YWR: +100% upside in Ping An

Everyone’s talking about European banks.

Which is cool… but a bit April 2023 (The Upside Everyone’s Missing in European Banks).

We have a higher standard though.

It’s good to enjoy the multi-year massive upside, but we also have to be on the hunt for the new, new.

And we found it.

What will everyone be excited about in 2026?

It’s China, and in particular Chinese insurers.

Our horse is Ping An (Ticker:2318 HK, $PNGAY)

Valuation

Wells Fargo + United Healthcare

The Back Story (Discovery’s Vitality)

China IRA’s.

Price Target (HK$ 105/share)

The Bear Case

Earnings Model & Reference Material

Valuation

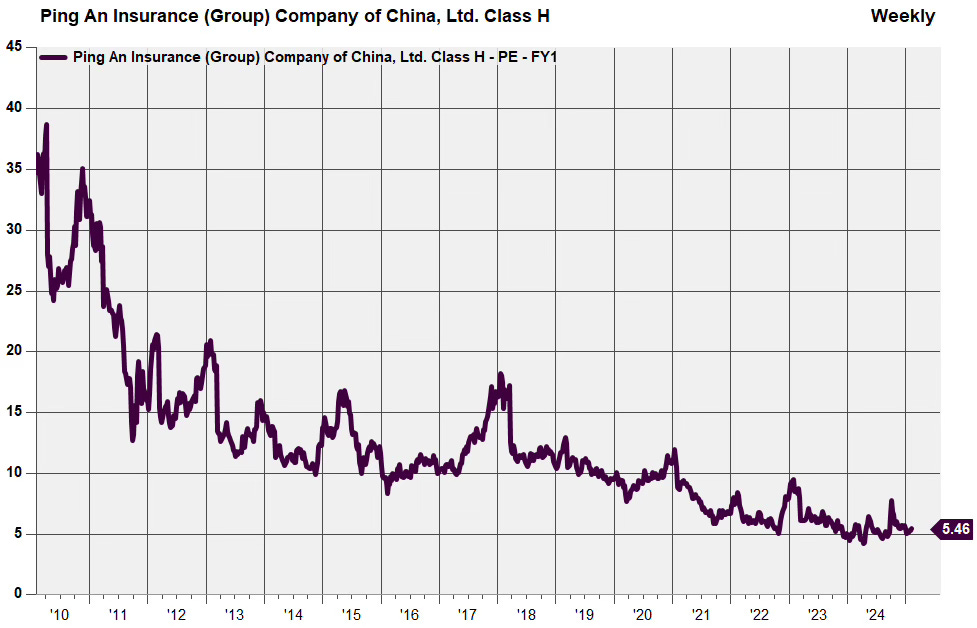

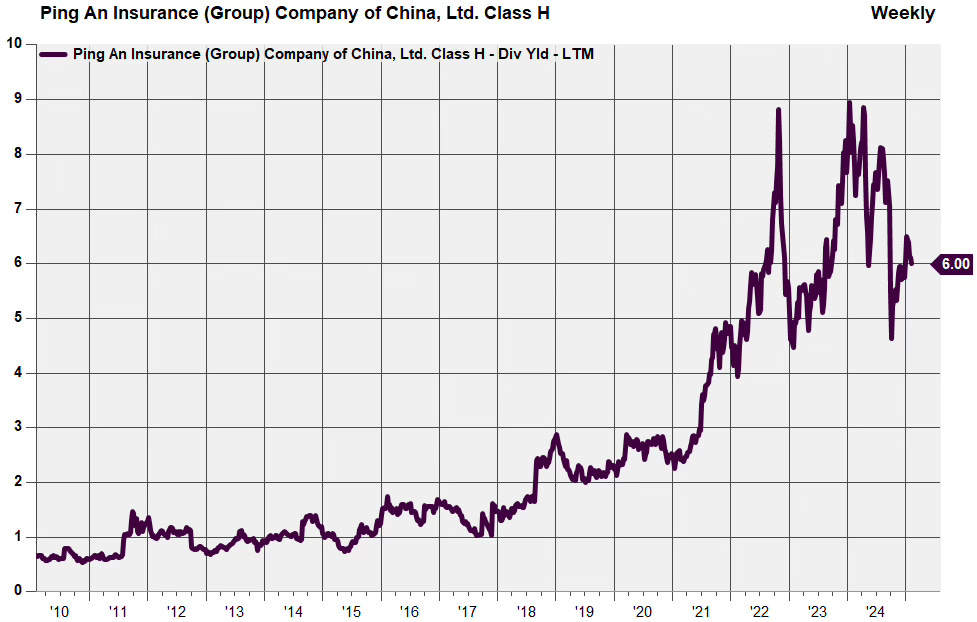

A few valuation charts to whet your appetite.

P/E of 5.5x 2024 earnings. In a moderate bull market Ping An trades in the 10-15x range.

A dividend yield of 6%, one of the highest ever, while Chinese 10 year bond yields are 1.6%.

Wells Fargo and United Healthcare

If you had to describe Ping An, it would be ‘What if Wells Fargo and United Healthcare had a baby, in China?’

Ping An is a $120bn market cap Chinese bancassurer (Bank + Insurance).

#2 largest life insurance company in China, behind China Life.

#2 largest property and casualty insurer behind PICC.

#13th largest bank in China.

Ping An Asset management has $775bn in AUM. Largest non-state owned asset management company.

240 million retail customers. That’s a lot.

When I say Ping An is WFC + UnitedHealth (and they use this description themselves) I say it to mean they are highly focused on retail financial products and leading in the technology, and distribution of these products at scale. The strategy is to grow products per customer, which was always a big Wells Fargo metric.

The Back Story. Not a sleepy Chinese insurer.

Ping A scores well in the Global Factor Model, but that’s not the real reason it stands out for me.

I’ve been hearing about Ping An for years. And it goes back to when I was investing in South Africa.

I used to own shares in Discovery, a highly innovative South African insurance company. Discovery’s great innovation is that insurance premiums for life and health should flex based on your activity. If you sign up for their Vitality product it tracks how many times you go to the gym, how much broccoli you buy at the store, whether you get your blood pressure checked, etc. This all creates a points score which affects the cost of your insurance. Live a healthy life and your health insurance will be cheaper. It’s an extremely popular product in South Africa and they’ve been franchising the technology all around the world.

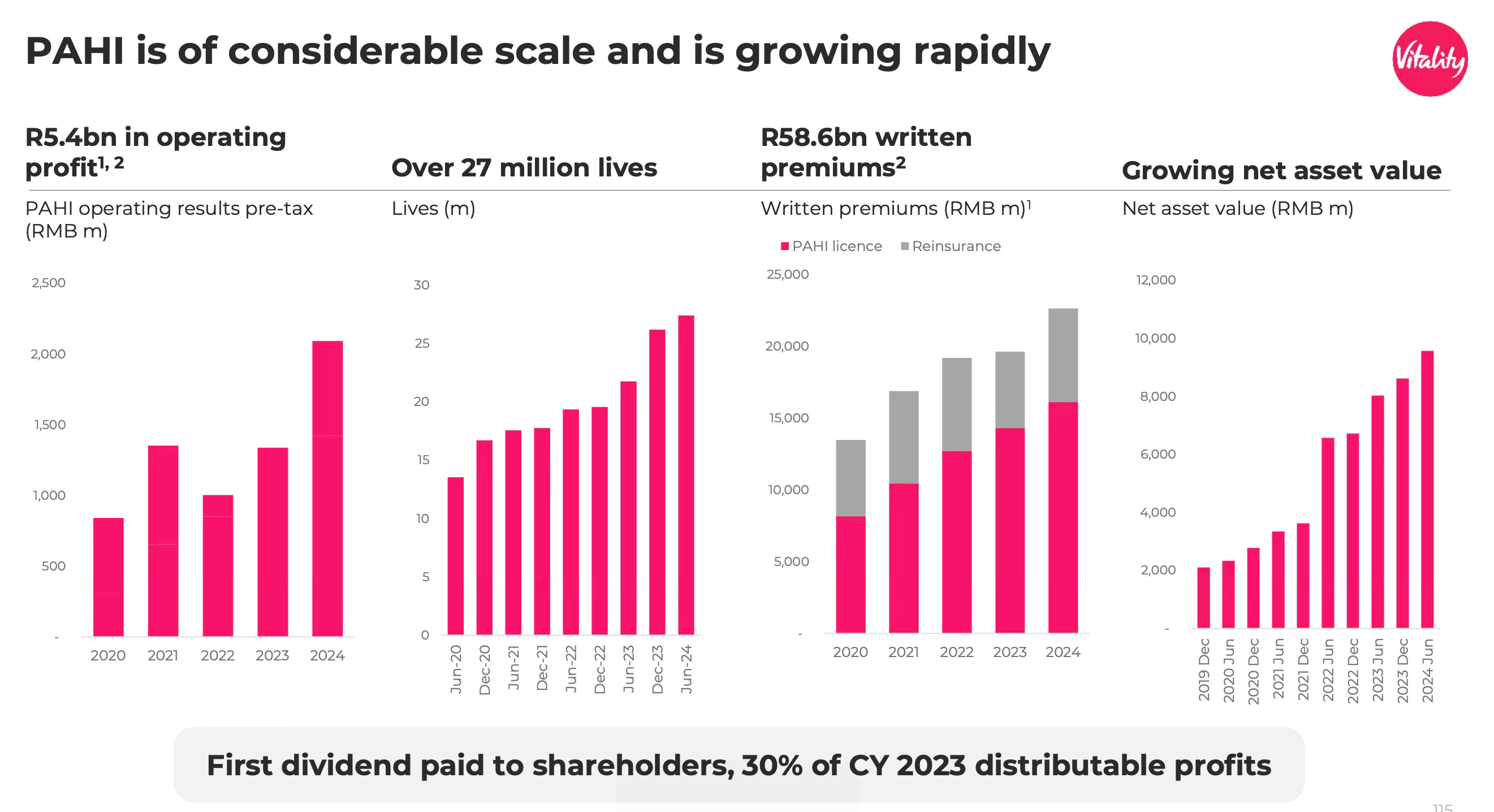

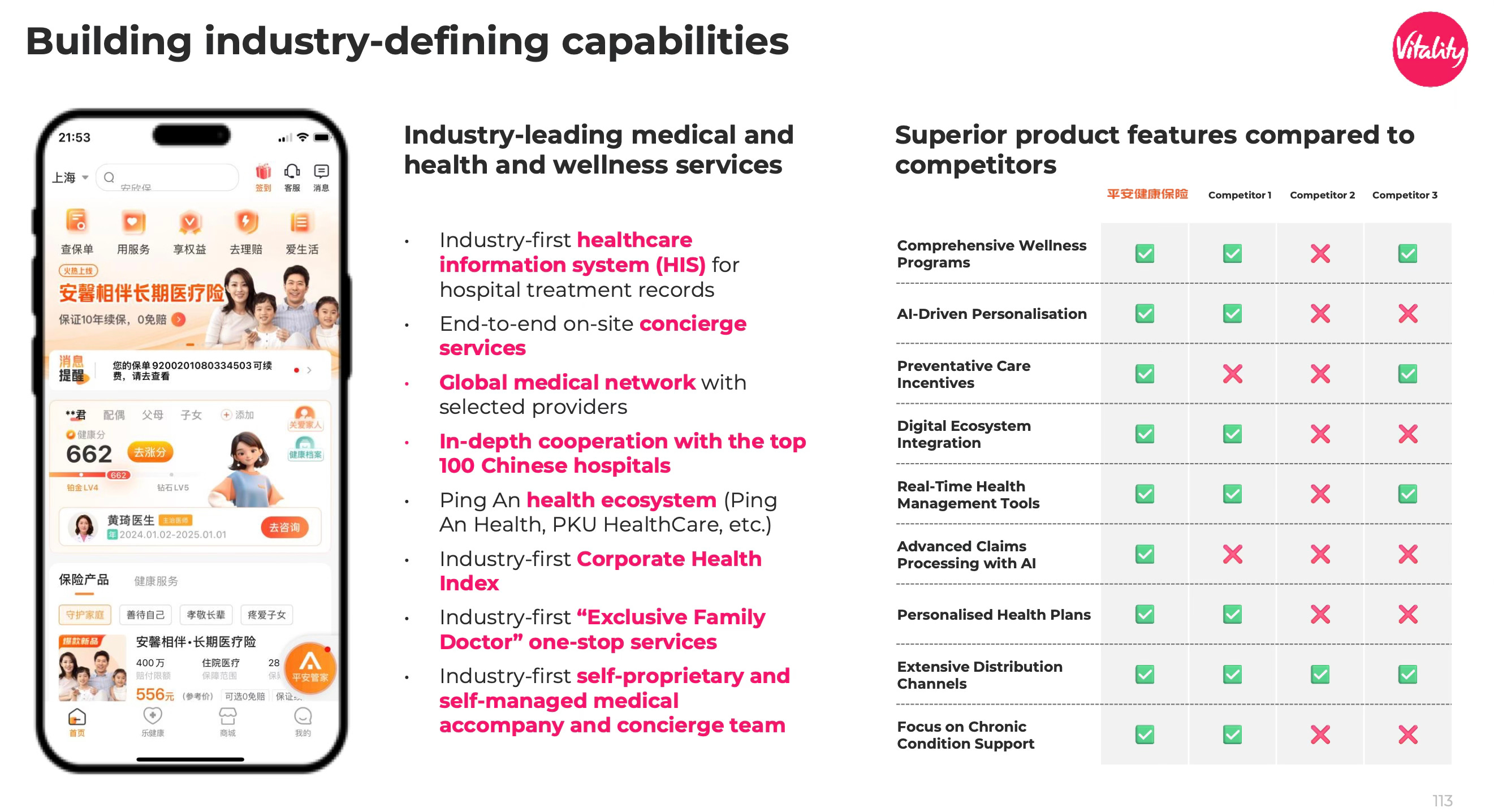

Ping An also liked this product and partnered with Discovery on Ping An Health (PAHI) with Discovery taking a 25% stake in the business. Ping An sees massive growth potential in Chinese private health insurance, but wants to also provide innovative technology driven products.

When I would visit Discovery in Joberg we would talk a lot about Ping An and their experience working with them. Despite all the growth there was no cash coming out of the partnership, so I would always ask if they were being scammed, or if Ping An had found a way to recognise the profit in other parts of their business.

Discovery’s main complaint was that they had trouble keeping up with Ping An. Ping An had big ambitions for health insurance and wanted to rapidly scale the business across China. For them it was a small business and they needed it to get to a much larger scale to be meaningful. Ping An had deep pockets and were happy to reinvest everything for growth. Discovery would have liked a bit less growth and more dividends from the partnership. But there was never a problem that Ping An was ripping them off, or that Discovery resented working with them. In fact Discovery said the idea flow was two-way. Every time they went to Shenzhen they were learning new ways Ping A was using technology across the entire healthcare ecosystem, and not just in insurance.

In summary, not a sleepy Chinese insurer. (Ping An Brain)

China IRA’s

Ping An is at record low valuations, has a 6% dividend yield, is highly innovative and growing, but there’s another kicker.

Chinese pension reform. Individual retirement plans.

This started as a pilot scheme in 2022, but in December last year the plan was officially rolled out nationwide.

Every citizen can invest RMB 12,000/year ($1,700) in a private pension plan.

The key detail is that Chinese can invest these pension funds into stock market index funds, similar to IRA’s in the US. Yes, stocks.

The China Securities Regulatory Commission, has included 85 equity index funds into the product catalog for private pension investment, among which 78 track various broad-based indexes, while the rest track those generating higher and stable dividends. (Source)

I’m sure these products will get off to a slow start, but eventually Chinese, like Americans and Australians, will figure out how the best strategy is to max them out and invest in the stock market.

If 200 million Chinese (just a guess) invest $1,700/year into the stock market it’s $340bn/year in inflows.

And what happens when the Chinese regulator increases the annual amount up to $5,000/year?

This is going to turn into a big growth story and investors will be looking for the plays on this.

Ping An with their combination of bank distribution, mobile apps, insurance agents and funds management business is going to hoover up the fund flows. In 5 years this will be a big business, but more importantly it will give Ping An a new growth driver which will rerate the P/E from 5.5x to over 10x (at least).

And what if the P/E went to 15x? UNH trades at 18x….

Oh, and how many stories have you read about Chinese IRA’s? Zero.

A monumental reform just happened, which is part of China building a consumer focused economy and nobody is paying attention.

Price Target HK$ 105/share (+133%)

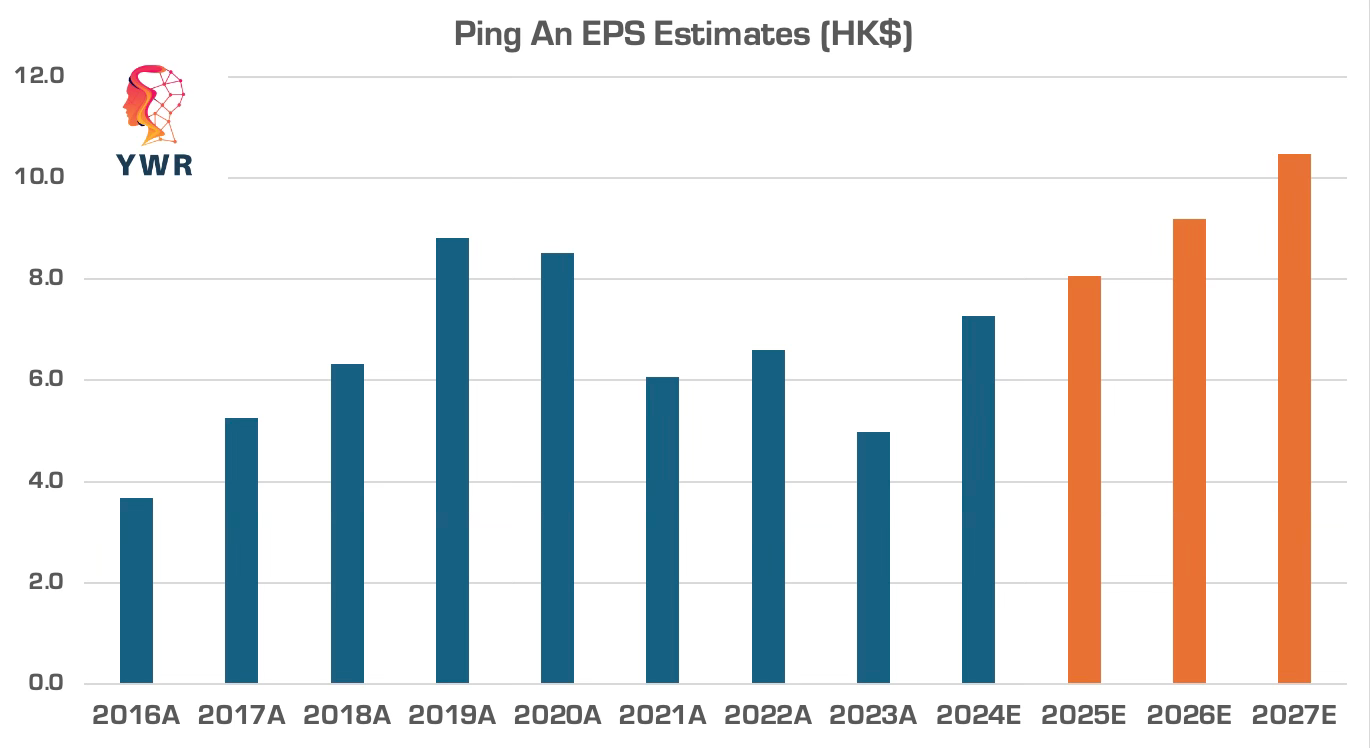

My scientific price target is that by February 2027 (2 years) the Chinese economy will be recovering, the stock market will be performing, sentiment will have improved, and Ping An will trade on 10x my estimated 2027 EPS of HK$ 10.5/share (RMB 10/share).

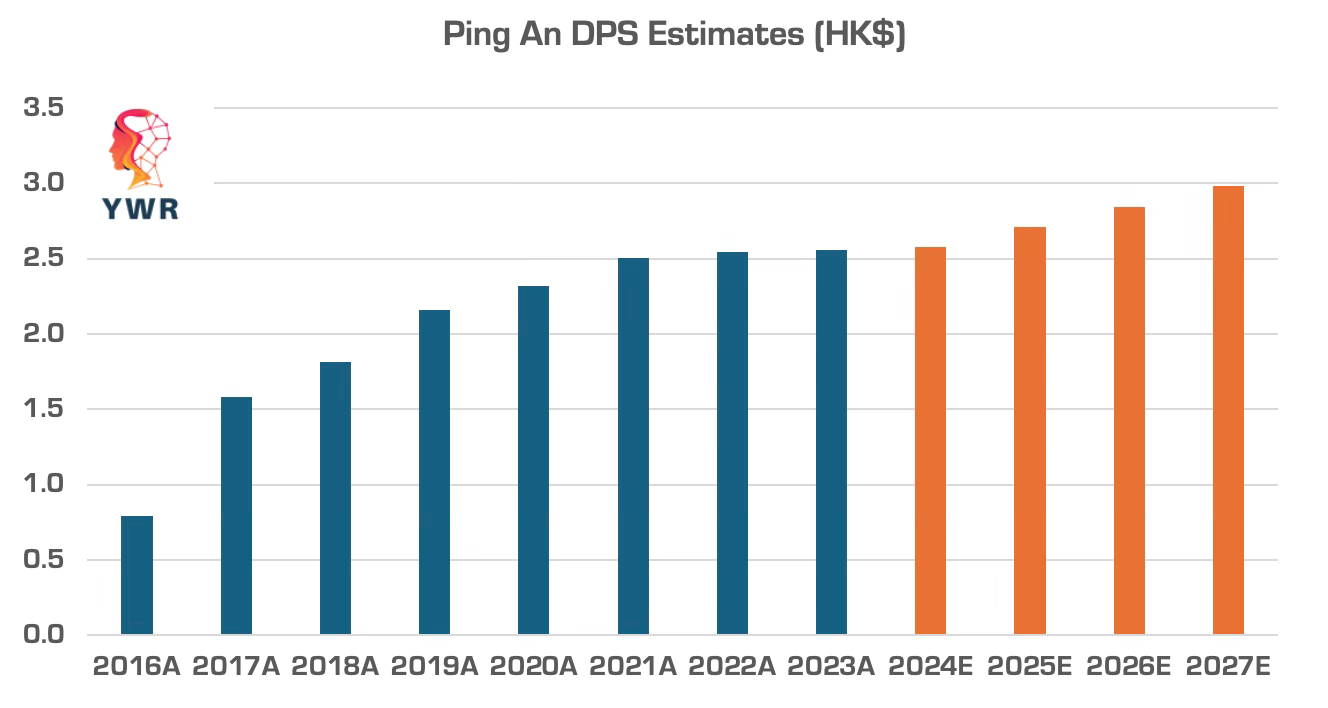

Ping An has been consistent about growing dividends even though profits declined in 2023, so I expect DPS growth to be slower going forward. Our $105 price target would be a 2.8% dividend yield based on my 2026 DPS estimate of HK$ 2.8/share.

Potentially, our total return over the next 2 years is +133% on the share price appreciation plus another 11% from 2 years of dividends (2024 and 2025).

+ HK$ 60/share ($45 to $105)

+ HK$ >5/share in dividends (YE 2024, 2025 + 1H 2026)

Total of $65/share

A word on my forecasts. It’s difficult/impossible to model life insurance companies. So I make a big simplification that Ping An is in the business of collecting retail assets in whatever shape or form (life insurance, asset management, bank deposits) and earning a spread on those assets.

My forecast is this return on Ping An’s constantly growing client assets (ROA) improves to 1.2% by 2027 from the low of 0.8% in 2023.

The Bear Case

It will be a headwind for Ping An’s earnings if Chinese bond yields stay this low for the next 5 years or do a ‘Japan’ and go lower to 0%. To some extent this is price and why Ping An is trading at the lowest valuations ever, but if yields

Ping A will have to again reset their life insurance earnings lower (which they already did in 2023). Ping A bank will also continue to struggle with lower interest rates, similar to European banks post GFC, although NPL’s won’t be a problem.

If it’s hard (for investors) to imagine US yields going higher, let alone Chinese yields, why own a company which doesn’t like low yields?

Maybe, if we are bullish on China it’s better to stick with Chinese tech stocks.

Here’s what I think:

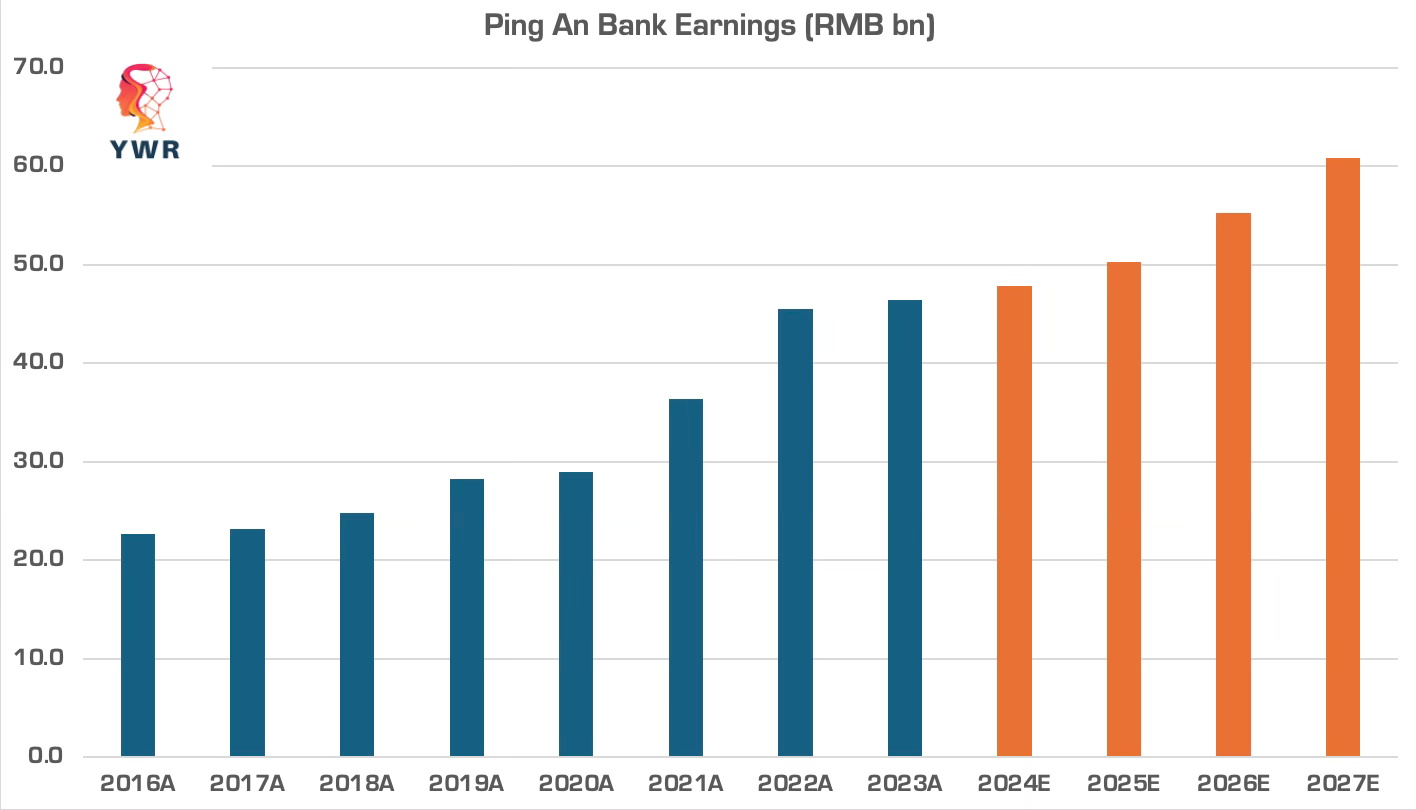

Traditional yield based life insurance isn’t the only growth driver. Ping An’s bank has been consistently growing with NPL’s of 1%.

Ping An’s consistent customer growth offsets some of the interest rate pressure.

P&C insurance was weak but now recovering and is a small positive offset to the life insurance.

Ping An is diversifying out of traditional yield based life insurance into asset management, health insurance and the whole health ecosystem (buying hospitals from troubled real estate developers). In short, Ping An isn’t standing still waiting for yields to go up.

The stock is too cheap. Who knows where interest rates go? We are getting paid almost 6% dividend yield to own the best in class diversified financial service business in China.

Summary

There are risks to everything, but for me the risk reward on Ping An is attractive and it fits my strategy of owning a best in class business with a high dividend yield which can appreciate over 100% in the next 3 years.

Earnings Model and Reference Material

Below are links to:

YWR Earnings model

E&Y report on the new IRA scheme

Oliver Wyman report on how Chinese insurance can 6x in the decades ahead.