YWR: Untouchable #7

Disclosure: These are personal views and investment commentary. This is not investment guidance or advice. For that seek professional advice.

************************

Erik: Hey babe! I’m home. Dinner smells good! What’re you cooking?

Hi Roosevelt…yes, you’re soo cute….yes you are!!

Is that my favorite.. are you making spaghetti and meatballs?

Can I help? Do you want me to do something?

Coley: Hi. Welcome home. Yes, it’s spaghetti and meatballs, but don’t touch anything. If you have to do something stir the sauce. Here’s a glass of wine.

So, how did my Dirty Dividend portfolio do today?

Erik: ‘Your’ Dirty Dividend Portfolio?

Coley: Yes, my Dirty Dividend Portfolio. It was my idea. You are the analyst.

Erik: Hmmmm… well it was up a bit and the dividends came in from Glencore and Barclays. We reinvested the dividends into more Glencore, Mercedes and the European banks.

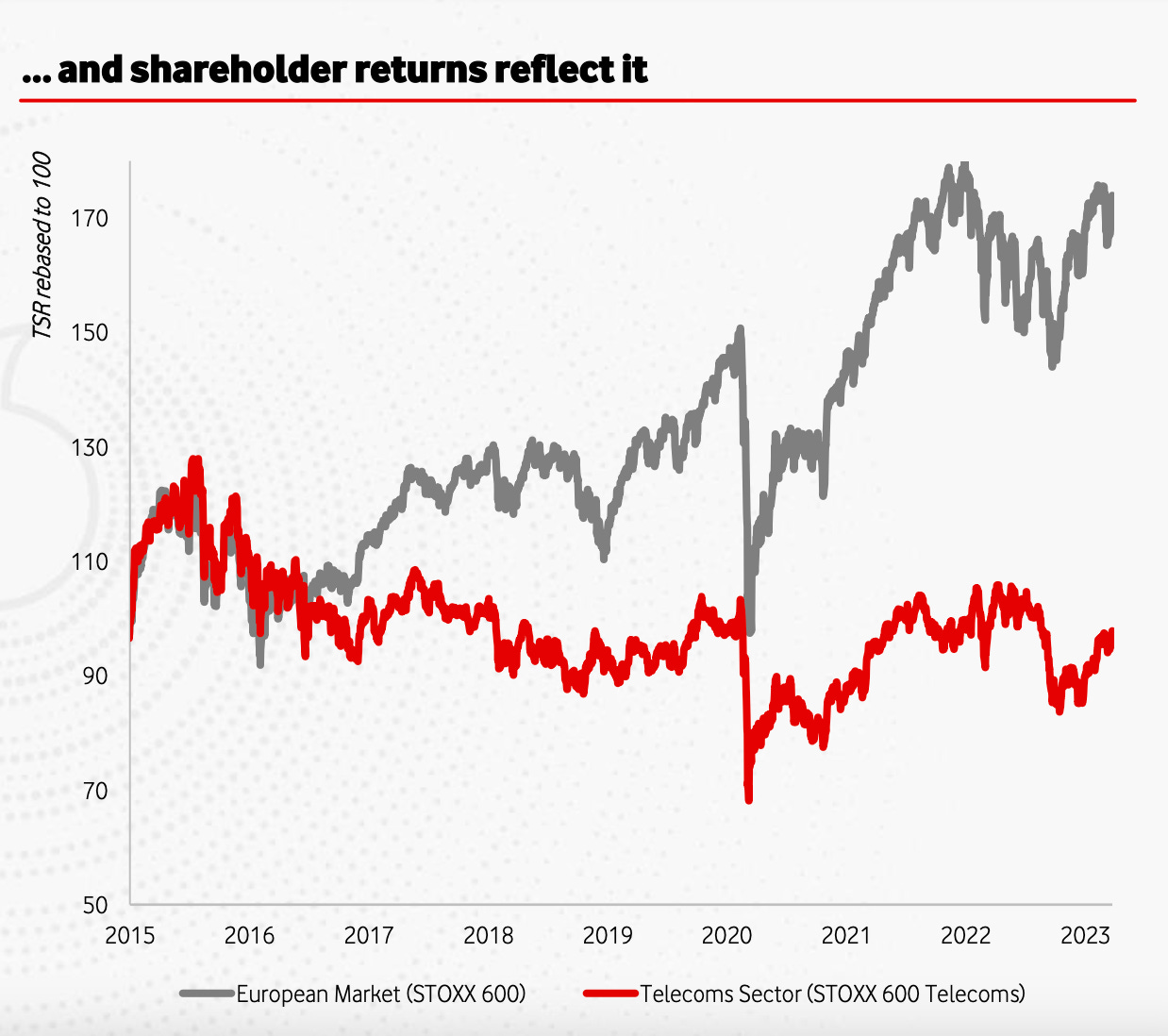

But I wanted to tell you about a new idea. The Telecom sector. They could be a new Untouchable. They’re hated and the dividend yields are 7-10%. AT&T and Vodafone in particular look interesting.

Coley: Telecom stocks are hated? Why?

Erik: They’re hated because 6 years ago the sector got excited about convergence of fibre to the home and mobile (the triple play) and decided to invest a lot of money building fibre lines to millions of homes all over the country. The idea was you would buy all your data needs from one company. Then 5G also came along and they needed to invest for that too.

So Capex has been running at record levels as they invested heavily in fibre, 5G spectrum, and 5G base stations. Meanwhile, the mobile telecom market has been highly competitive and prices have been flat to falling. Data consumption is up, so they need lots of infrastructure, which costs a lot of money, but the market is mature and pricing is going nowhere.

So the companies were providing more, and more capacity and struggling to grow revenues. They spent too much money, got overleveraged and had to cut their dividends. So now everyone hates them.

Perversely, the exciting theme of the growing need for data and 5G, which everyone was excited about, turned into sector wide over investment and a shareholder disaster. It’s similar to what semiconductors are doing now.

Coley: So why do we want be part of this disaster?

Erik: Because I think we are at inflection point. The telco CEO’s realise they have to change. They realise they over invested, are getting crappy returns and are the worst performing stocks in the market.

My view is over 2023-2024, AT&T and Vodafone wrap up the 5G spend, and because there is no 6G, they ratchet back capex by a few billion. At the same time they raise prices on mobile, because they can.

Mobile pricing hasn’t kept pace with inflation, all the players are in pain, and it’s in everyone’s interest to raise prices. Plus there is room to do so. Look at our mobile bill. Think about it. We use our phones all day, we sleep with them, and the bill for our family is 100 pounds. It’s a bargain compared to 20 pounds for one lousy burger at the pub. If Vodafone upped prices to 140/month would we think it was crazy? No.

So you get this massive swing in free cash flows as companies raise prices and lower capex. That makes the stock prices rerate. In the first stage investors go from worrying if the dividends are going to get cut, to realising they are sustainable and you get a small rerate. Then in stage 2 the telcos pay down debt and there is the realisation dividends might even grow so you get a second rerate. Three 3yrs out the dividend yield on the shares has rerated from 8% down to 6% and the dividend per share has grown +10%. You get 25-30% return from dividends and another 30% in stock price movement.

Telcos go from ‘untouchable’ back to the steady, defensive dividend payers they were supposed to be.

Coley: I don’t know..it seems kind of boring.

Erik: But if we get a recession boring will be what people want.

Knock. Knock.

Erik: Not sure who that is… I’ll get it. Hello?

John: Hi. Sorry for the surprise visit, but are you Erik from YWR? I’m John Stankey, CEO of AT&T. I’m on a flight back to Dallas, and connecting through London. I thought I’d take the opportunity while I was in town to talk to you. I heard you are working on a new Untouchable sector. And it’s Telcos.

Erik: John! Wow. Come in. Yes. Can I get you a red. It’s Waitrose brand. Hope you don't mind. This is my wife Coley.

John: Thank you. Yes on the wine. Anything is fine. Coley nice to meet you. That spaghetti and meatballs smells divine. Can I help you while Erik and I talk? Can I chop some garlic for you?

Coley: Wow Erik. Your friend is a real gentleman. Yes, please chop these if you don’t mind. Thank you!!

Erik: So John. How did you hear about Untouchable 7?

John: Well, it’s a weird story, but I was just in Barcelona at an industry conference. And after the conference we were having a party. And ZHU was there. And so ZHU and I were talking, sharing tracks, you know. And then he says he was partying with you guys last week in Chamonix, and that you had said you thought telcos could be a new Untouchable. So when I heard that I knew I had to drop in and chat with you about it.

Erik: ZHU wasn’t supposed to say anything, but he’s right. I was thinking you’ve been spending billions to add fibre to the home, and the share price has been killed because it. And you cut the dividend.

But maybe now we are about to see the returns from all this investment. Now you have top notch mobile combined with high speed fibre to the home and maybe now you finally win the triple play customers. Maybe investors are hitting peak bearishness right at the inflection point.

John: Erik… that’s exactly right. And let me add a few points. For the last three years our teams executed on a strategy in mobile that enabled us to go from annually losing share to now delivering the right combination of continued postpaid phone ads, low postpaid churn, growing average revenue per user, and profitability growth.

Now, let's turn to our fiber business. Our investment thesis for building more fiber started with our understanding that people needed better and faster broadband connectivity than what was available, that those needs would only grow exponentially. We believe that by providing the best access technology on the planet, we could transform our Consumer Wireline business into a fiber-fueled sustainable growth franchise. Our results have only strengthened that confidence as returns continue to exceed our initial expectations.

Over the past three years, we've had more than 3.4 million AT&T fiber net ads, boosting our subscriber base by roughly 80%. Everywhere we put fiber in the ground, we feel good about our ability to win with consumers. In fact, our average penetration rate is about 38%. Over the past three years, our fiber net additions have outpaced the leading cable providers' broadband net additions. This is an impressive accomplishment given the size of their footprint.

So let me summarize. Our mobile business is growing share in ARPU, low churn, and improving margins. And our fiber business is accelerating new build penetration, growing share in ARPU, while lowering churn and improving margins. This is the formula for sustainable top and bottom-line results, and we're confident this success will be sustainable over the next three years.

Erik: And you think you can grow by taking customers from the cable companies?

John: Yes, and here's why. As industry convergence accelerates, our economics in both fiber and wireless provide AT&T a strategic advantage that will be hard to match. The lifetime value of our mobile customer is significantly higher than that of a cable customer. Cable's busy adding wireless customers at low lifetime values just to protect customers they already have. We're not only keeping our own current high-value customers happy, but also adding more of them (from the cable companies).

Knock. Knock

Erik: That’s strange. Not sure why someone is at the door. I’ll get it. Hello.

Margherita: Hello. I’m sorry to disturb you this evening. Are you by chance the writer of YWR? I am Margherita Della Valle, CEO of the Vodafone Group. I was hoping I could speak to you.

Erik: Margherita! It’s nice to meet you. Come in. Your timing is good. This is my wife Coley and this is John Stankey, CEO of AT&T.

Here’s a glass of Waitrose red. And may I ask if you’re here to speak about Untouchable 7? And let me guess.. were you by chance at a party in Barcelona with ZHU?

Margherita: Yes, on both questions. I want to speak to you before you put out your post. I know the share price is awful, but I want to let you know we are really trying to change things at Vodafone.

Erik: Yes,the shares are getting hammered, but the dividend yield is 10% and Coley and I thought they were looking interesting. What’s the story? Why are the shares down so much and is the dividend secure, or are you about to cut it again? Because that’s what the share price is saying.

Margherita: You get right to the point. I’ll be honest. Our challenge today is three of our largest markets have declining revenue and our returns are below our cost of capital. Our performance relative to major competitors has also not been good enough. Germany has been especially difficult.

Vodafone has to change. And by change, I mean a significant redesign of where we focus our efforts and how we organize ourselves. We need to take out complexity and simplify how we operate. We have planned the reduction of 11,000 roles over the next three years in Germany and Italy. The resources it will free up will be reinvested in customer experience and in brand to support growth, which is my third priority.

Erik: I was telling Coley you should raise your prices. Are you doing that?

Margherita: We started raising retail prices in November, and will be repricing up our customer base throughout the first half of the year.

Erik: And what about capex? Can you cut back capex?

Margherita: We can’t cut dramatically yet, but we have a clear ambition to deliver returns in excess of cost of capital. We will discriminate, if you want, more strongly between the markets which we are returning cost of capital or the segment in which we have good returns, like business, and make sure that we allocate our CapEx accordingly and consider inorganic structural actions where the returns are not there.

And another thing. We have found there are lots of ways to improve the customer experience without expensive Capex.

We have plenty of data, as you would expect on that. What customers want us to improve is really this simple service. I know, it seems basic, but I think it's quite important, and I think sometimes overlooked in telcos.

Customers want to have a good experience when they upgrade, or they call the call centers. It's not about network performance. It's not about innovation. And it's not even value for money. And I think that's what we need to focus on. And it's in our DNA to work on it.

Erik: Sorry to pester, but the dividend?

Margherita: We sold some towers, so our leverage is down to 2.5x EBITDA, which I’m comfortable with, and so I’ve reconfirmed the dividend at 9 euro cents.

Coley: John, Margherita. This has been really helpful. Thank you for stopping by. We are about to eat, so I am going to have to wrap this up. But thank you again. And John, great job on the chopping. Show Erik some time.

Erik: Yes, see you. Thank you for the visit. Good night.

John & Margherita: Good night.

After John and Margherita have left.

Erik: So what did you think? Should we start small and buy some AT&T and Vodafone?

Coley: The dividend yields are 7-10%, but aren’t we already getting that with what we have? And didn’t you say Santander just increased the 1H div by 39%? And didn’t Commerzbank today say they were going to distribute EUR 2.7bn in dividends and buybacks from now until May 2025, or 20% of the market cap?

I think we keep stacking up shares in what we have, but keep an eye on the Telcos. Good work though.

And can you do me a favour?

Please can you take Roosevelt out quickly? I think he needs to go #2.

Thanks.

Erik: OK. Sure. Come on Roosevelt.

************************

If you want the models for AT&T and Vodafone the links are below.

Have a good weekend!

Erik