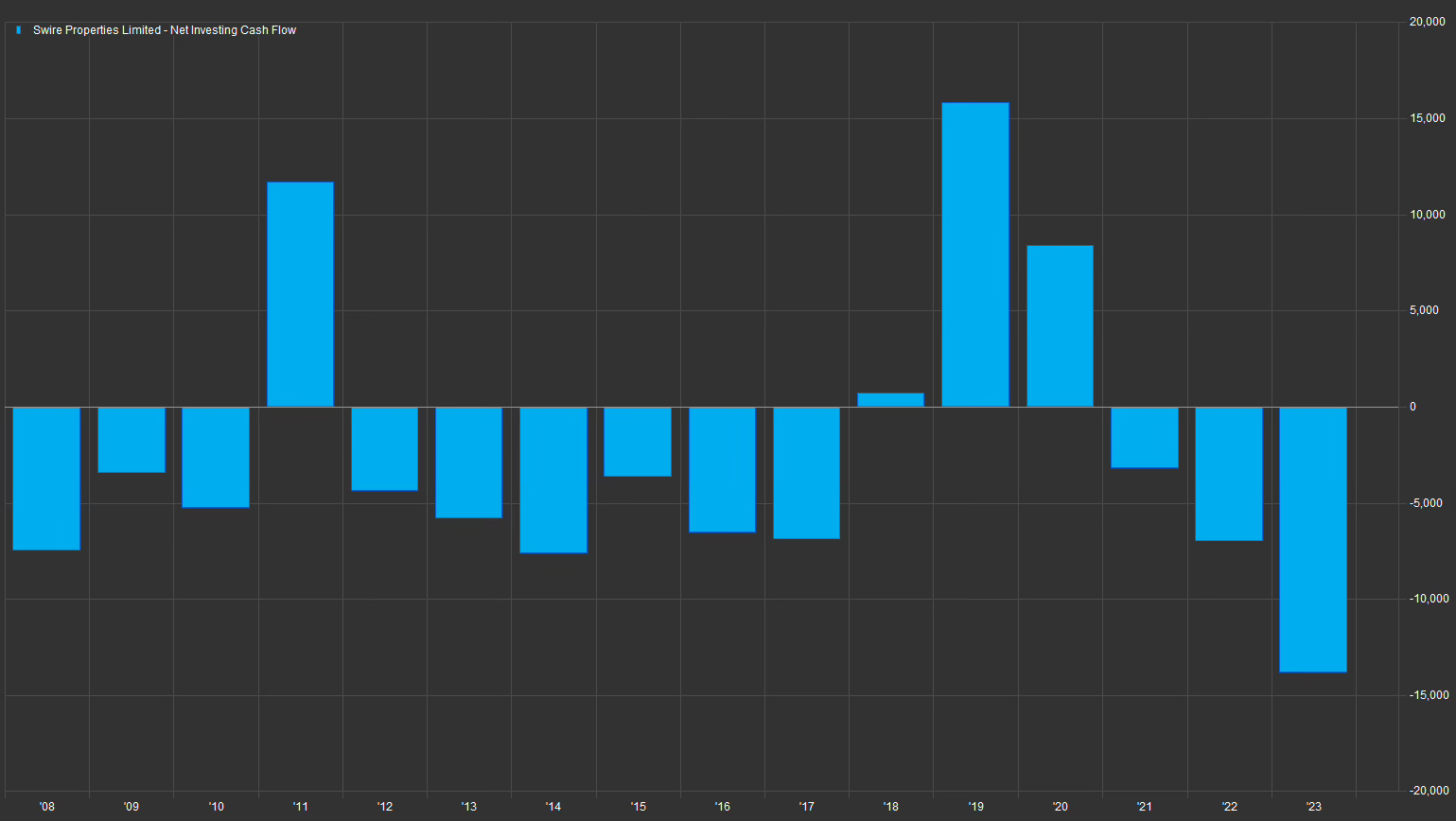

In 2018 and 2019 you were selling off offices in Hong Kong and got super deleveraged. In 2019 you sold Cityplaza towers 3 & 4 for $1.9 billion and got down to 5% debt/equity. That was amazing timing because it was right before COVID. You sold $2bn in Hong Kong offices at peak valuations, got all cashed up, and then sat on the sidelines for 3 years while COVID and Evergrande steamrolled mainland China. Now you get to deploy that money on the lows while your competitors are imploding.

I mean I love it. Everyone is chicken littling while you are aggressively buying up trophy assets across China. Instead of freaking out you are doubling your China exposure. These are bold moves and it sets an example. Australia Dave style! Sorry… That’s another story.

Tim: Well, Erik.. I don’t know why you bothered to fly all the way to Hong Kong, because you seem to know the story well. But I would like to add color on why I think what we are doing at Swire is special and why we feel confident to commit capital when others are fearful. We are very careful about our reputation and what we do. We are a stable, long-term real estate owner, with a good credit rating, who builds premier properties and doesn’t get into trouble. We don’t get over extended on developments and when we do take on developments we execute high-end city changing type projects like Taikoo Li in Chengdu or Pacific Place here in Hong Kong.

Take Taikoo- Li Chengdu for example. We saw an opportunity to transform a run down area around the Daci Temple into a high-end shopping center, intertwined with a complete renovation of the temple. It changed Chengdu.

The result has been amazing. The site is a top tourist attraction. Now other cities have noticed and want one too. For example, we’ve been invited to Xi’an to develop a similar style of project which blends the historic with the new.

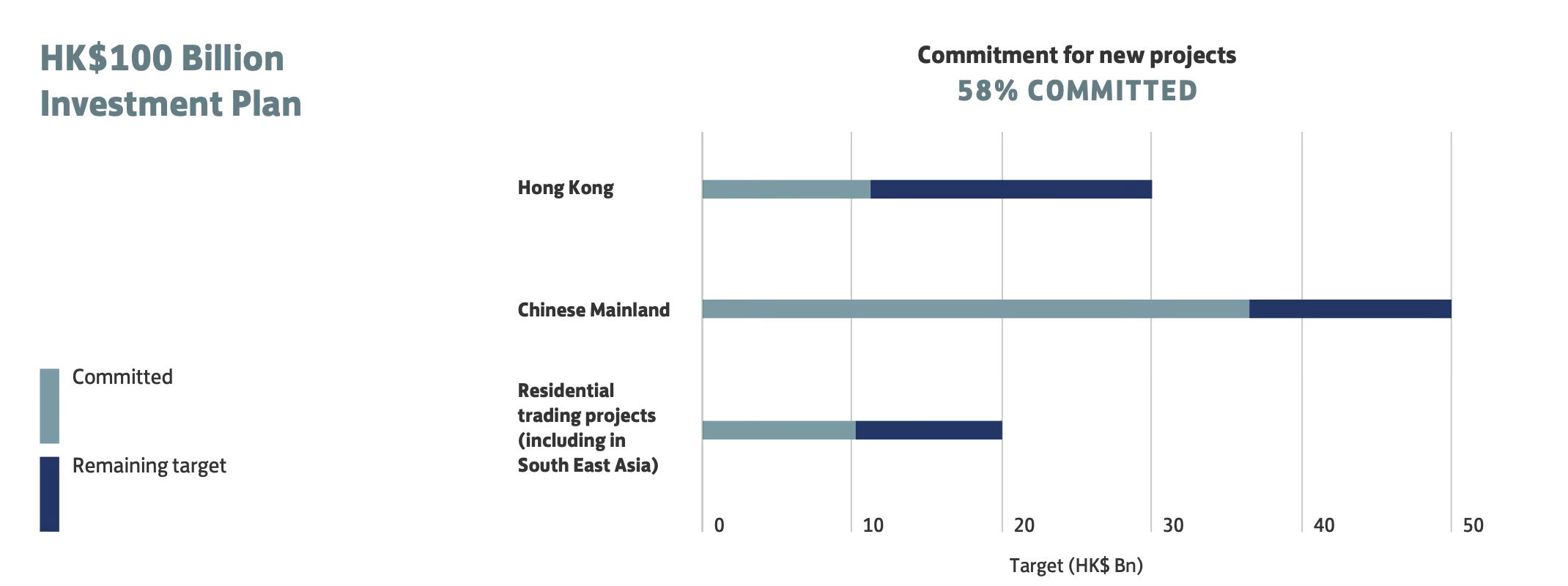

And like you said, we’re taking advantage of the downturn to really accelerate our goal to double Swire’s China exposure. In 2022 we announced a 10 year plan to invest HKD 100bn (US$ 14bn) which included a doubling of our China exposure. It’s only been 2 years and we’ve already committed HKD 58bn of the 100, most of it deals and projects in China.

For example, we bought out the rest of Taikoo Li in Chengdu (now 100% ownership) for RMB 5.5bn and also bought a 40% stake in two trophy developments in Shanghai for RMB 10bn. During the good times it’s impossible to get into Shanghai developments at a reasonable valuation, so he have to take advantage of this window where we have the cash and others don’t. When the two new Shanghai projects are complete it will be our biggest area of operations in China.

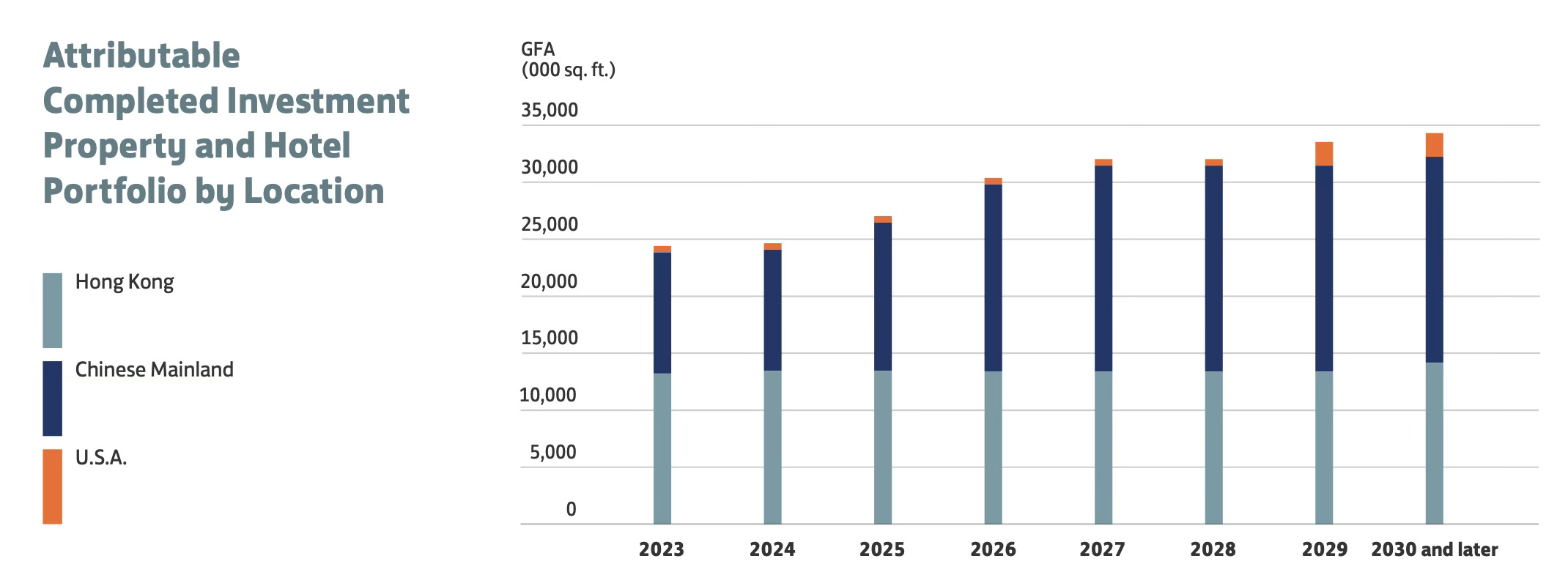

But the main point for your readers to realise is we’re building hard-to-execute, highly valuable, city-changing, trophy properties that hold their value with low vacancy rates. We are building luxury malls in the best cities in China and the world’s top luxury brands are lined up to take space. We aren’t a fly by night operation throwing up 2 bedroom apartments across China. We very little debt and a rock solid existing portfolio of 24mn GFA with occupancy in the high 90’s across all established assets.

We will fund the HKD $100bn of investments organically over time using our substantial debt capacity, free cash flow, and some asset sales.

Erik: Tim… that’s super helpful. Thank you. I’ve taken up too much of your time and should be going. I’ll make sure you to email you the post when I get back to London and write everything up. And thank Li for the coffee. It was just how I like it.

Tim: Oh, one more thing. Please tell Mrs. YWR we paid a 2023 dividend of HK 1.05/share (7% yield) and in the past 20 years we’ve only skipped a dividend once; 2009. Our guidance is to grow the dividend a mid-single digit % every year. We’d be honoured if she’d consider us for her Dirty Dividends portfolio. We’re aren’t going to buyback shares though. We want to keep investing in our projects.

Erik: Will do Tim. Thank you again!

Tim: And you know what else? Buy the shares and in 2027 you can visit Taikoo Li in Xi’an for the opening and not hate yourself for missing the China rally.

!!!!Disclosure alert. This interview involves artistic license and did not officially happen!!!

*****************************

Below is a link to the full China property screen with over 100 companies with listings in Hong Kong.

I thought Swire looked good, but maybe you see something more interesting.