YWR: 7 Reasons Rates go Higher

Why did the Israelis know to prepare for a Zombie attack?

Why were they the only ones who saw it coming and prepared?

10th Man Theory

The problem with most people is they don’t believe something can happen until already has.

It’s not stupidity or weakness. It’s just human nature.

So we decided to make a change.

If 9 of us look at the same information and come to the exact same conclusion. It is the duty of the 10th man to disagree. No matter how improbable it may seem.

The 10th man has to start digging with the assumption the other 9 are wrong.

Since everyone assumed this talk of Zombies was cover for something else, I began my investigation on the assumption that when they meant Zombies, they meant Zombies.

Mossad Chief, Jurgen Warmbrunn, World War Z.

The 9 Men

What is that idea in the market on which everyone agrees? That thing where everyone looks at the data and comes to the same conclusion. What do the 9 men think?

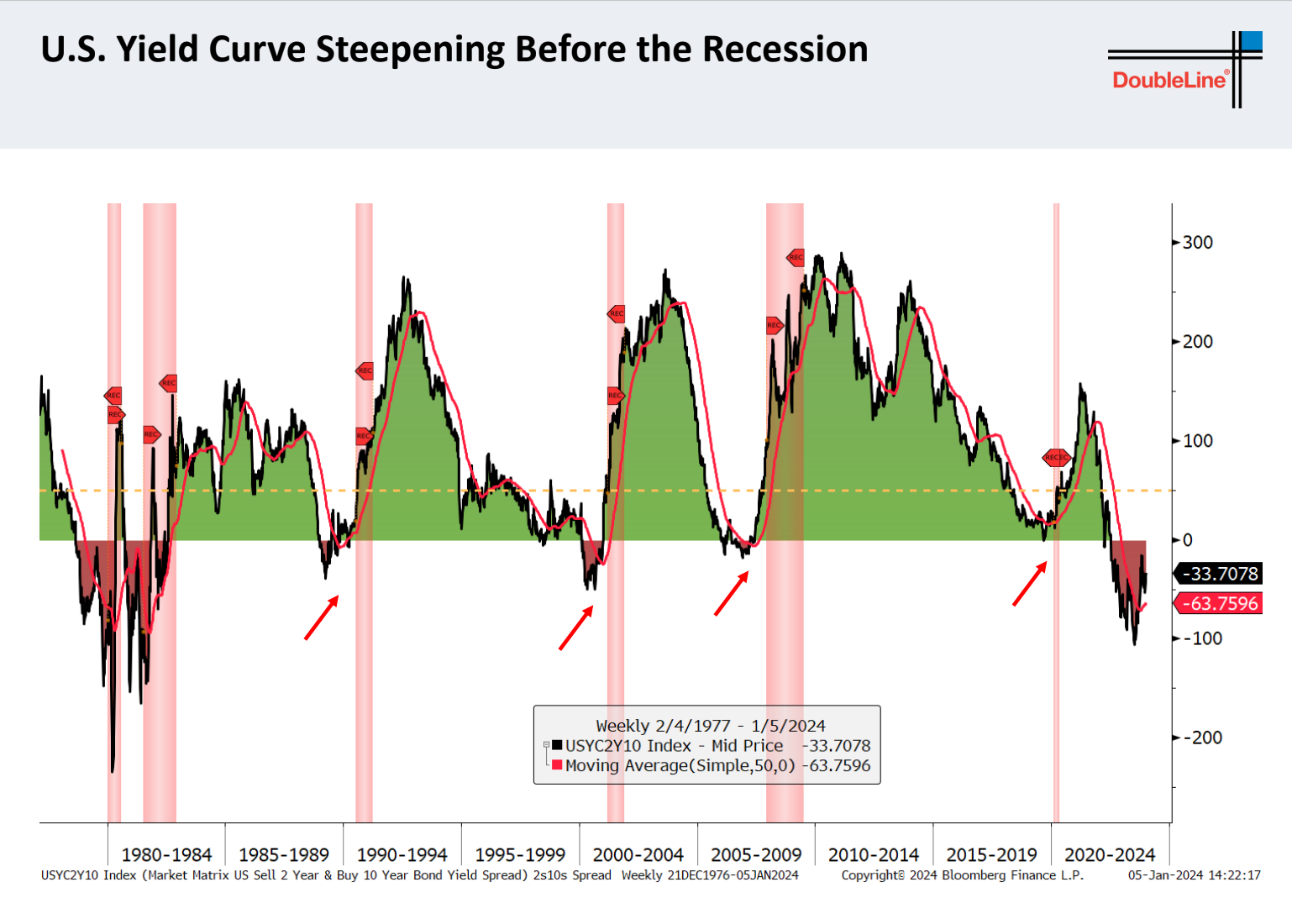

It’s that interest rates go lower.

You see it everywhere. It’s Jeff Gundlach in his ‘Just Markets’ presentation where he is predicting a recession and sharp rates cuts.

It’s Chen Zhao and his forecast that we are going back to pre-pandemic interest rates. Inflation will go sub-2% this year and could even go negative! The Fed will mechanically have to cut rates.

Chen’s view (and it’s conventional) is that goods deflation has already fallen. The pandemic supply problems are over, and there is no price pressure coming from commodities or China.

The last shoe to drop is rental inflation. It’s the only thing keeping CPI above 2%. And that is about to fall too. It also might go negative. It makes sense. We have a record amount of multi-unit housing under construction.

All of it makes perfect sense. In fact it’s the thing all fund managers agree on for sure. It’s not 9 men, it’s 249. They all look at the same charts, and come to the same conclusion.

The bond market too has priced in 4 rate cuts for this year. All that’s left is for Powell to do it.

Which is why investors are sure bonds will be the best performing asset in 2024.

Jurgen would say this is a risky set up.

How could everyone be wrong? No matter how improbable it seems.

What would be the case for a 6% Fed Funds Rate?

YWR readers… we need to do our duty. We need to step up and be the 10th man.

For the sake of our fellow investors.

7 Reasons interest rates go higher.

How does it happen?

How do we get a situation in 2024 where inflation isn’t falling, and the Fed realises CPI has been above target for 3 years and they actually need to raise rates higher? To 6%.

It’s a combination of some or all of these 7 trends coming together. And I thank Our Man in NYC for meeting up in London to help put it all together.

#1 China - we discussed this last week in The Surprise Market for 2024. China’s provinces are gearing up for growth. You have the 2nd largest economy, and the most commodity intensive, pulling every lever to have a big year. Yet, everyone thinks Goods Inflation stays tame. This is a yellow/red flag that commodity driven inflation and global growth could surprise to the upside.

#2 Commodities - low oil inventories, low copper, supply chains getting disrupted, wars breaking out, Saudi production cuts. As discussed in Max Max Scenario and The First Quantum Situation for a mix of reasons (low commodity prices, shareholder pressure, ESG) miners, oil companies, and service providers are not investing in new capacity. If for some reason global growth turns out higher than we expect, the commodity supply chain will tighten quickly.

#3 Absolute level of wages - another consensus view is that sometime this year unemployment will rise and wage inflation will crash back below 2%. Gundlach and Chen have the same chart on this. And they point to small signs the labor market is loosening (falling quit rates).

But Chen and Gundlach are missing the point on wages. And any worker can point it out to them, or they might realise it themselves next time they pay $7 for an egg McMuffin at McDonalds.

When it comes to wages, workers are still massively offsides from what happened the last 3 years.

Since 2020 house prices are +40%, and mortgage rates have gone from 3.5% to 6.5%. That’s 40% more house price and 2x more interest.

In 2020 a first time homebuyer needed $49,000 to buy a house, which was fine because the median income was $54,000. But in 2023, with higher prices and higher interest rates, the required first time buyer income was $87,000, but the median income had only risen to $59,000.

So if you are a worker asking for a wage increase, because you are sick of never being able to do anything, sick of living in the same small house, and your boss tells you, sorry, the most I can give you is 3% and that’s fair, because that’s the rate of inflation, you say fooook that. 3%? It needs to be 30%. That’s why I wrote 30,000 reasons wages aren’t falling.

So wages are too low on an absolute level and it’s a pressure cooker. The thing keeping it in check is workers aren’t sure how much leverage they have, and the narrative is that the economy is weak. But that could change.

#4. The relationship between debt creation and prices has changed. For 45 years the US could add trillions of debt and it wouldn’t generate inflation. You can see it in the scatter plot below. Debt grows at log scale while CPI growth is linear. Then in 2020 that 45 year regression line changed. It’s what we talked about in Phase Transitions. This chart says be careful if you are adding a lot of debt, this time around it might be more inflationary than you expect. Next slide please.

#5. US Government debt growth is going vertical!

It doesn’t get enough attention just how much debt the US government is issuing. We are through the pandemic, but debt growth is still pumping. It’s why the Fed can raise rates 550bps in a straight line and nothing happens. The economy doesn’t flinch. The positive view/take on this is that on a % change basis the growth rates should moderate in the years ahead. Maybe. We will come to a reason why that might not happen in point 7, but for now I want to point to the lacklustre growth in bank loans and corporate bonds.

My fear is this. What if the government is stimulating the economy so much, that it is about to spill over and bank lending and corporate issuance join the party too? What if all three start going vertical? And then think back to the scatterplot in Point #4 on how CPI is been reacting to debt growth. But what would make banks start to lend? I thought we had a banking crisis.

#6.What do you do with EUR 250 billion? YWR readers know I’ve been flagging the build up in excess capital at European banks and how it reaches EUR 255bn by 2025. It’s enough capital for EUR 1.9 trillion in new lending. But European banks are timid and unsure about the economy, so they are playing it safe. But one thing you see from banks like Commerzbank, is that they fancy themselves experts on renewable energy project finance. That is one space where they are comfortable lending globally. So keep that in mind.

Meanwhile, US banks are still cautious about office exposure and the occasional regional bank blowup, but my prediction is the large banks made enough provisions in 2023, and will be positively surprised in 2024. European banks definitely, but US banks might also be ready to lend again in 2024. And so bank lending joins the debt growth party. Which brings us to #7. The trend that connects the dots and brings it all together.

#7 The Biggest trend nobody is talking about.

Well, actually its 6 trends coming together across 8 different industries. Which is why lots of companies can see their own little part of it, and how they are benefitting, but don't know how to articulate what is going on.

Except for one company. They do the best job of telling the story, which is why smart investors are following their every word.