YWR: Untouchable #9

A new Untouchable… #9

Totally hated.

Same as the others before it.

Untouchables #1 & 2: Mining and Energy (September 2021)

Untouchable #3: European Banks (September 2021)

Untouchable #4: European Autos (September 2022)

Untouchable #5: Airlines (May 2023)

Untouchable 5b: Tobacco (July 2023)

Untouchable #6: US and UK Telecoms (September 2023)

Untouchable #7: China (April 2024)

Untouchable #8: Renewable Energy Stocks (February 2025)

Trading at multi-decade low valuations.

Everyone knows it has no future. Just an unstoppable bleed out to eventual death.

The problems are obvious and unfixable. No one can imagine an alternative reality.

And yet… I see a combination of events coming together which could turn these headwinds into tailwinds. At least for a while.

I see the set-up for a multi-year renaissance for this hated industry, which if it happens, would give us an explosive combination of earnings upgrades and revaluation.

What sector am I talking about?

What is our new Untouchable?

It’s Active asset managers.

Yes. I’m talking AB, TROW, JHG, IVZ, SDR LN, AMUN FR, APAM, BEN, GQG AU,

The big ugly, hated mutual fund complexes. Dinosaurs from an ancient era when people respected portfolio managers and cared what they thought.

I know what you are thinking, but let’s breakdown the 3 main problems.

#1 Severe underperformance versus the S&P 500. Over the last 10 years only 2.5% of active large-cap growth managers beat their benchmark. A track record so shockingly bad that literally a monkey would have done better. Active management becomes a joke.

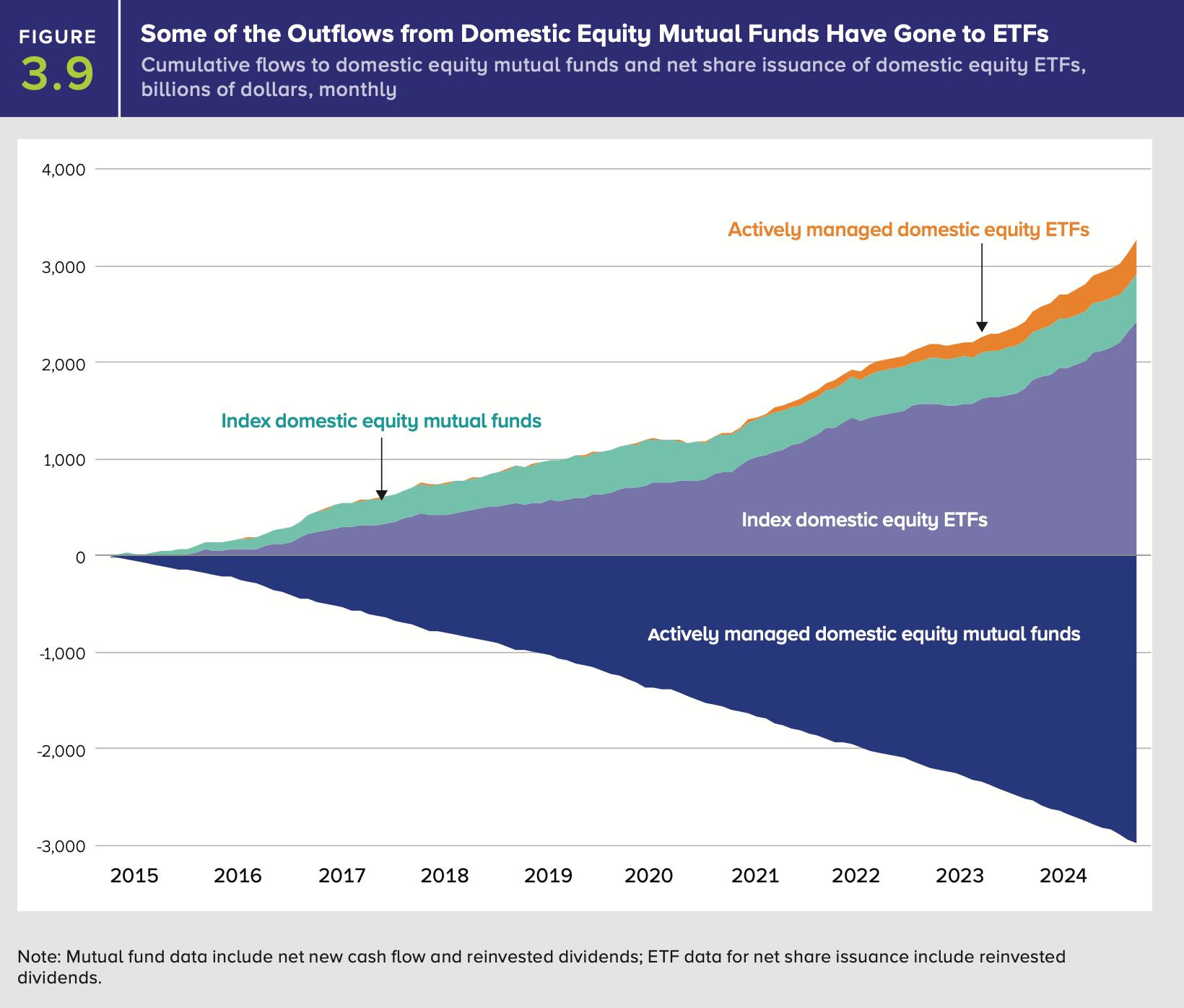

#2 Switch to ETF’s: This severely bad performance and the rise of ETF’s led to $3 TRILLION in cumulative outflows from active funds to index funds and indexed ETF’s from 2015-2024. Despite supposedly being experts at analysing industries, active equity managers take 6 years to react the biggest disruptive trend in their own industry. 6 years to realise the ETF is a superior product for the consumer. Trade it anytime and trade options on it.

#3 Switch from Public to Private: When institutions needed something to sell so they could add more to PE, they turned to active equity mandates. Institutional asset allocation in 2026 is a long list of PE funds for the PE bucket then indexation of the equities by BlackRock for 10bps or in-house. No need for active equity mandates.

Given this set up how could things possibly improve?

This is a death spiral. How do we get bullish?

Indexation and ‘What is Water?’

Kansas City FundCo

The FAANGM Anomaly

Every Dog Gets its Day

Actively Managed ETF’s.

Private assets for All.

Asymmetric Valuation Set-Up.

Indexation and ‘What is Water?’

Let’s say it’s 1974 and you are in the fund seeding business. A guy named ‘Jack’ comes into your office to pitch you a new idea for a fund.