YWR: Why 10yrs go to 6%

I see three reasons 10yr yields can move to 6%.

I’m not wild about this view, but let’s go through it.

The Backdrop: Inflation never died.

Think back to pre-COVID. If I told I had a crystal ball and the Fed was going to raise rates from 0% to 5%, you would have said the economy would crash. No way consumer and businesses can withstand a yield shock like that.

But we did.

I’m always interested in the dog that doesn’t bark.

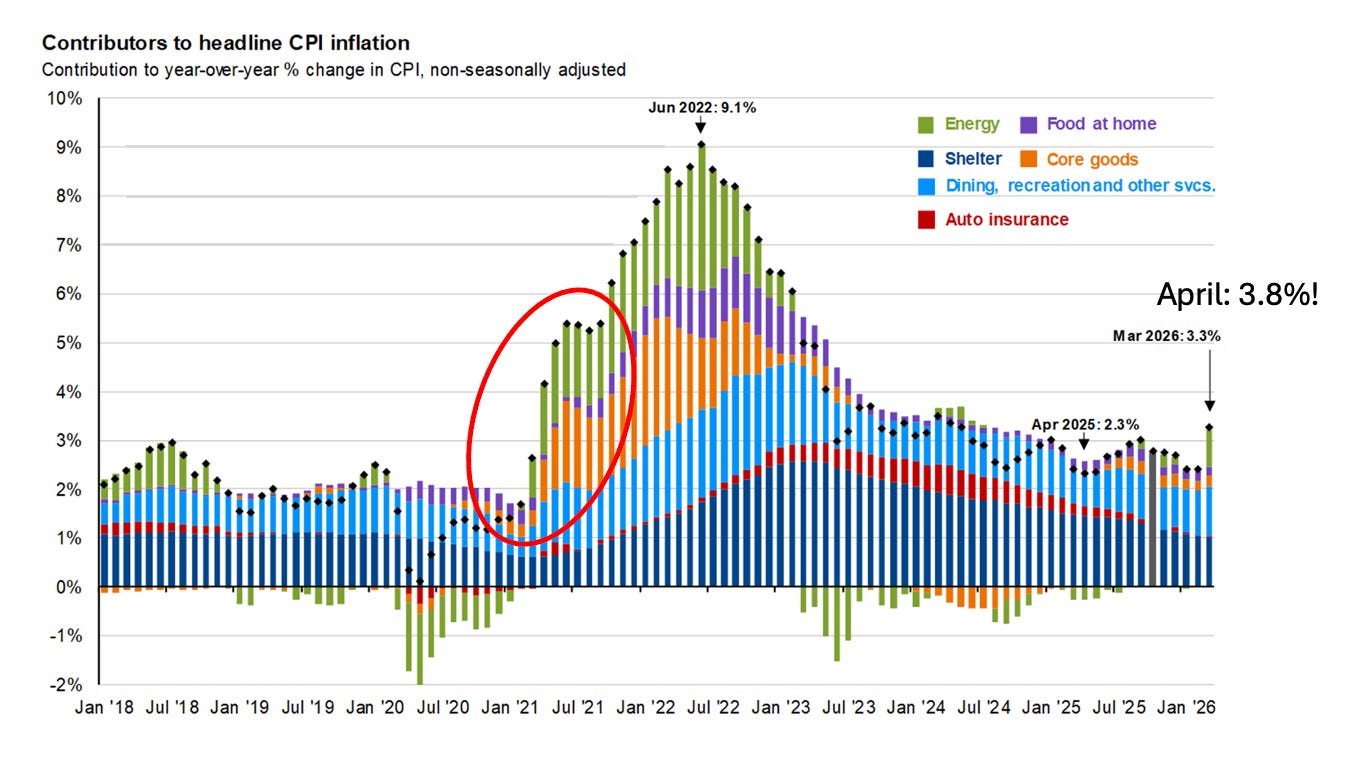

After the Fed raised rates to 5% we didn’t get the deflationary crash everyone expected. And inflation never went back to sub 2%, despite all the Fed predictions that it would.

Instead inflation stabilised around 3%.

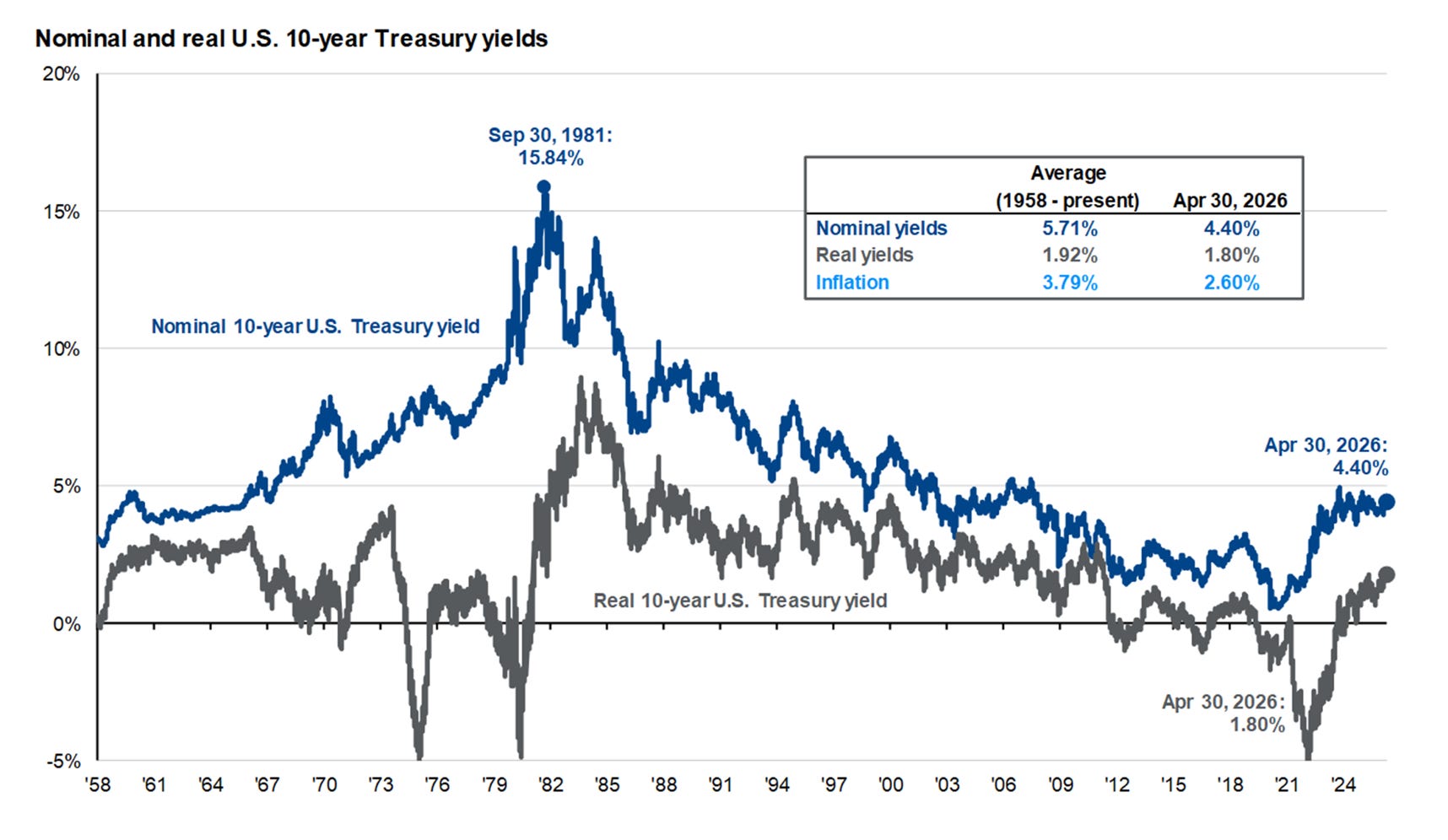

And US 10 year yields hovered in the 4-5% range.

Which creates a concerning chart. A chart which suggests we are in a new era. An era of rising yields. And it’s just a matter of time before we get the next move higher.

Here are the three trends I see converging.

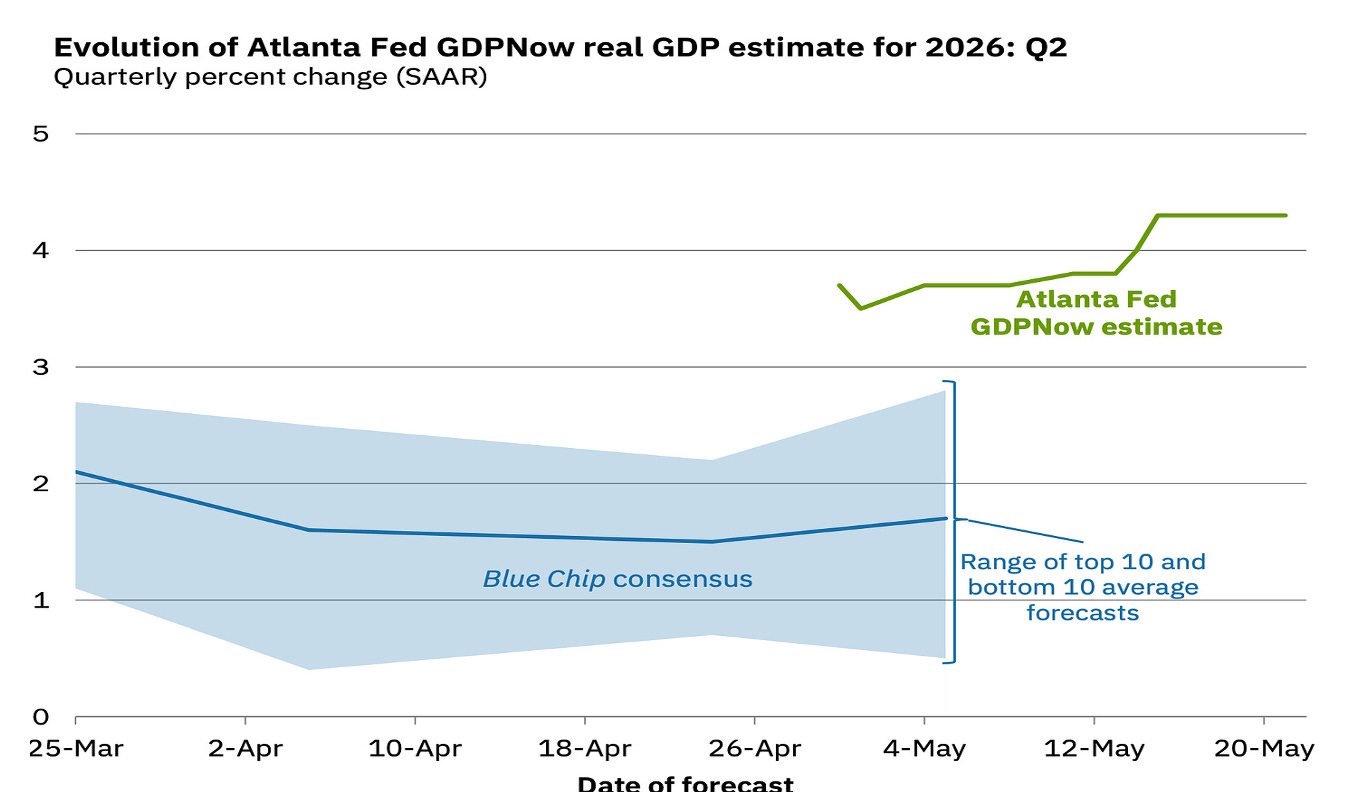

#1 The US Economy is Running Hot.

Every month I try to save you from the bears by putting together Boom Charts presentations which track the economic acceleration underway.

What’s driving it?

We have government deficits running 5-6% (which normally would be recessionary stimulus), on top of corporate capex through the roof because of a revolutionary new technology.

Governments and companies spending their brains out.

Added to this is something the market doesn’t fully appreciate yet.

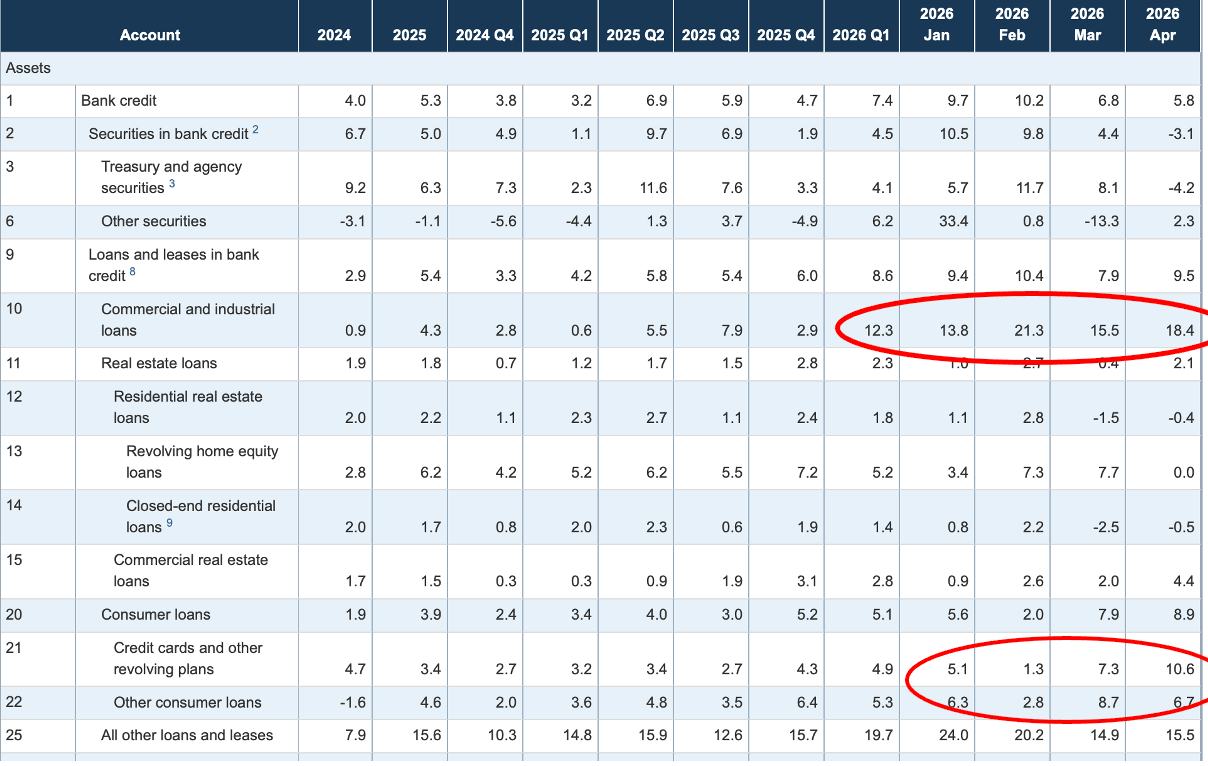

Banks in the Europe, the US and Japan are back to lending again. Banks are the true money creators. It’s taken a long time, but the post-GFC winter is thawing and banks are getting their animal spirits back. It’s Trump, it’s Warsh, it’s a whole change in tone from the top that it’s OK to take risk.

And now they are.

Total loan growth for US commercial banks is running at 10%, compared with 3-5% previously. Commercial and Industrial loans are especially hot (+15-20%).

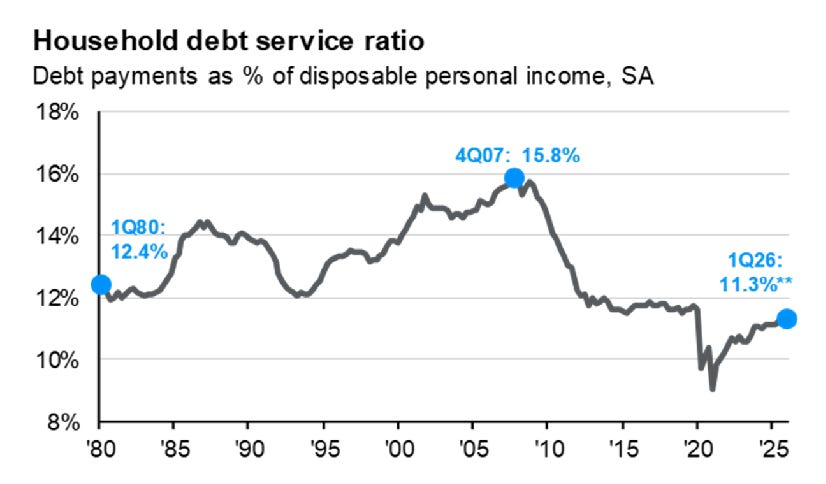

I also see another trend. A pick up in consumer lending. Both consumers and corporates have been on a 15 year deleveraging trend since the GFC. Which puts them in the position, that if they want to borrow, they can. The consumer has an amazing balance sheet, a job, wage increases and a debt service ratio at the low end of the range. So consumers are starting to borrow again.

Put it all together (government spending, corporate spending, loan growth) and you get 4% GDP growth.

That’s not China. It’s the US. Bam!

Reason #1 rates can go higher is because we have strong hot economic growth.

#2 Delayed effect of Tariffs

Do you remember all the panic last year around tariffs and how they were going to cause an inflationary spike? Instead inflation was fine, bond yields went nowhere and the market roofed it. That’s when we proposed something radical (S&P $10,000).

But I want to share something from the EM playbook.

When the FX crashes in an EM economy consumer stocks initially get killed. Right after the FX move consumer companies are careful to not shock the consumer. Their costs go up, but they can’t pass it on to their customers. Margins get hammered. But the trade is that that is the time to buy them. Over the next 12-18 months they raise prices gradually and claw back their margin. Revenues grow, margins expand and earnings beat expectations. This is the trade many miss. They assume the margin compression is permanent.

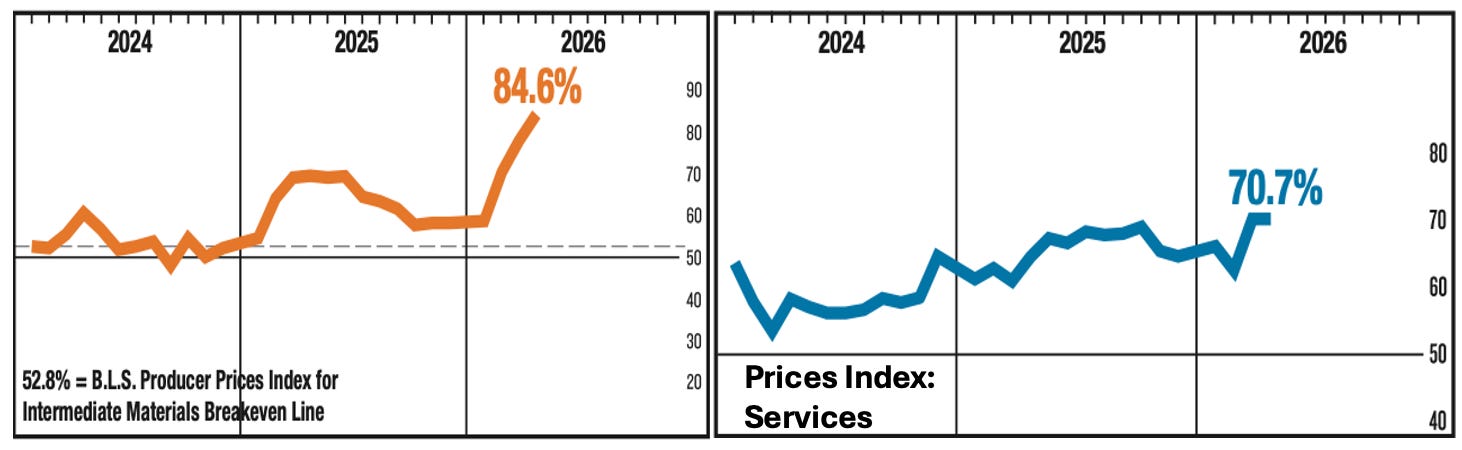

I think we might be seeing this in the US. Tariffs went up but companies were careful about passing it on to consumers right away. Plus they had existing lower cost inventory which they could use to smooth out the effect. But now 1 year later we are seeing the costs come through.

When you look at the PMI reports for Manufacturing and Services the prices component is through the roof.

Everyone is raising prices across the board.

It could be a mix of things, including the strong economy, but I think this is also the tariff impact finally coming through.

A trading thought: Everyone hates consumer discretionary. But if this is like EM where consumer companies gradually raise prices and get their margins back, plus the consumer is starting to borrow again because the economy is pumping… could this be the surprise outperformance sector? Short semis- long consumer?

Reason #2 is the delayed inflationary impact from tariffs finally coming through.

Now reason #3 interest rates go higher.

#3 Energy and Food

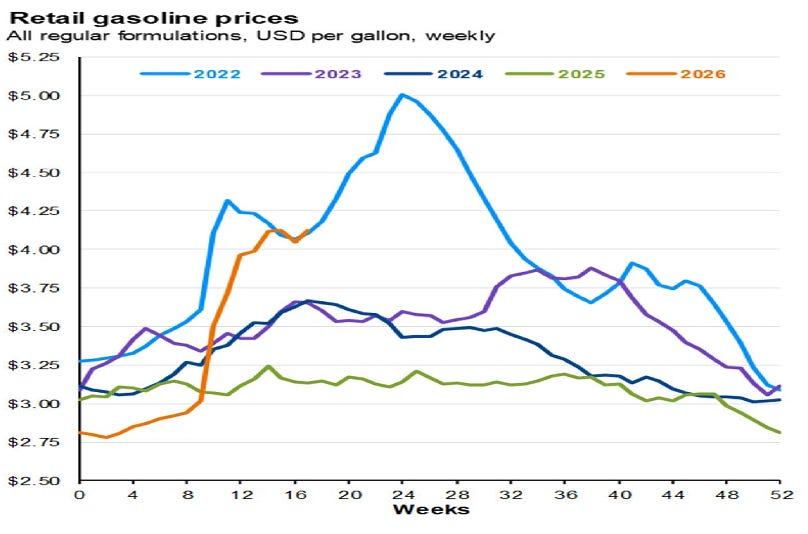

The Iran War seems to be stuck in a deadlock. Is this something we need to get used to for the long-term? Do we get another leg higher in energy prices before this is finally resolved?

The move in gasoline prices resembles the early part of the move in 2022.

Same thing with urea prices.

We are getting a pop in energy driven inflation readings.

Overall inflation was +3.3% in March then +3.8% in April. That’s getting close to 4%.

In the context of the last 30 years $100 Brent is not that high, especially given overall inflation ($15 for a beer). That’s why the move to $100 hasn’t been a big deal for the market. ‘Expensive’ oil prices today would be in the $150-200/barrel range.

Putting it all together energy and food prices can go higher in absolute terms which feeds through into CPI for several more months.

Higher energy and food prices are going to be on top of price increases businesses are already pushing through to pay for higher tariffs.

Which means we could have inflation readings in the +4% range for a sustained period.

And because the economy is running hot, and the Fed will be afraid to raise rates, the 10 year rises to 6%.

Let’s leave it there and have a think about it.

Have a good weekend and remember The Nairobi Solution Ch.8 drops on Sunday.

Here’s Chapter 7 to get you caught up.

Erik

Hey Erik! Regarding the consumer, what are your thoughts on oil at 150 to 200 dollars? Looks like the energy shock is just beginning… disposable income will be squeezed hard especially at lower part of K economy. Consumer sentiment at extreme lows. On top of that employees not feeling brave to ask for salary raises on back of A.I. threat to employment. I can’t see a rebound on consumer cyclicals any time soon… could it be that loans are high because people are squeezed? Need to pay attention to NPLs..

a generalised sell off that pulls everything down could happen unless we have even more support from gov… I think only banks, energy, and tech (software and hardware) do well. And perhaps orthogonal healthcare as a separate theme.

Some people a drawing parallels to 2007 2008 increase in oil prices before the GFC. Also the mad valuation of SpaceX open Ai and Anthropic hitting the market this year. It appears a great transfer of wealth from Nasdaq investor to Elon on the first part. How is it that Nasdaq passive investors are forced to buy spacex at 100 times sales… it’s insane.

And Hormuz… how will Trump climb down?

market is complacent. Sorry for the rant! Any thoughts on where you see the pessimistic bear side is wrong would be much appreciated

C O N S E R V A T I V E !

We’re looking at 7.5 - 8%. Then settling back to 5-6%.