YWR: China Cash Dragons 1H 2024 Earnings Review

Time to review the 1H earnings from our Cash Dragon theme.

It’s good to stop talking macro and get into the details of actual corporate earnings.

We’ll start with the best results (Tencent) and work down the list from Alibaba to Baidu and Las Vegas Sands.

I’ll keep it succinct and to the point.

All the updated YWR earnings models are available at the bottom of the post and at the www.ywr.world Data & Models tab.

Tencent (700 HK)

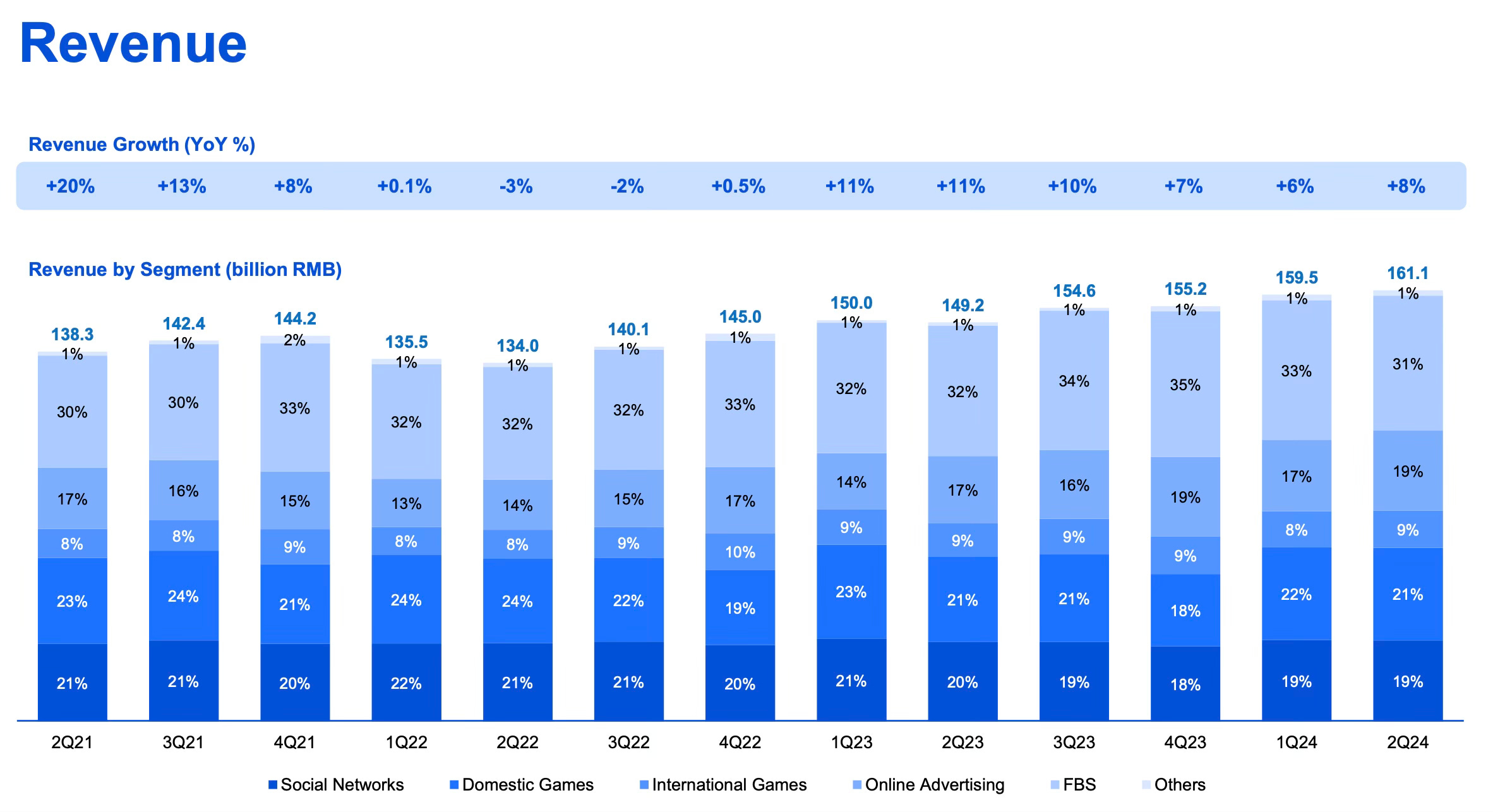

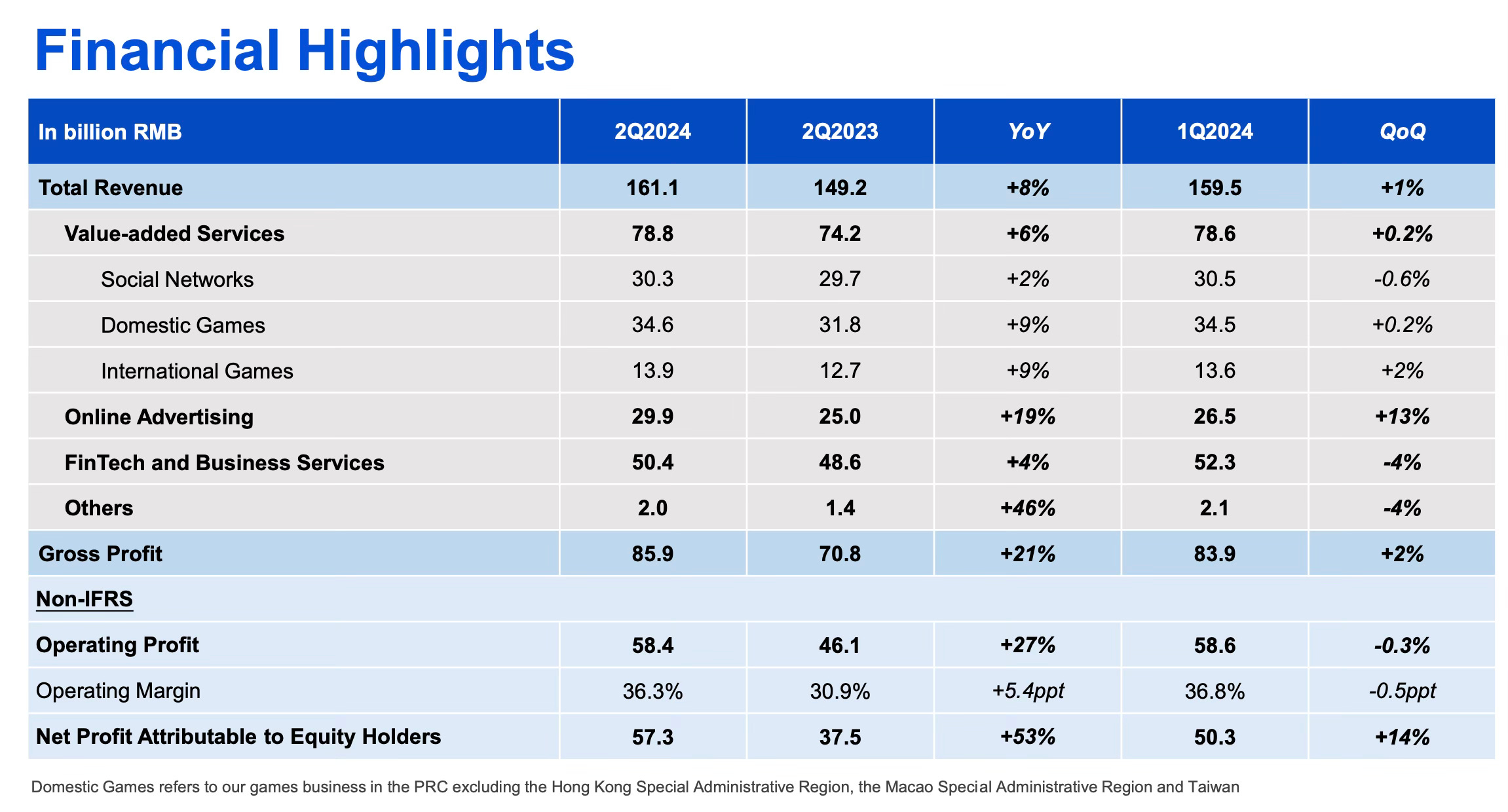

Total revenues hit a new all time high, but the growth rate is single digits. The business mix is shifting, with less ‘Social Networks’ and more ‘Advertising%, which is fine. Facebook is 100% advertising.

Domestic and International game growth is back to 9%, but the real growth business is online advertising. Fintech revenue growth is suprisingly low at 4%, but management says it is because people are keeping more money in their WeChat wallets, which hurts high margin cash out fees. So long term this is positive.

But the real story is how Tencent is managing costs. In Q2 they turned 8% revenue growth into 27% operating profit growth and 53% net profit growth. It’s encouraging that Tencent can grow operating profits 27% while overall growth in China is depressed.

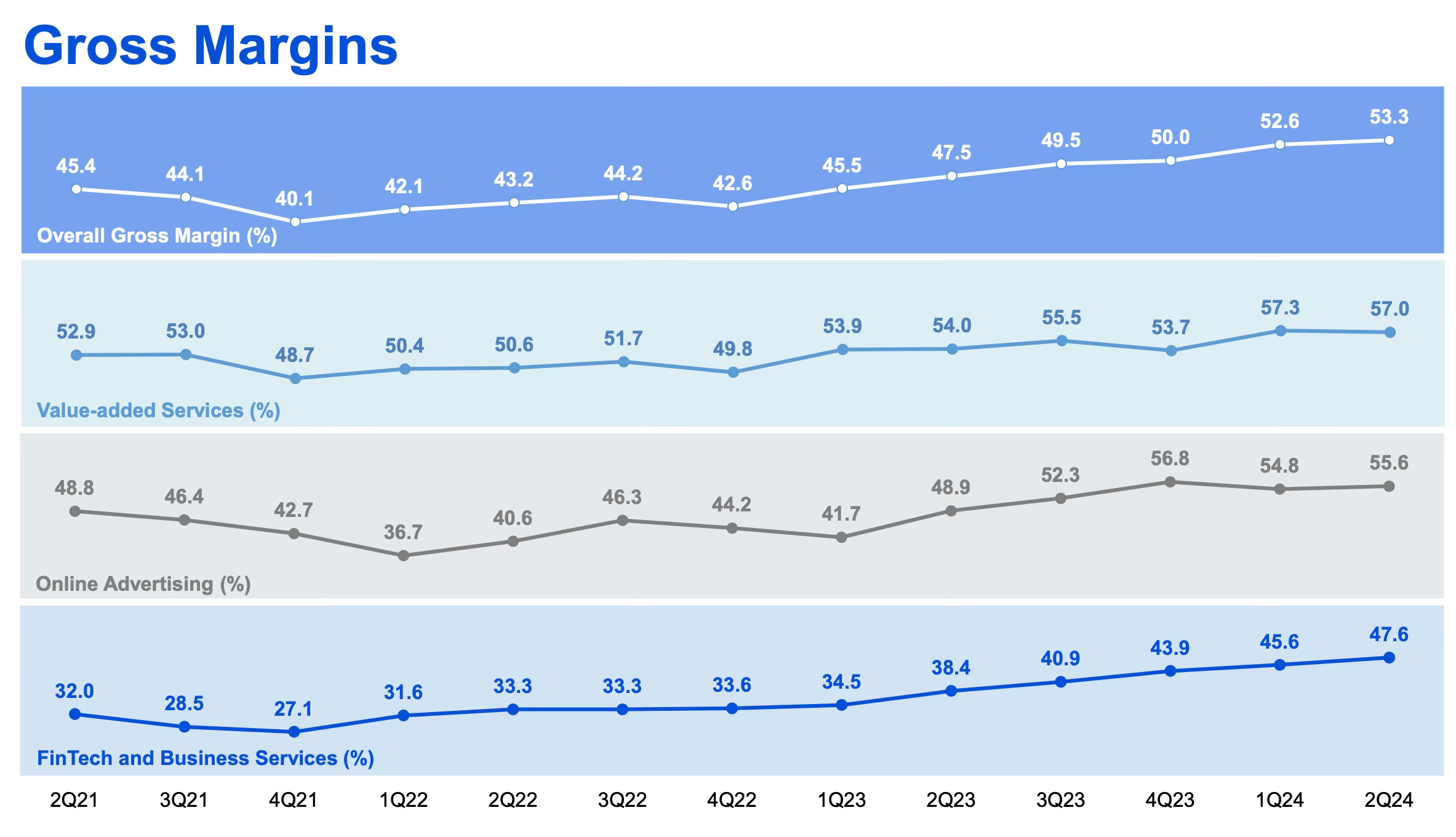

Gross margins have been improving in all business lines. Management says they are focused on high margin revenues.

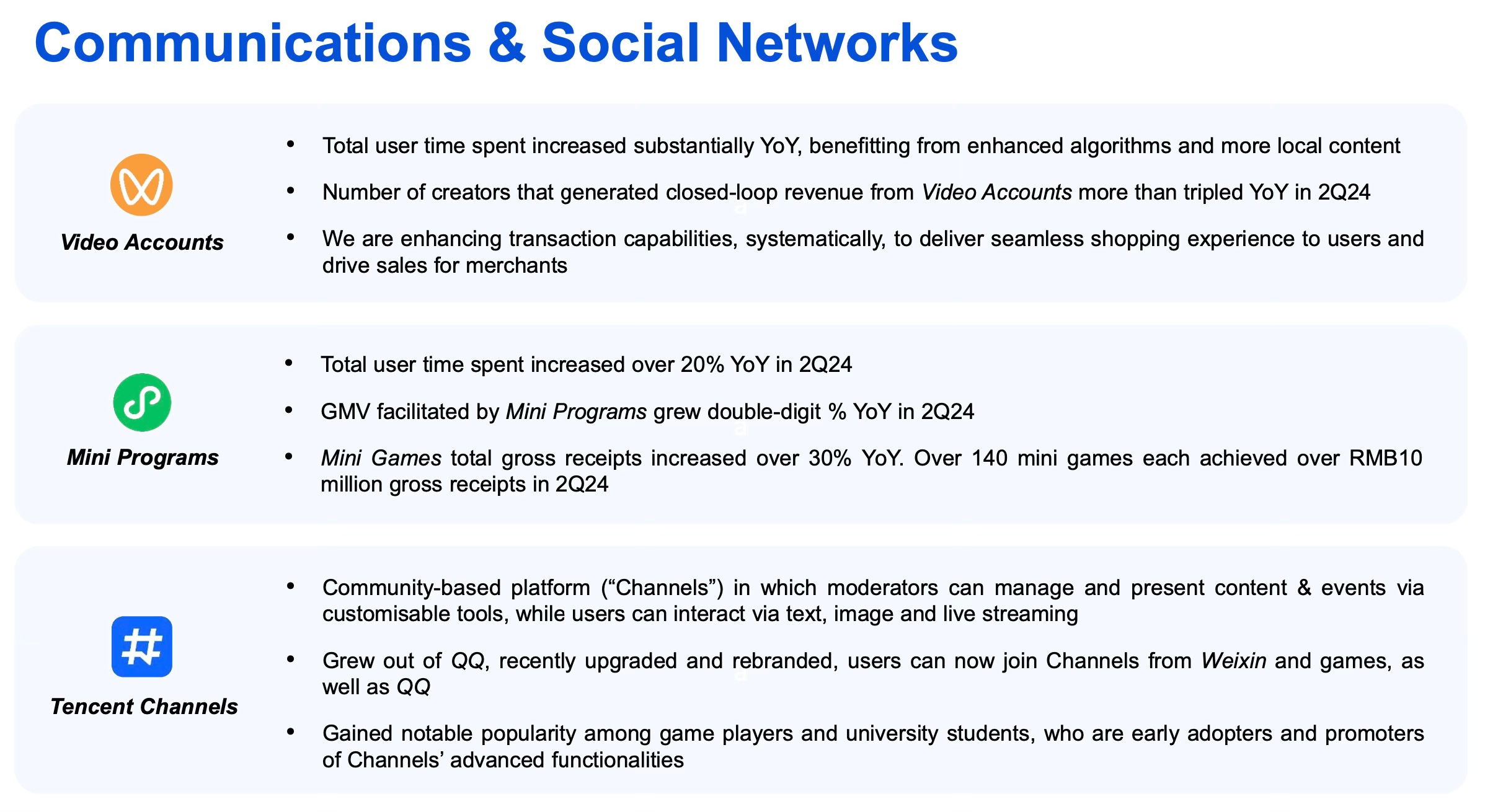

I like the line in the slide above about Mini Programs where it says ‘gross receipts increased over 30%’. Our multi-year thesis in Tencent’s Path to HKD$ 1000/share is that the Mini-Program super app model will grow outside of China.

Overall, these were good results and the market is happy. The EPS estimate trend for Tencent is finally trending positively.

YWR continues to own Tenecnt and next quarter would like to see the Fintech business accelerate.

Alibaba

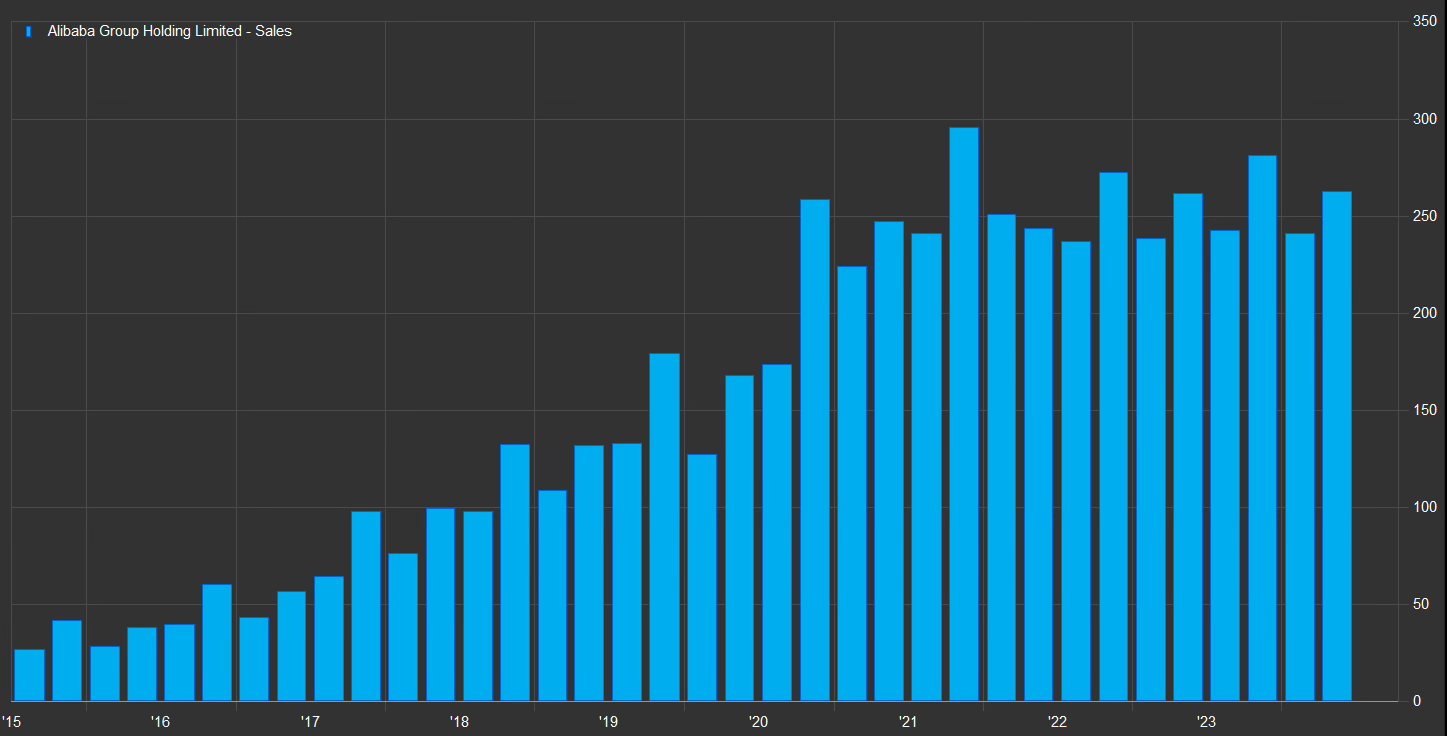

Like Tencent, Alibaba is growing revenues, but it’s single digit growth.

Alibaba quarterly revenue chart.

Alibaba’s Taobao business, the Amazon of China, is struggling with a cautious consumer and competition from PDD and JD.com.

Besides revenue growth Alibaba’s other problem is getting expenses right-sized to the lower growth rate. Alibaba’s results the last 2 years have also been full of ugly goodwill and investment impairments below the line which made their quarterly earnings a mess.

Back in the heydays of 2016 Aliaba was investing multi-billion $ stakes in everything ($4.6bn for a 20% stake in Suning, $1.25bn into Ele.me, $1bn into Lazada, $1bn into Koubei) and launching lots of exciting new initiatives from cloud computing to logistics and media.

From the 2016 investor day:

The company has come to see it as increasingly important to transition from a pure e-commerce play to an internet company with a broad ecosystem of services including cloud computing and big data, online payments, logistics and marketing. Alibaba has also made big moves into the media and entertainment sectors, further expanding the ways it can engage consumers.

When considering whether or not spending 10 percent of Alibaba’s market cap for leadership positions in these sectors and markets, as well as buying back $5.1 billion worth of stock, was the right move for Alibaba, Tsai called it “an absolute no-brainer.”

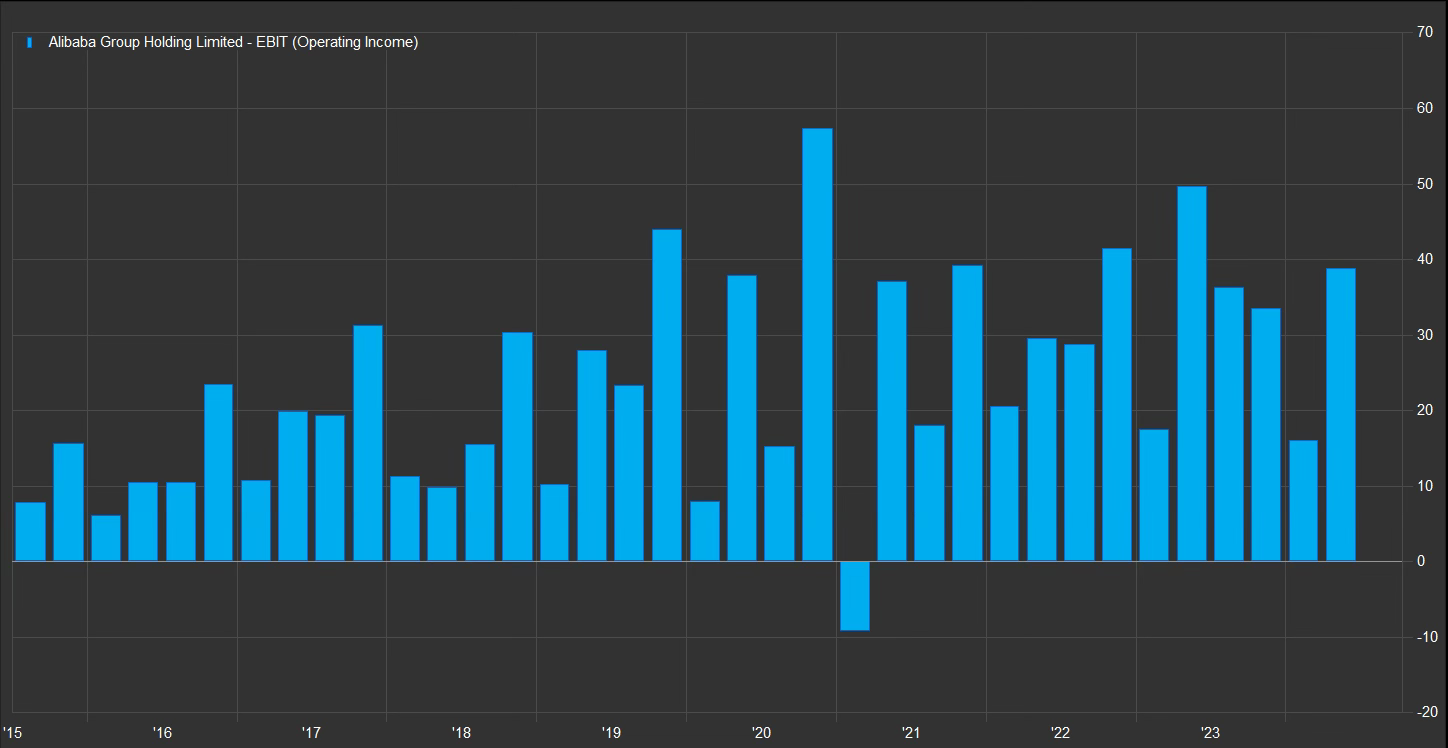

All those ‘no-brainer’ investments from 2016 have been money losers with huge write downs. But I expect we are through the worst with the one-off impairments.

In the chart below you can see the quarterly EBIT line is starting to grow and regain consistency.

Alibaba’s Cloud computing business was a bright spot in the results. Alibaba’s Cloud business has historically not been profitable and a disappointment compared to the initial hype. Now with AI, things are improving.

Looking to the medium- and long-term, we're confident that Alibaba Cloud's overall revenue, excluding Alibaba consolidated subsidiaries, will return to double-digit growth in the second-half of the fiscal year with gradual acceleration thereafter.

Source: Q1 2025 Call.

Revenue

Adj. EBITA

2023

25,065

916

2024

26,549

2,337

Yoy %

6%

155%")

Management is also focused on turning around all the money losing business they got into like Asian e-commerce.

International e-commerce.

International commerce retail

International commerce wholesale

Revenue

Adj. EBITA

2023

17,138

4,985

22,123

(420)

2024

23,691

5,602

29,293

(3,706)

Yoy %

38%

12%

32%")

Digital Media; another ‘great idea’ that is a money loser.

Revenue

Adj. EBITA

2023

5,381

63

2024

5,581

(103)

Yoy %

4%

N/A")

Alibaba realises they can improve bottom line earnings significantly just by reducing costs in these money losing businesses.

This past quarter's financial performance continues to demonstrate our strategy to revitalize growth in our domestic e-commerce and cloud segments while reinforcing our leadership position. At the same time, we are improving the monetization and operating efficiency of our loss-making businesses with the goal of achieving sustainable business growth and profitability.

Source: Q1 2025 Call

And Alibaba continues to buy back shares.

Shares repurchased (Mn ADSs)

Outstanding shares (Mn ADSs)

sep. 30,

2022

$2.1

24

2,626

Dec. 31,

2022

$3.3

45

2,585

Mar. 31,

2023

$1.9

22

2,566

Jun. 30,

2023

$3.1

36

2,549

sep. 30,

2023

$1.7

19

2,531

Dec. 31,

2023

$2.9

37

2,499

Mar. 31,

2024

$4.8

65

2,434

Jun. 30,

2024

$5.8

77

2,378")

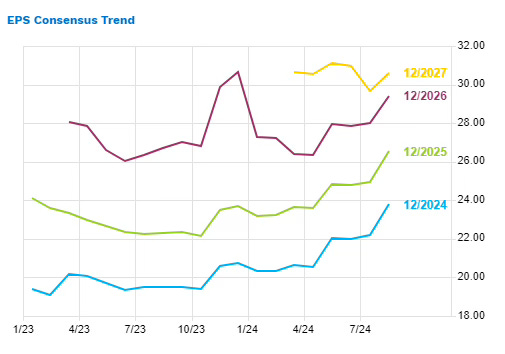

In conclusion Alibaba’s Q2 earnings were positive and analysts are raising estimates, which hasn’t happened in years. YWR continues to own Alibaba.

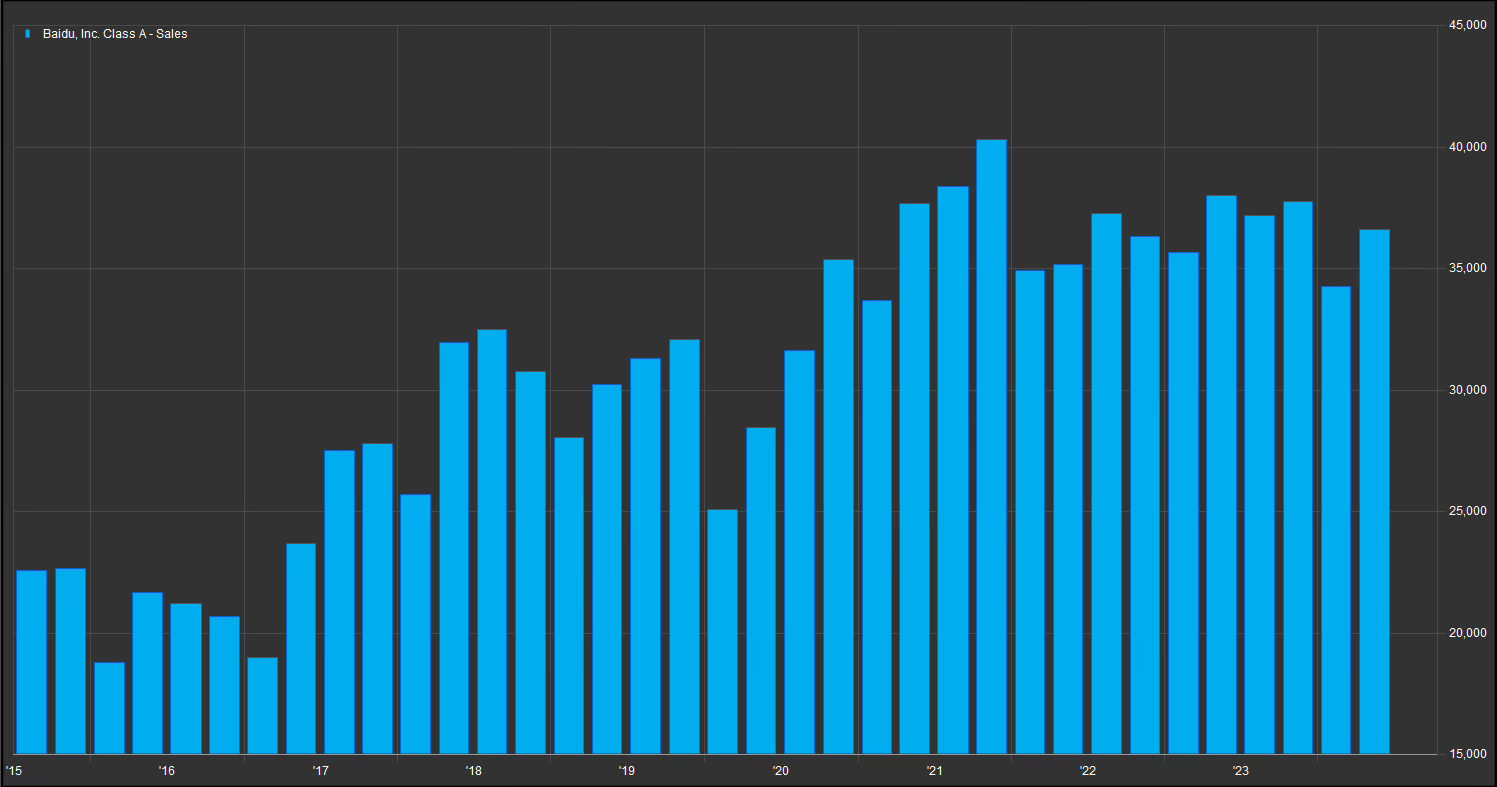

Baidu

The market is killing Baidu after Q2. To me it seems overdone, beating a dead horse and missing the upside around the corner.

And somehow Baidu’s problems monetising AI has not been noticed by the VC’s piling billions into the latest Chat GPT round.

Unlike Tencent and Alibaba, Baidu’s revenue growth was negative in the quarter ( -1% yoy). Baidu’s core business, online search, is in decline, while the ‘Others’ segment, which includes Cloud computing, is growing.

Baidu has reacted to its stagnant revenues by cutting expenses. Quarterly EBIT is near an all time high. But you’d never guess it from the share price.

The concern for investors is that Baidu’s core business (paid search) is in decline and the company hasn’t figured out how to monetise it’s leading Ernie AI model.

CEO, Robin Li, is very open about the challenges of what he calls ‘The Hundred Model War’, which is the fierce competition amongst AI models in China.

Despite the near term pressure, we remain confident in our direction and the potential of GenAI and foundation models. As we move into 2024 we are happy to observe a significant change as Baidu is scaling AI to address real world problems and generate value.

Central to this effort is making ERNIE affordable and accessible. I'd like to highlight key elements of our progress. The scaling of AI is accelerating at a breakneck pace, reflecting the value that ERNIE creates for people and for business alike. The most tangible benefit from AI comes from the adoption and use of applications built on top of our apps. Just three months ago, we announced that ERNIE handled about 200 million API calls daily. Recently, it surpassed 600 million calls. Over 1 trillion tokens are generated every day. To make ERNIE more affordable, we continue to expand our model portfolio and enhance our capabilities to meet diverse customer needs.

Li has been open that the growth in AI is changing the traditional paid search model (Google’s bread and butter). Instead of searching online, users are using AI agents to find information and it is hard to monetise this in the traditional business model. So online search revenues are falling while cloud revenues are accelerating as customers spend more on AI computing.

AI Cloud revenue reached RMB5.1 billion, marking a consecutive acceleration to 14% year-over-year growth, while sustaining non-GAAP operating profitability in the second quarter. The strong growth is mostly attributable to the following two factors: first, GenAI-related revenue continued its robust momentum, accounting for nearly 9% of our total AI Cloud revenue in Q2, up from 6.9% in the previous quarter. As more enterprises integrate GenAI and foundation models into their daily operations, they increasingly come tous, thanks to our reputation as China's most advanced and cost-effective AI infrastructure provider, and our excellent MaaS platform for model training and inference.

The second major driver of AI Cloud revenue acceleration is cross-selling of our CPU cloud services to our GPU cloud customers. In Q2, we continued to observe an increase in CPU spending among our GPU cloud customers. Our strong brand in GPU cloud is helping us win businesses in the CPU cloud industry. With revenue acceleration, AI Cloud business continue to deliver positive non-GAAP operating profit and improved margins.

The other way Baidu is monetising AI technology is through their leading robot-taxi business Apollo-Go. Apollo-Go is already active in Wuhan, but will expand into more cities in China. We need Kathy Wood to write a report on Baidu’s already operating robot-taxi business and value it at 1 TRILLION $$$’s!!!

Baidu is finding that AI changes everything and how you monetise it is different.

This AI transformation is not just about enhancing the traditional search experience. It's about redefining what search can do for users. In Q2, we have accelerated the pace to renovate Baidu Search using learning. New features such as AI-generative search result, interactive features within search, and ERNIE agents have been rolling out rapidly. This renovation has high potential, but is not something that will be completed in a short time. During this process, there may be a negative impact on revenue, but we are confident that the result will be a completely different new AI ecosystem, one that is much more versatile, productive and user-friendly. So it may take some time before we see a noticeable revenue contribution from the AI enhancements in our search product, but we are confident that focusing on creating long lasting user value rather than short term revenue will ultimately create tremendous value and drive sustainable revenue growth.

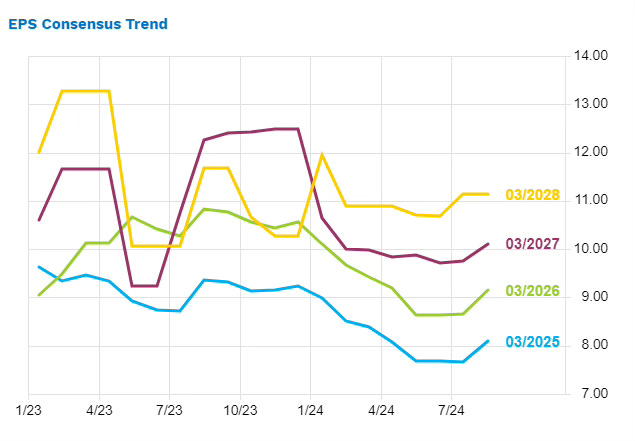

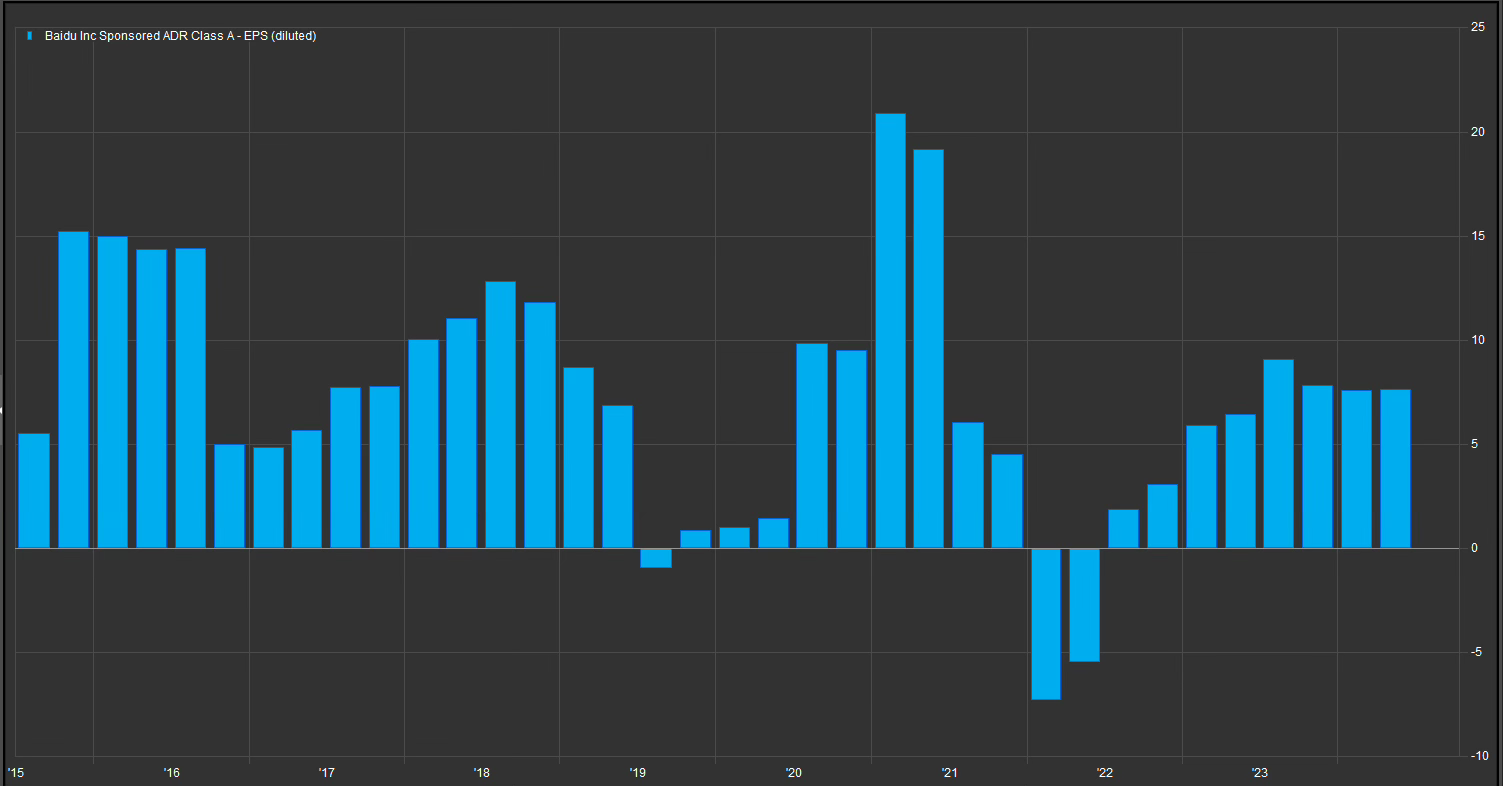

Meanwhile, Baidu’s trailing 12 month EPS is relatively stable at RMB 7-8/share.

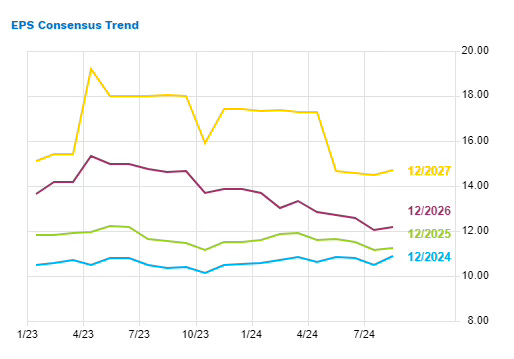

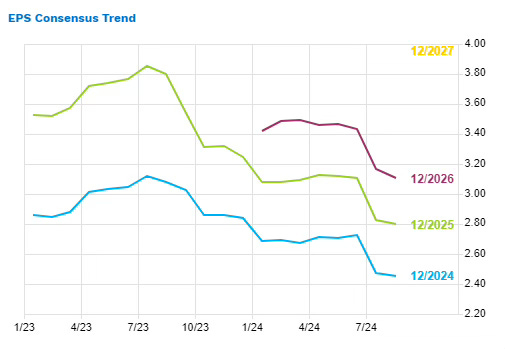

Analyst estimates are unchanged after the Q2 earnings, but we need a pick-up 2H 2024, or estimates will come down to RMB 8/share. YWR is at RMB 7.7/share for 2024 ($8.5 per ADR).

YWR is sticking with Baidu at 10x earnings for the ADR. Baidu has a leading AI model and ways to monetise the technology with either it’s existing businesses (online search, cloud computing, robotics-taxis) or with new businesses they invent along the way.

Las Vegas Sands

YWR owns LVS to play the long-term growth of wealth in Asia. Buying a luxury casino operator with dominant market shares in Singapore and Macau at a time when earnings are depressed seems like a good long-term play.

But Q2 results were not great and YWR reduced its 2024 forecast from $2.60/share to $2.37.

The recovery in Macau revenues stalled in Q2 and LVS continues to suffer from construction disruptions to its Macau casinos. Investors have heard the explanation before and that the disruptions will continue into Q4, but there is a sneaking worry, that maybe the construction disruptions are a cover for underlying weakness and revenues will continue to disappoint in 2025.

And will the Chinese consumer ever recover?

It doesn’t get any press from the China bears, but Macau gaming revenue is making new highs (+29% yoy) and mass win/visit is higher than ever at $779. Note this is mass gaming and doesn’t include high rollers.

On the negative side analysts didn’t like the weak Q2 visitation numbers.

And while LVS revenues in Macau grew 7.7% in Q2, there was no operating leverage. Macau EBITDA only grew 3.6%.

Operating margins in Macao declined.

The story is that LVS is going through major renovations at the Cotai arena and the Londoner casino and once construction is complete LVS will have better properties than everyone else at the same time the Chinese consumer recovers in 2025. So now is a perfect time to do the renovations.

But it means 2024 is a time of uncertainty.

Is LVS losing share because of the casino and Cotai arena renovations or is that a smokescreen for the fact the LVS product is overpriced relative to the competition?

While investors did not take the Q2 results positively management sees things differently. They think they are putting up great numbers in the midst of major renovations and a weak Chinese consumer. It’s a good sign for the future.

When you look at our performance, page 14 of the slide deck, you can see what happened in the quarter. The Venetian Macao did $262 million of EBITDA in the quarter at a 38.2% margin. And it's missing about half its volume of unrated play. So, just with the arena out, which is also a very valuable amenity to drive premium mass performance, look at the strength of the performance of The Venetian. Same thing is true in The Plaza. Look at what the Four Seasons did, 40% margin, $100 million of EBITDA.

So, when we look at The Londoner, we basically took out an equivalent property like Melco or an equivalent property to Wynn Palace. We took that capacity out of the market for ourselves to renovate it. So, for us to put up $550 million in the quarter, in my mind, this is a great result, because we know that we have a limiter in place.

We're missing a significant portion of what is ultimately going to be one of the best properties in Macao, if not the best property. And if you look at the success of The Londoner right now, if you look at the win per unit per day on the table side, The Londoner is the second best in our system. So, in Macao, so when you think about that, the model has been proven and the investment has been validated. Now we're going to open up the better half hopefully by the end of the year in major part, certainly the limiters are going to come off.

So, in my mind, this is a very positive investment for us and we'll get to the margins. We're already doing it in our other properties. It's just a function of renovation, because we're carrying all the costs now associated with the shuttered casino and 1,500 rooms. So, The Londoner impact is really one half of its working, you see the performance, you see the slot win, you see the slot performance win per unit, you see the table win performance, you look at the hotel performance and the non-gaming amenity performance. And then you look at the side that's shut and you realize that's the better side, but we're carrying all the cost. The potential in the future is really there.

We feel very strong about the potential for the margins to reach where we need to go.

And just remember, pre-pandemic, we were at 35% to 36% EBITDA margin on a whole normalized basis business in aggregate. So, we'd like to believe we're in a good spot. We're competing effectively. We have great assets. We're investing for the future.

And when we're done, we're going to have the newest and best products in the market. So we feel very strongly about the path that we're on. It's just going to take a little bit of time to get there. Source: Q2 Earnings Call.

Overall, Q2 earnings were not helpful. Investors are turning skeptical and reducing earnings estimates for 2024 through 2026.

YWR is sticking with LVS, but we will have to be patient. This could take until Q4 2024 or 2025 to regain momentum. The risk is the shares are not trading at a low P/E in the meantime.

Below is a link to the update YWR Earnings models for:

Tencent

Alibaba

Baidu

Las Vegas Sands