YWR: Why does QARV work so well?

The Most Annoying Colleague

Four years ago I was working with a colleague on an investment strategy for a global absolute return fund. We had a small team and were trying to think how we could have a view on thousands of companies around the world from an office in London with no travel budget. We all agreed some kind of systematic quant strategy was necessary.

This colleague had a mannerism of speaking loudly and having a strong opinion on everything. He wasn’t mean natured, he just had a way of stating everything as an undisputed fact. One of his predetermined ‘undisputed facts’ was that this new fund would only invest in ‘Quality’ stocks. ‘Quality’ was the best performing style and we would simply rank the top stocks in the world for ‘Quality’ with a few valuation parameters added in to create what he called ‘Quality at a Reasonable Value’ or QARV.

I was less sure. Yes, Quality as a factor had performed well for many years, but was there cyclicality to this factor? Were we committing the fund strategy to ‘Quality’ right at the end of a multi-year run? Like buying ‘Growth’ stocks , just when ‘Value’ is about to outperform.

The other problem I had was that the ranking model’s use of EBITDA metrics didn’t work for bank stocks. Bank stocks don’t have EBITDA, or they do, but it’s kind of a useless metric. “How will we handle banking stocks?” I asked.

"We will just exclude them.” my colleague declared.

“And we will exclude mining stocks too.” he added.

“Banks and miners detract value over time and there is no reason to own them in a portfolio.” he stated with certainty. “They add unnecessary volatility. So we will not own them or worry about including them in the ranking model.”

I tried debating him that maybe there could be a time, even years, when banks or mining stocks would outperform, and wasn’t it dangerous to not even have these sectors in the model, but he was confident this was would never happen.

See what I mean?

I was also worried about the valuations on a lot of the tech and semiconductor stocks his model was throwing up. Many of the model’s ranking factors were based off annual metrics (like net debt/equity), which didn’t change much over the year. The rankings were quite stable and so the turnover in the quarterly rebalancing was low. Effectively, it was a buy and hold strategy. We were supposed to buy these ‘Quality at a Reasonable Valuation’ stocks and let the quality factor work.

That fund never got off the ground and so it wasn’t something we had to worry about. Even better, a year after that conversation a lot of the semiconductor stocks we would have owned were not doing well, which made me smug that my naive colleague and his QARV model had called the peak in the ‘Quality’ factor. My skepticism had been right.

That was 4 years ago. And now I’m not feeling so smug. Yes, in 2022, the year immediately after we ran the rankings, the stocks didn’t work so well, but since then the returns have been amazing. Semis had a bad 2022, but then caught the AI wave and have gone up multiple X’s. And tech stocks like Microsoft, Apple and Google have gone on to make new highs too. Over time the QARV model would have done exceptionally well.

I bring this up because I saw this colleague recently at a party.

And even though it’s embarrassing I try to make it a habit to always openly admit when my calls are wrong. So at the party I decided to tell him how well his QARV model worked and how much I liked it now. He loved hearing this and we went on talking about it for awhile. He said he would send me the latest rankings.

What’s the deal with Quality?

‘Quality’ is an interesting factor. It isn’t always defined the same way, but generally it means low debt/equity, high ROE’s and low earnings variability (MSCI Quality Methodology).

What’s strange about ‘Quality’ is how consistently it has outperformed for long periods of time. Like 30 years.

‘Growth’ and ‘Value’ can swing back and forth, but ‘Quality’ seems to outperform by a few % every year, without much giveback.

As you can see in the chart below the relative outperformance of Quality has been consistent for 30 years!

Project Zimbabwe and ‘Quality’

One of our YWR themes is that we are in a sustained period of higher inflation. We don’t know the exact CPI, but it’s more in the range of 3% of 5%, and not 1-2%.

The consensus view is that the way to play higher inflation paradigm is through value stocks. The idea is with inflation nominal growth is no longer scarce. Cheap stocks can ‘grow’ again. You don’t need to pay so much for high priced tech stocks. The rule of thumb is that Mining and Energy stocks are typical inflation plays.

But I’m starting to wonder if actually ‘Quality’ is the longer term winner. Yes, there will be huge years when value snaps back, but if we think out over years 5-10, is it worth paying the higher P/E for the less capital intensive business with higher cash flows?

Is the under appreciated challenge for the Value stocks that their higher capital base is more expensive to maintain in a high inflation environment? And over time it is better to be in the capital light business even if you have to pay up a lot for them in Year 1?

We’ve been tiptoeing around this concept with our China Tech, HKEX and SGX positions, but the James Davolos interview on Money Matters makes me think maybe we should be doing more with the exchanges.

And it makes me very conflicted on the US tech stocks. Yes, they are expensive and they’ve done well for years, but it bothers me that none of my professional colleagues are bullish on them. We are all supposed to be investing ‘experts’ and yet we are consistently wrong on the biggest most profitable businesses in the world. It almost makes me contrarianly positive on them.

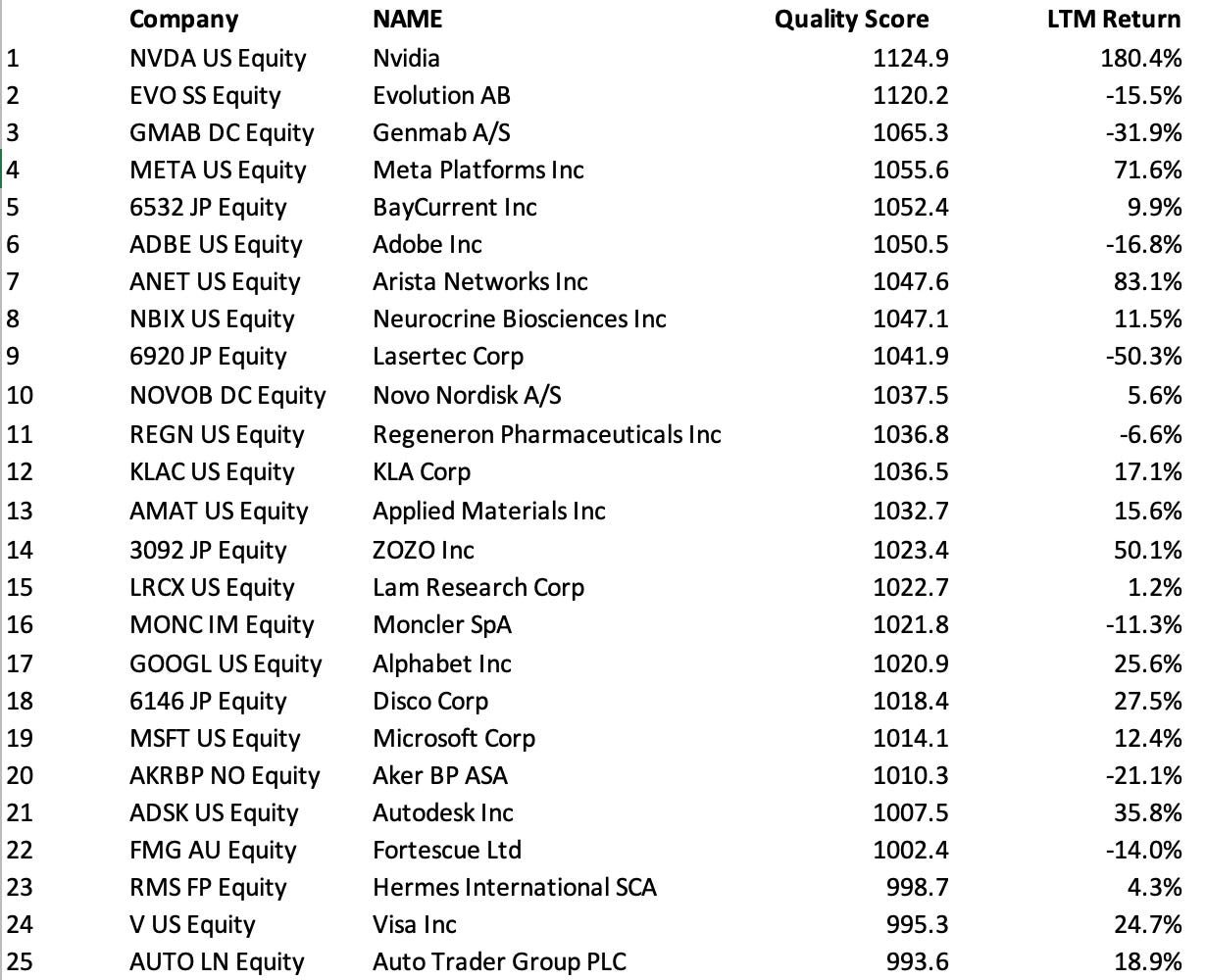

QARV Top 25

If you are interested in QARV, here are the Top 25.

There is a link at the bottom of the post to the full rankings file with rankings on over 1,300 global stocks.

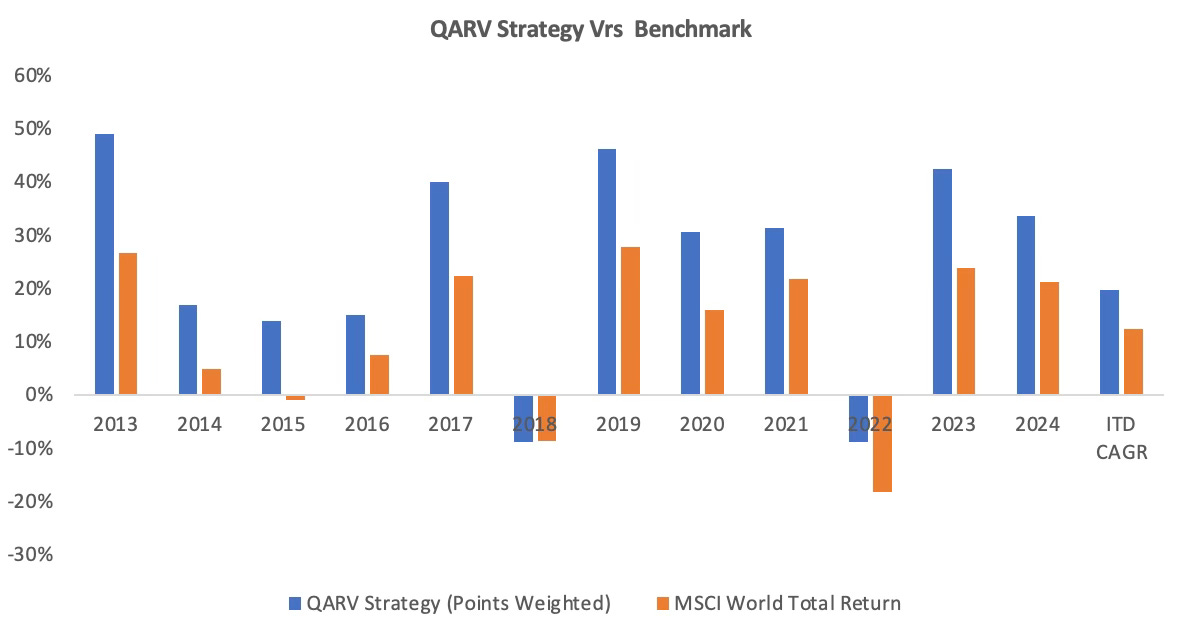

Below is the backtest of how these rankings have performed vs the MSCI World Index.

Link below to full QARV rankings (as of November 29, 2024)

Have a good weekend.