YWR: Would you be interested in Nvidia on 7x?

SK Hynix is a gem (000660 KS).

There’s probably 100% upside in the shares through 2027.

If we had 1 min in an elevator I’d say it’s Nvidia on 7x earnings.

Let me explain.

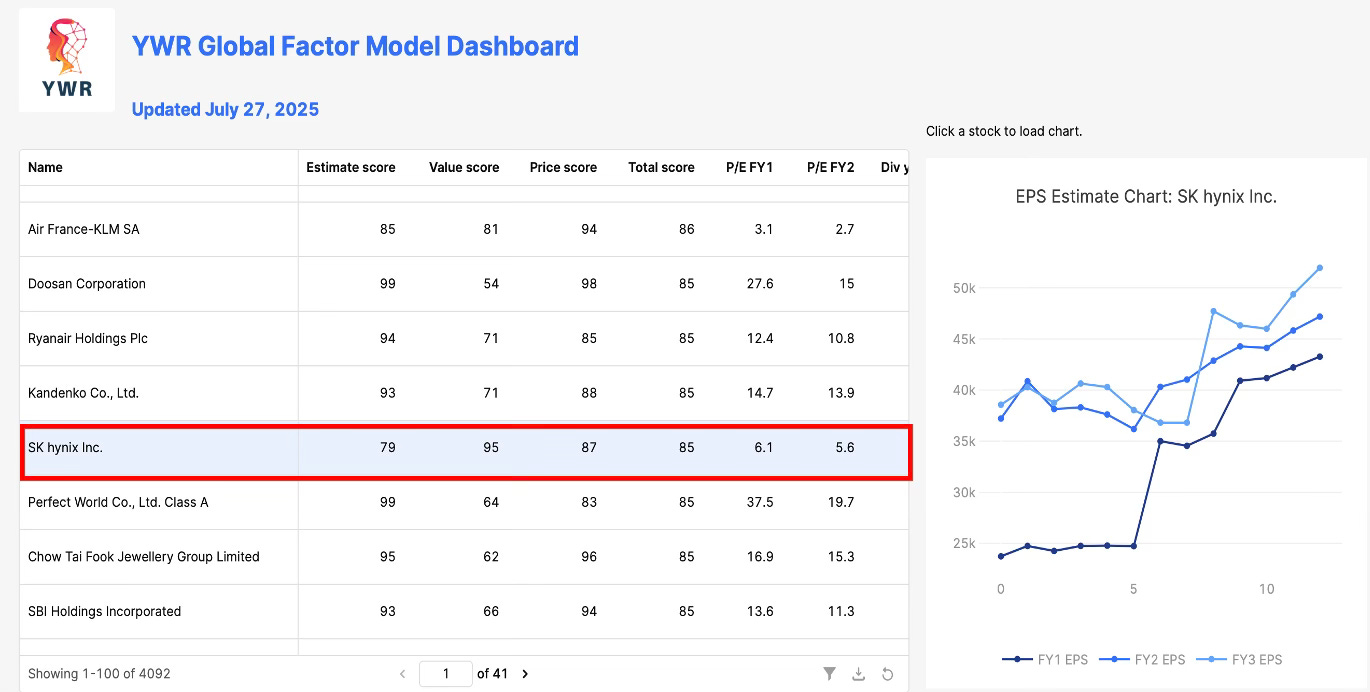

The Global Factor Model has been screaming at us to work on SK Hynix since 2024.

The model loved SK Hynix’s world leading estimate revisions, price momentum and P/E less than 7x.

But like we discussed in Why Estimate Revisions Work, the factor model just tells us there is something new happening which analysts don’t fully understand. It’s up to us to do the digging and find the story.

So I finally did the work because it’s 11% of our ishares Korea ETF and also because one of our themes has been that hardware is the new software. SK Hynix is another data point in this theme.

How HBM changes the game

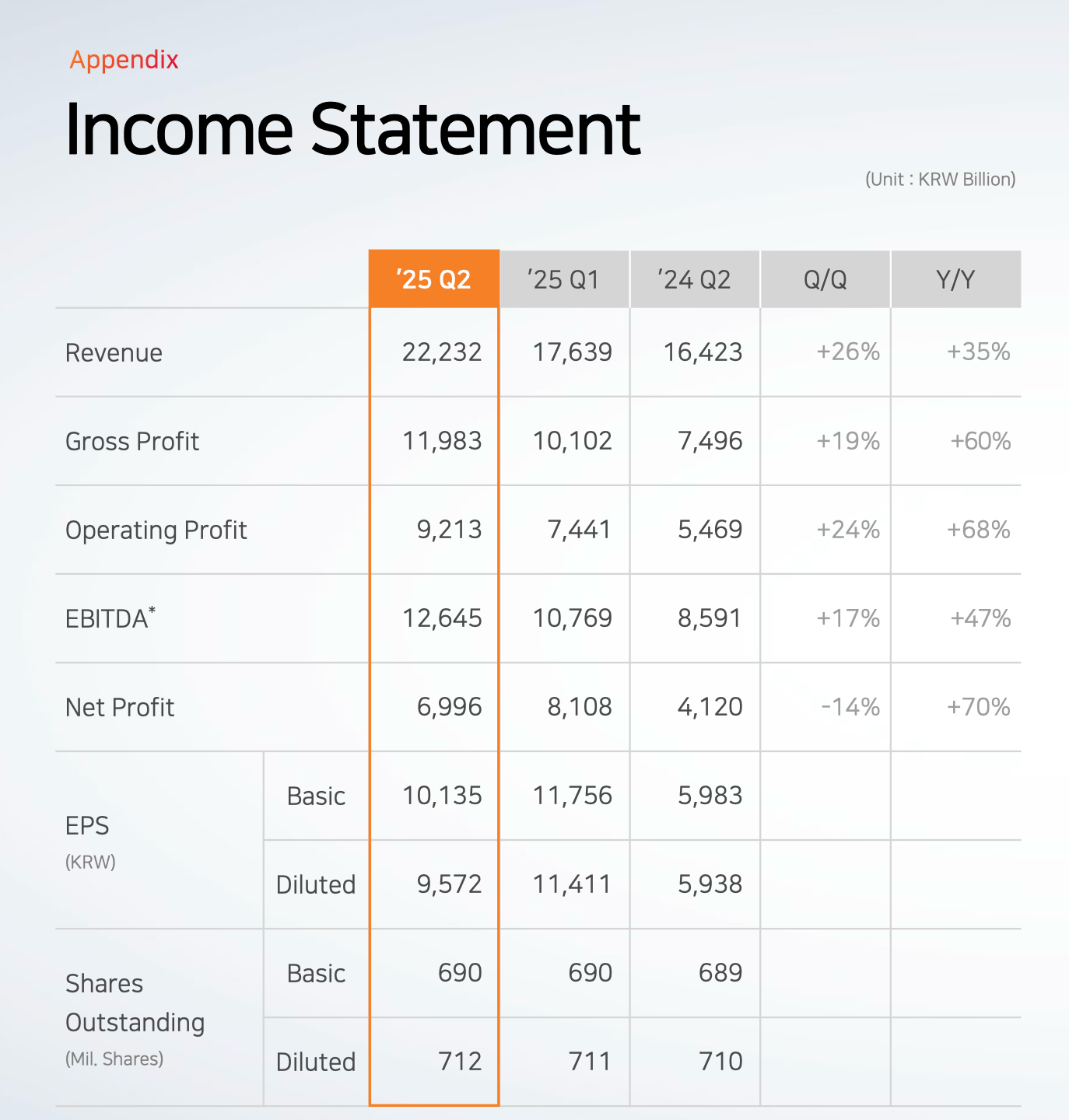

SK Hynix’s earnings are exploding.

Revenues +35%.

Operating profit +68%

Net profit +70%.

But why is this happening? And can it last?

To understand the revenue growth and margin expansion in an industry famous for ruining every good thing with price competition we have to understand what’s new.

HBM. High Bandwidth Memory.

In 2015 SK Hynix pioneered a new monster memory chip so over spec’d no one knew what to do with it. SK Hynix had stacked 8 DRAM chips on top of each other. Stacking the chips on top of each other enabled unprecedentedly fast memory access for a GPU. But at the time the only conceivable use for this high speed memory chip was potentially a high end graphics video game. Back in 2013 that was the biggest use case for high-end GPU’s that anyone could think of.

So HBM was a cool product, but super niche with no real use case.

Still SK’s engineers persisted with developing HBM chips. Their view was a use case would emerge for this incredibly fast chip.

We know what happens next.

GPU’s evolve from being a niche chip for video games to becoming the center of AI computation.

The leading developer of GPU chips goes parabolic.

The Memory Wall

AI is booming. And Nvidia is developing faster and faster GPU’s.

But a problem has emerged.

The Memory Wall or the Memory Bottleneck.

The memory chips necessary to support AI GPU’s haven’t kept up with the faster processing speeds.

Memory chip speed has become a drag on AI processor speed.

Which has swung the entire AI industry’s attention to memory chip speed, and to HBM memory chips in particular, and to the world leader in HBM chips… our friend SK Hynix with over 60% global market share in HBM.

SK Hynix finds itself at the centre of AI development.

Why this time it’s different.

So why is this world leader with 60% market share in HBM chips, the critical chip for improving AI speed, trading on a P/E of 7x?

Because the skeptics think they’ve seen it all before. This is a memory chip company. Things always boom and bust. Sure there’s demand now, but in the next 2 years capacity will increase and profits will collapse. Like in the past. Memory is a cyclical boom bust industry which never makes money.

Everyone knows that.

So why is it different?

3 Reasons