YWR: Unleash the Cash Dragons!

Disclosure: These are personal views. They are not investment recommendations to buy or sell a security. For investment advice seek professional help.

In 2022 YWR brought you a controversial new investing theme.

A theme so controversial many said it shouldn’t be done.

Professional investors saw the genius of it, but feared they would lose their jobs following such a bold strategy.

It was a portfolio constructed from the 5 most unloved sectors in the market trading at the lowest valuations in their history.

5 sectors with no future.

5 sectors hated so much we labeled them ‘The Untouchables’:

European Banks

Autos

Mining

Big Energy

Tobacco

In 2022 we brought these sectors together to form a strategy we called The Dirty Dividends.

That was 2022. The rest is history.

Today Dirty Dividends is a household name with families across the US replicating it for themselves in their brokerage accounts.

Now in 2024 we’re doing it again.

YWR in collaboration with StirlingAI | Cracking the Code is bringing you a new theme.

A theme which once again tests the boundaries of what is safe, and acceptable.

A theme which once again no professional money manager would ever recommend. But should.

A theme comprised of 7 stocks sure to make you uncomfortable every time you look at them. But shouldn’t.

7 large, liquid ‘uninvestable’ stocks full of cutting edge technology and cashflows trading at historically low valuations.

It’s a set up which rarely happens in large cap tech stocks. And when it does we need to take advantage of it.

Stirling AI & YWR present to you:

Edmund… please take it away. This is your creation.

Introduce them to the Dragon7.

YWR is one of my favorite blogs.

So, I am thrilled to team up with Erik for a joint post on the Dragon7 companies:

Roaring Dragons

Understanding the Dragon7 companies is not difficult. Neither are they too different from familiar tech companies in the US.

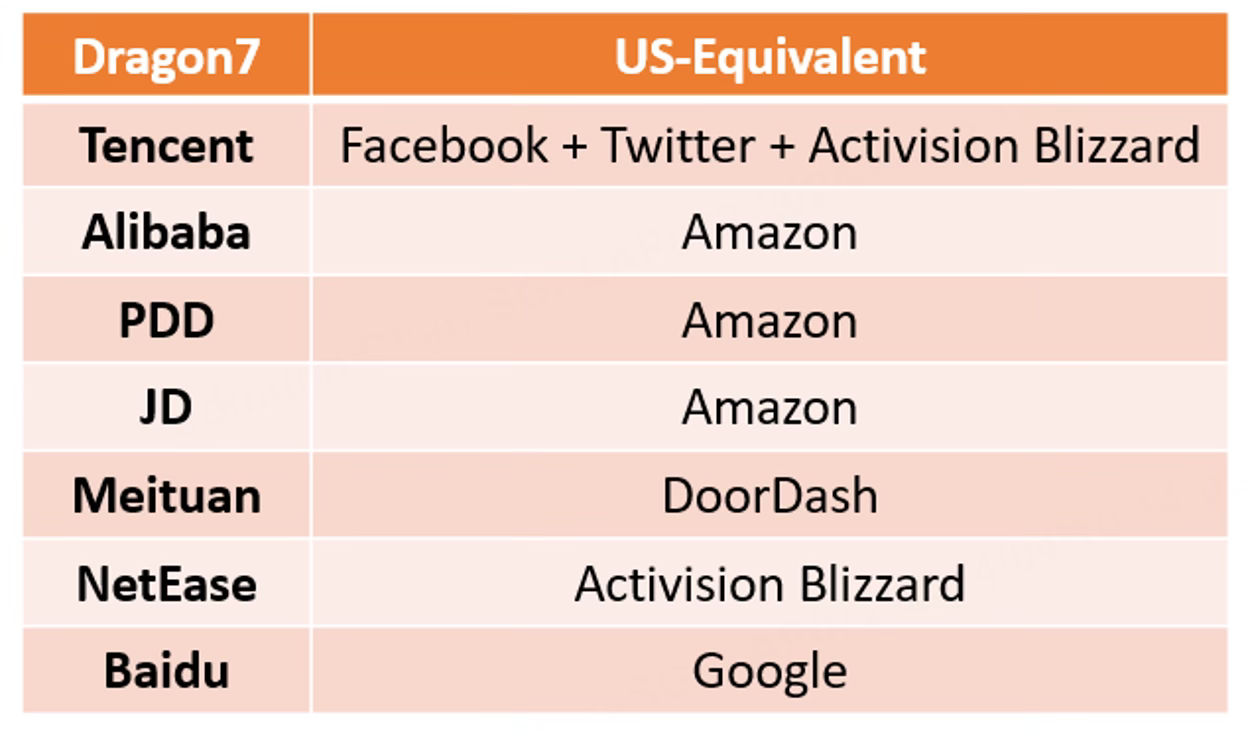

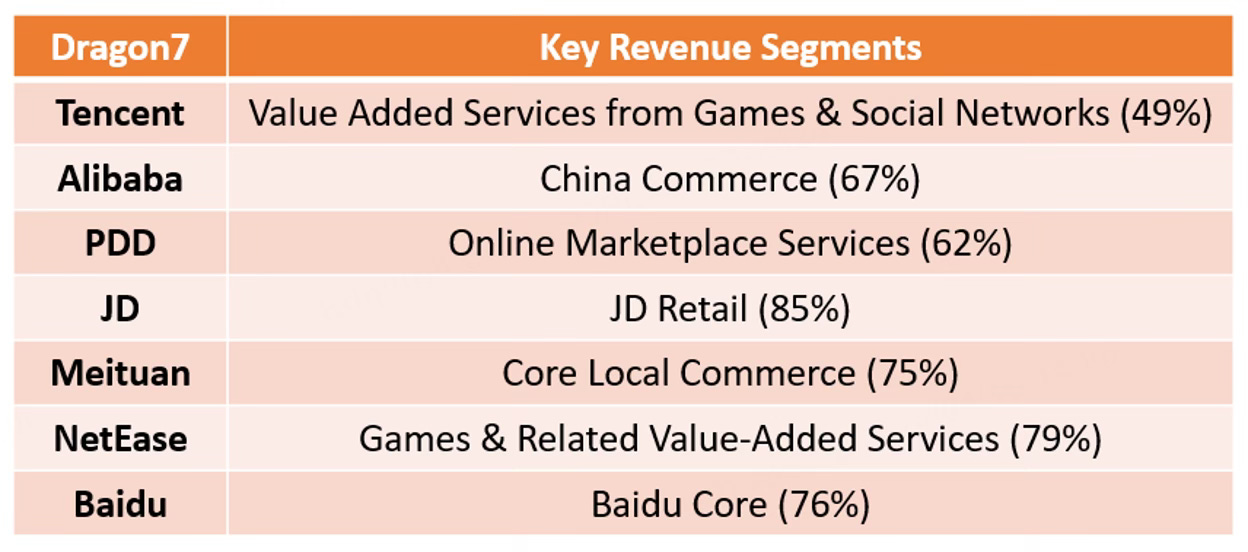

Leading the Dragon7 pack is Tencent, a behemoth with a staggering $380 billion market cap. It is the equivalent of Facebook + Twitter + Activision Blizzard combined. In China, Tencent's WeChat is ubiquitous with over 1.3 billion monthly active users. Functioning as a Super App, WeChat integrates third-party features such as photo filters and payments, all in one app.

Sorry to interrupt Ed…

But I’d like to add ‘Visa’ as another western equivalent to Tencent. Those 1.3 BILLION WeChat users also use the app to make payments. Think WhatsApp with payments.

Back to you.

The next largest Dragon7 is Alibaba, with a $190 billion market cap. Just as Alibaba is the 'Amazon' of China, its founder, Jack Ma, is the ‘Jeff Bezos’ of China. Incidentally, both Jack and Jeff are among the richest internet tycoons in their respective countries. Alibaba's platforms, Taobao and Tmall, are household names, amassing an annual GMV exceeding $1.1 trillion.

Following closely in the Chinese e-commerce market are PDD and JD with a market cap of $161 billion and $42 billion respectively. For a long time, JD has been the second-largest e-commerce company, with its leadership in electronic goods and warehouse solutions. However, PDD's innovative team purchase model has propelled it ahead, and the company is even challenging Amazon in the US with its Temu app.

With a market cap of $83 billion, Meituan is also recognized as an e-commerce company but it is more like the DoorDash of the US. Its main focus is the food delivery business, in-store hotel & travel business. The company operates mobile apps including Meituan Dianping and Meituan Waimai.

Beyond these e-commerce companies, NetEase is the next biggest Dragon with a $63 billion market cap. As a powerhouse in online gaming, the company ranks behind Tencent. Its core games include hit titles such as Fantasy Westward Journey, and Ghost.

Last but not least, Baidu is the 'Google' of China, with a $36 billion market cap. The company is the leading cloud and AI company in China. Its Ernie Bot is the equivalent of “ChatGPT” in China.

Together, these Dragon7 companies are the internet tech giants of China.

Cash Dragons

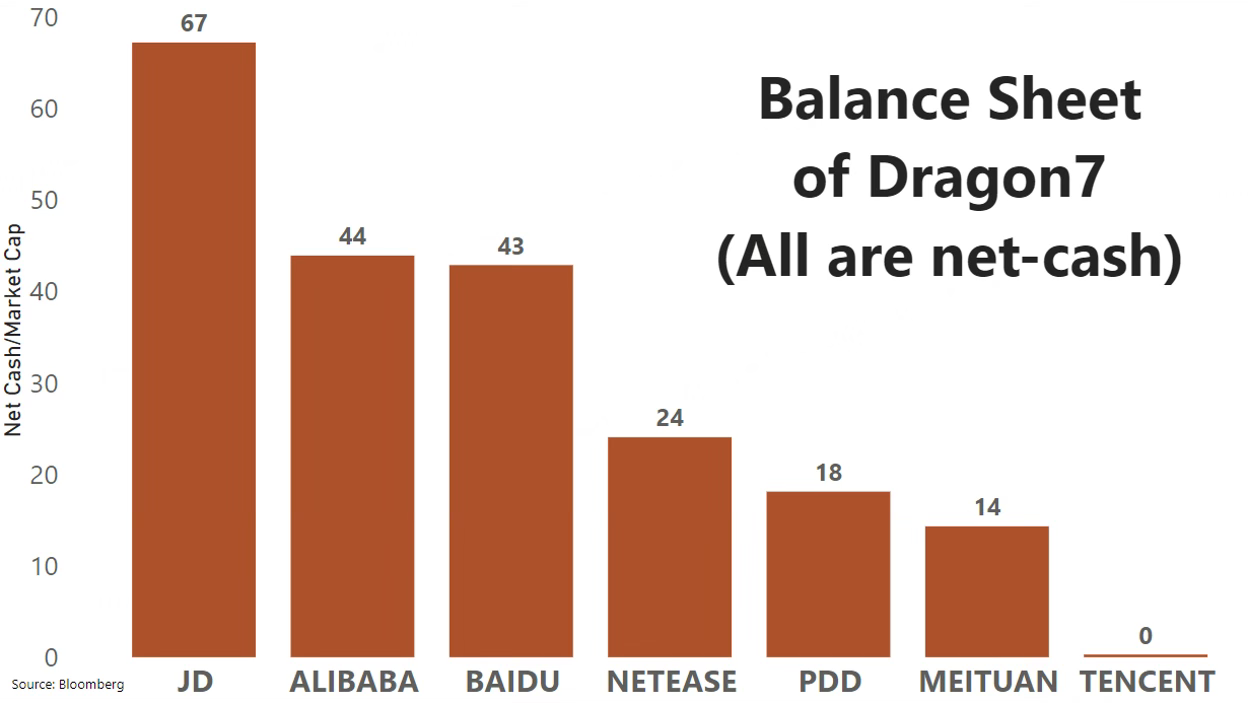

The Dragon 7 companies are a cash oasis, in stark contrast to the levered property sector.

They are sitting on a cash mountain of $204 billion, nearly a third of their total market cap of $955 billion. JD leads the pack with net cash holdings equivalent to about 67% of its market value.

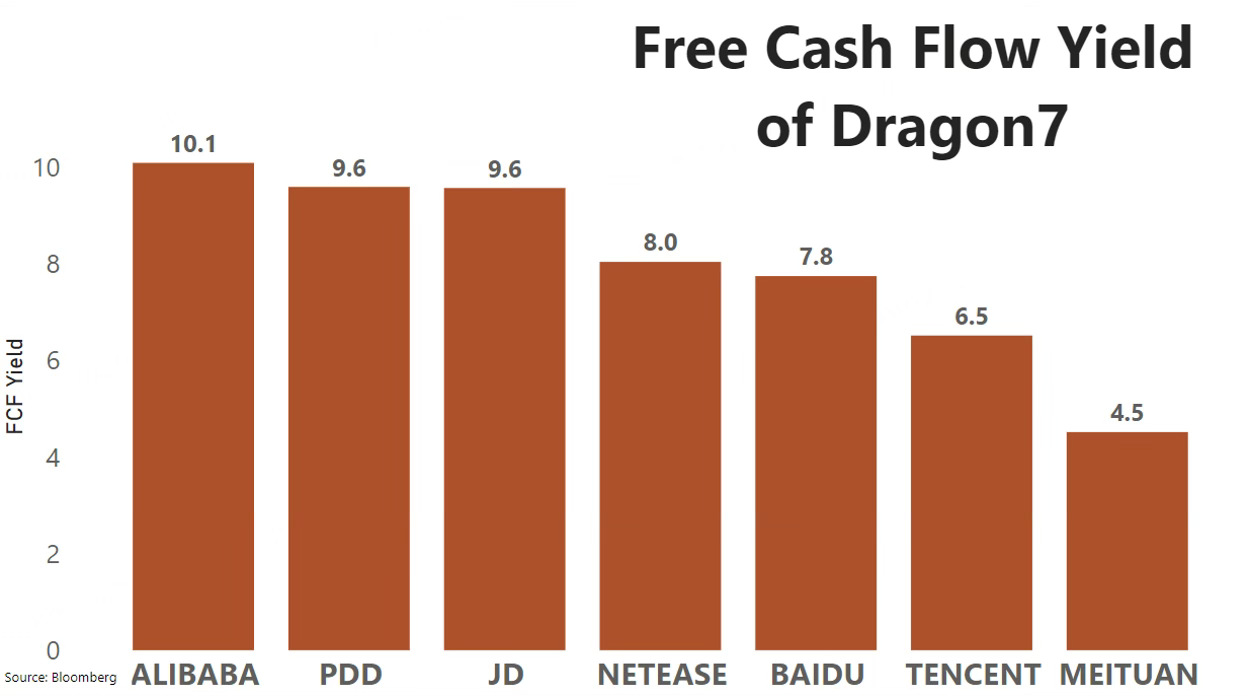

Not only are these companies flush with cash, but they're also raking in cash. On average, their free cash flow yields stand at 8.0%, with Alibaba topping the charts at an impressive 10.1%.

As a vote of confidence, these companies are increasing their share buybacks. Alibaba, for instance, ncreased their share buyback by an additional $25 billion (for a total authorised of US$ 35bn over next 3 years), while Tencent doubled its buyback for 2024 to HK$100 billion (US$12 billion). Baidu has a $5 billion buyback with $4.3 billion remaining. JD.com announced an additional $3bn buyback with their Q4 results on top of the $1.5bn remaining on the existing plan (so $4.5bn over next 3 years).

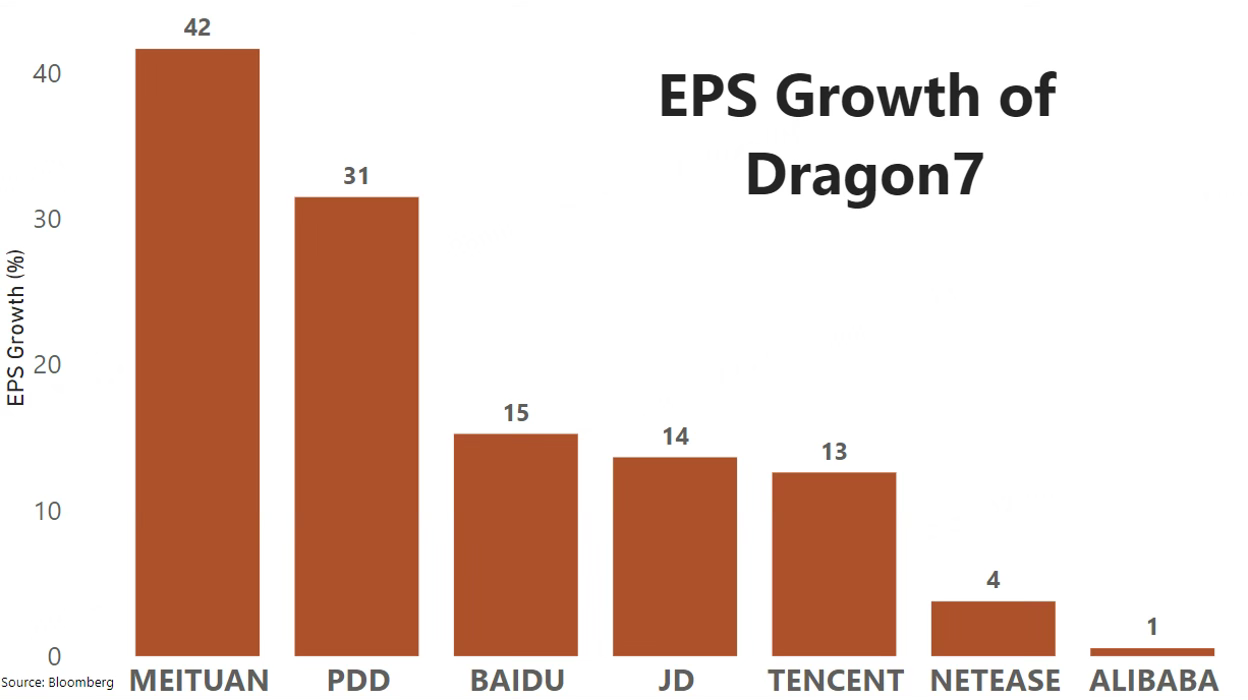

Furthermore, these companies are trading at a modest 12.9x P/E, in spite of a robust 17% EPS growth projected for FY2024,This represents a bargain valuation at just 0.7x PEG. Alibaba stands out with the lowest P/E of 8.6x, while Meituan boasts the highest expected EPS growth of 42%.

With such a compelling valuation and robust balance sheet, investing in the Dragon7 companies offers limited downside risk and presents an attractive opportunity for investors.

Generational Dragons

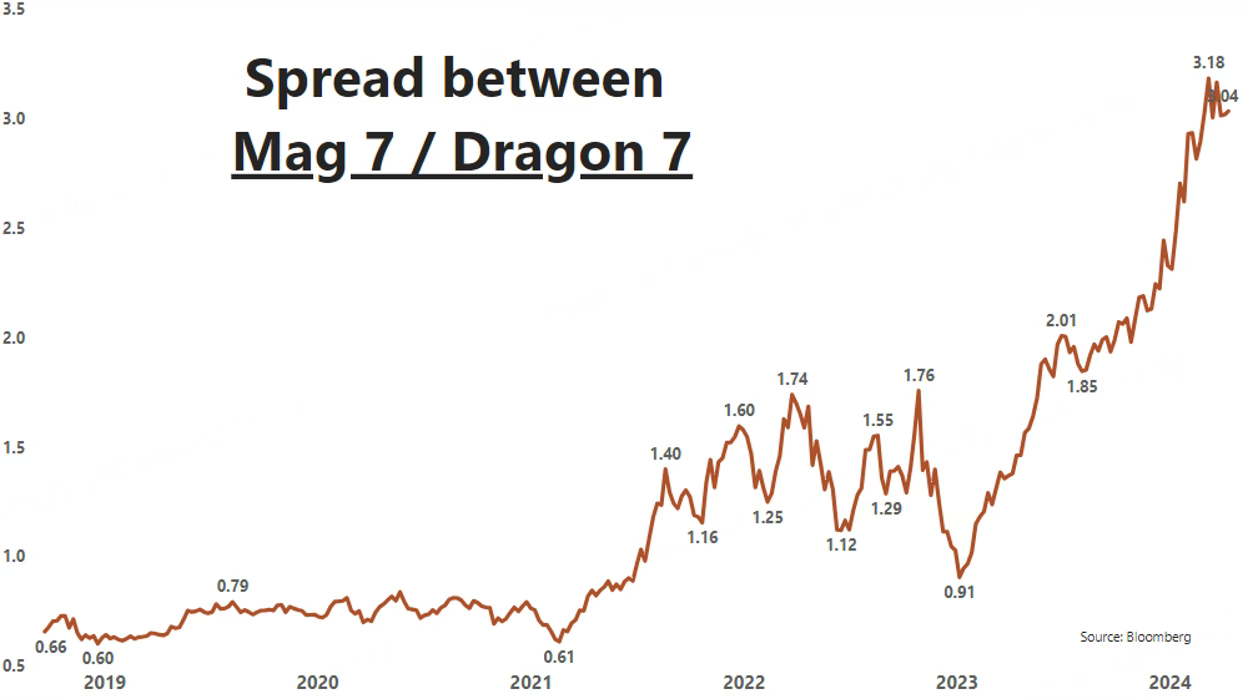

Back on February 13th, I introduced the idea of a generational pair trade between the Magnificent 7 and Dragon 7 stocks. At that time, the difference between the two groups was at a multi-year high of 2.89.

Since then, this gap widened even further, reaching a peak of 3.18 before settling back to 3.04 currently.

Nevertheless, with strengthening fundamentals, this pair trade still looks promising for investors and could be a rare opportunity that comes once in a generation.

Wow Ed…. Thank you! Great work. Great charts. Great theme.

And I love the contrarian thinking. It fits our Surprise Market for 2024 theme.

Our Mega-Fund readers will appreciate that this is a multi-year theme in big, liquid stocks where they can get massive and don’t have to trade it. They can just let it compound.

Like with Dirty Dividends YWR will help us along the journey with earnings models to track results and make estimates. As well as deeper dives into the Dragon7 to further appreciate the businesses these companies are building which will keep us in the trade.

Below are my models for Tencent and Baidu. I previously owned Tencent and bought some Baidu too. I will add more models as they become available.

Disclosure: These are not sell side models. They are meant to be easy to update and a way to track earnings vs expectations, make estimates and generate price targets. You are welcome to download them and add whatever extra segmental or WACC analysis you want.

| A guest post by

|