PE/VC Q3 2024 Deal Tracker

Every quarter we check in on the Private Equity and VC deal flow. It’s good to know what they are doing with your money, but it also sparks ideas for our public investments.

The full Q3 deal database is at the bottom

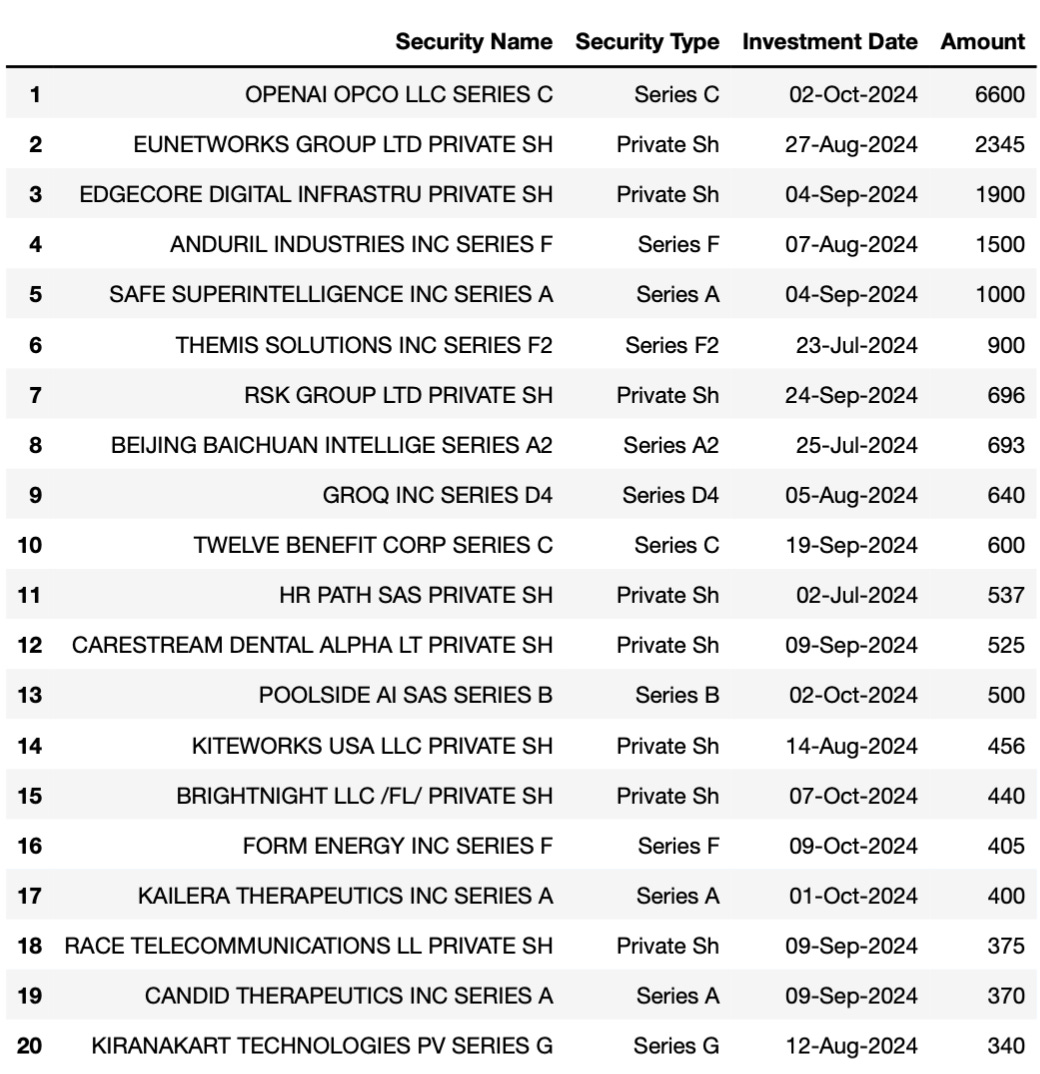

Top 20 PEVC Deals in Q3 2024*

*Many deals do not have deal size information disclosed. VC deals are more likely to have deal size data.

OpenAI: Thrive, Softbank, Microsoft, Nvidia and Fidelity all participated in the OpenAI capital raise. Apple didn’t. Microsoft and Nvidia’s participation brings up the question of whether this whole AI ecosystem has gone circular with the chip and hyperscaler companies funding OpenAI so it can keep buying chips and compute. Good article from Edward Zitron on why OpenAI is a bad business and will need perpetual capital raises.

Eunetworks owns high-speed fibre in 18 large European cities (London, Paris, Amsterdam, Dublin, Berlin, Hamburg, etc). It’s backed by Stonepeak Infrastructure, who mostly came out of Macquarie Infrastructure. Like all PE firms Stonepeak has been buying datacenters, fibre and cell towers because they see a trend of growing data connectivity.

Edgecore Digital Infrastructure: This is Edgecore’s 3rd capital raise this year bring the total to $4.24bn ($1.9bn in January, $440mn in March, $1.9bn in September). They are using the money to build AI data centers. Partners Group in Switzerland has been leading these capital raises. Data centres have been a huge theme all year ($6.4bn into Vantage Datacenters in January, $1.3bn into Estruxture Data Centers in June, etc).

Anduril raises another $1.5bn. This is the cool AI drone defence company. Fidelity, Counterpoint Global and Baillie Gifford participated. Baillie Gifford’s strong focus on ESG didn’t stop them from investing in attack drones.

Safe SuperIntelligence: It’s nice when the day you start a new company, it’s worth $5bn. That’s the story of Ilya Sutskever, a cofounder at OpenAI, who left after a disagreement with Sam Altman about safe AI.

Safe SuperIntelligence is differentiated from the other AI companies. Unlike OpenAI, Anthropic and xAI which are trying to find business and consumer applications, Super Intelligence AI will just focus on research.

“It’s important for us to be surrounded by investors who understand, respect and support our mission, which is to make a straight shot to safe superintelligence and in particular to spend a couple of years doing R&D on our product before bringing it to market.” AINews

Sequoia and Andreesen Horowitz led the $1bn round at a $5bn valuation.

RSK’s $696mn capital raise led by Searchlight Capital and Ares shows sustainability isn’t completely dead. RSK is an environmental consulting firm. Kind of a backdoor play on renewable development.

Poolside AI is another interesting one. It is 16 months old (founded in April 2023) has no product, but intends to develop AI coding assistants (of which there are already many including Amazon Q) and is worth $3bn. The $500mn round was led by Bain Ventures, Nvidia, HSBC Ventures and Citi Ventures

Folks….this looks like a circular train smash. The VC funds + the hyperscalers (MSFT, Nvidia) pour in money to fund AI start ups which in turn spend that money on chips and datacenters. Many of these companies are less than 3 years old and seem to have no product.

Isn’t this like Pets.com where we are going to be laughing about how stupid everyone was?

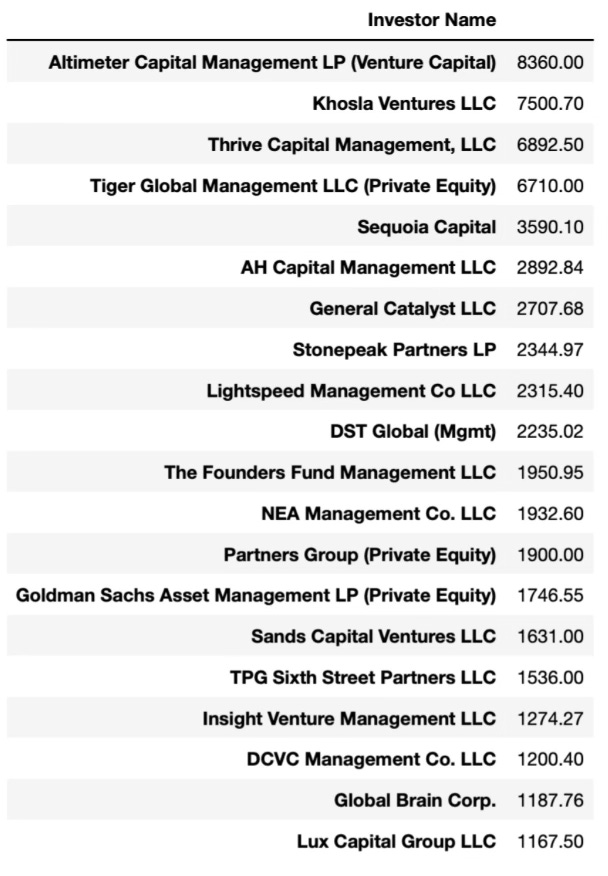

Most Active Funds

The data has many imperfections, but this is which funds are most active by adding up all the deals where they participated. It depends whether a fund participated in a big deal with a stated value.

For example, Altimeter participated in OpenAI, Anduril and Scio Technologies all in the same quarter, so they screen as highly active. Thrive participates in all the OpenAI rounds.

Deals under $100mn

We always focus on the big deals, but most VC capital raises are less than $100mn.

KKR Deep Dive

A lot of traditional PE deals don’t have information on the size, which is why firms like KKR seem less active, but they arent’.

Below is their Q3 deal flow.

I want to flag the Telecom Italia deal (#7). KKR spent $20bn to buy Telecom Italia’s fixed line assets. KKR has been working on this deal for years and it finally got EU Competition approval. The background is that Telecom Italia got over leveraged, became unprofitable, and has been spinning of towers and fixed line assets to deleverage.

Telecom Italia is in a death spiral and selling whatever they can to KKR to deleverage. This is happening right in front of Mario Draghi, which is why the profitability of European telcos is important to him and it was a focus item in his report. He doesn’t like seeing the whole industry get picked apart by US PE funds. Are European telcos the equivalent of US railroads in the 1980’s? (A Secret to Making Money)

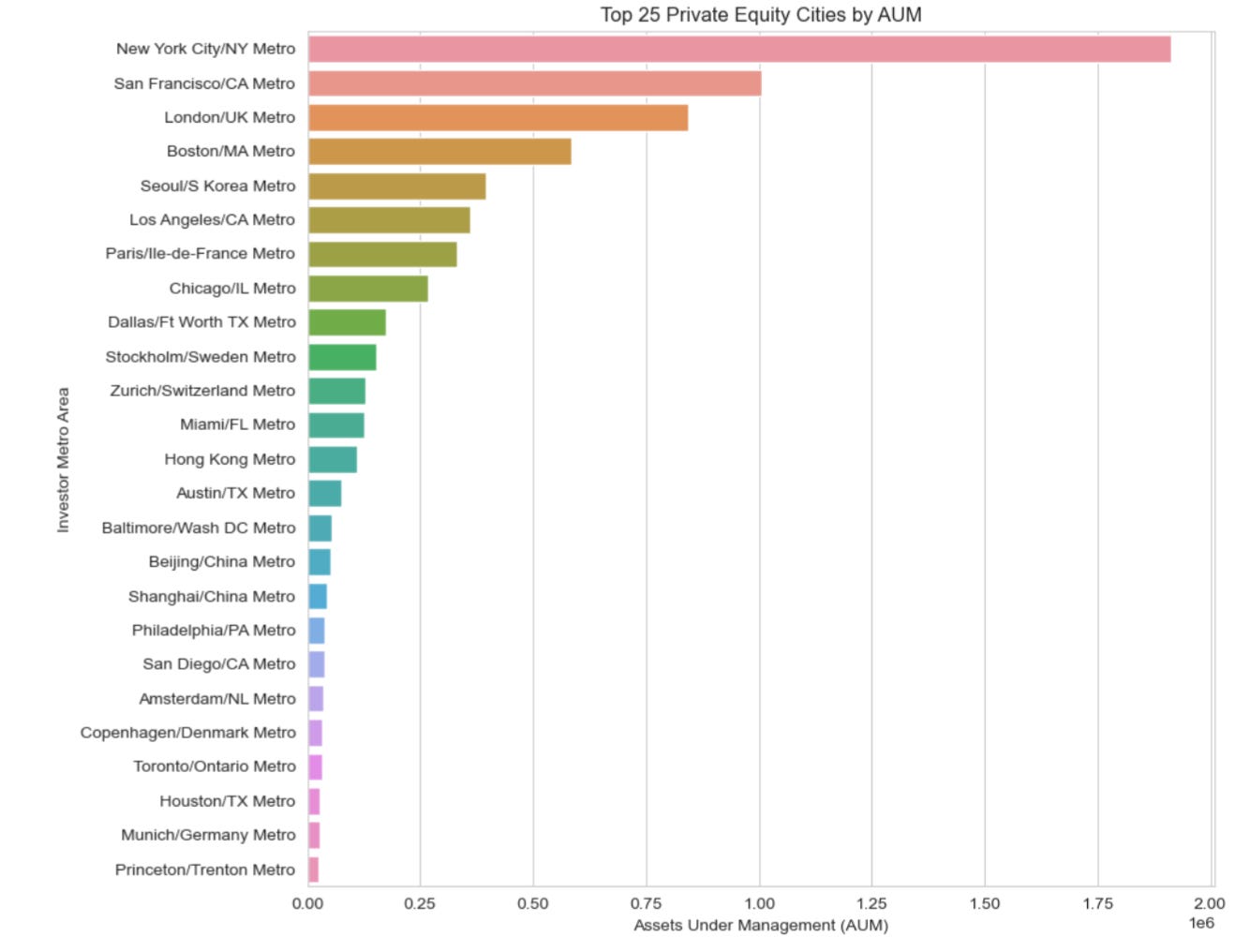

Top Cities for PE and VC Funds

Top Industries for PE and VC investment.

We go through 46,000 portfolio company holdings and sort by industry. Michael Pettis has a view that even though the US doesn’t have an industrial policy, China does. And by default US industrial policy is the reciprocal of China’s. If China wants to dominate manufacturing that forces the US into software, which is what you see when you look at the PE/VC portfolio holdings.

Nobody wants to investing casinos, banks, railroads, gold, autos or tobacco.

Below is a link to the full Q3 2024 Deals database.

All datasets are also available in the Datasets and Models section and www.ywr.world.