YWR: Global Factor Model

It’s happening…

We’ve been talking about it for over a year, and were early…

…but now the Factor Model sees it too.

It’s China.

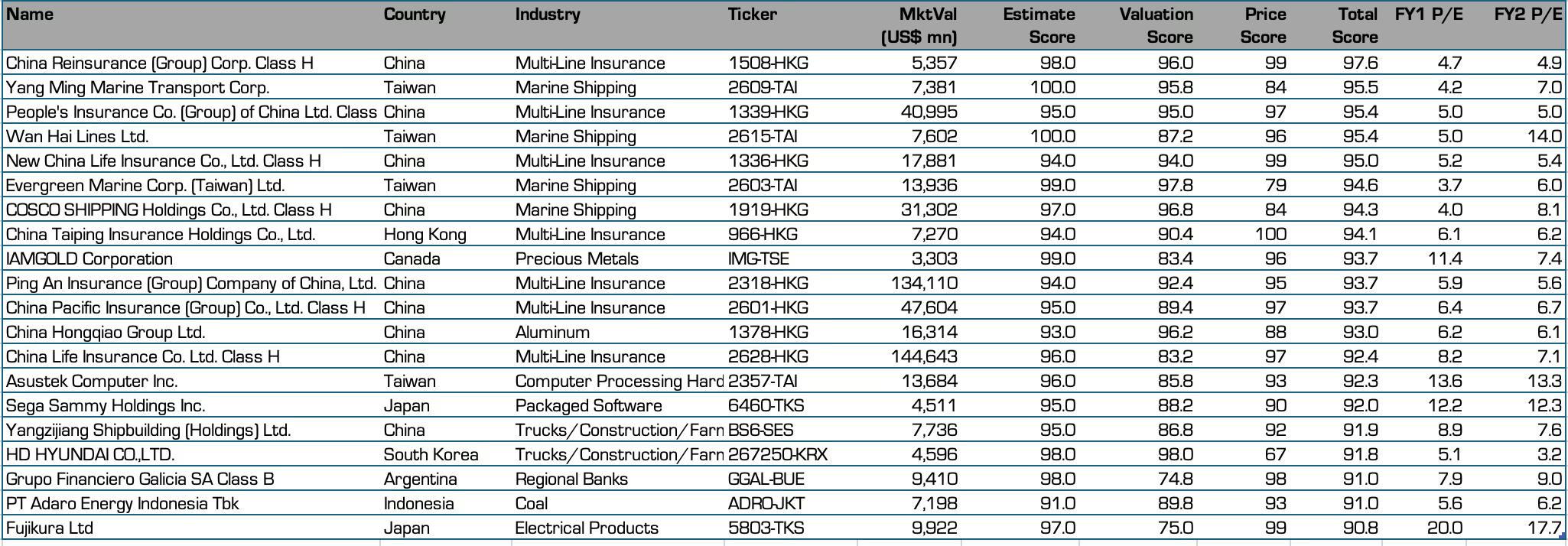

The YWR Factor Model is flooded with China stocks. 10 of the top 20 are Chinese and it continues from there. China is the best scoring country in the world.

YWR Global Top 20

What do you see? Shipping and Insurance. We covered shipping in September’s factor model update.

What’s new is Chinese insurance. 7 of the top 20 are Chinese insurance companies.

What the heck is going on?

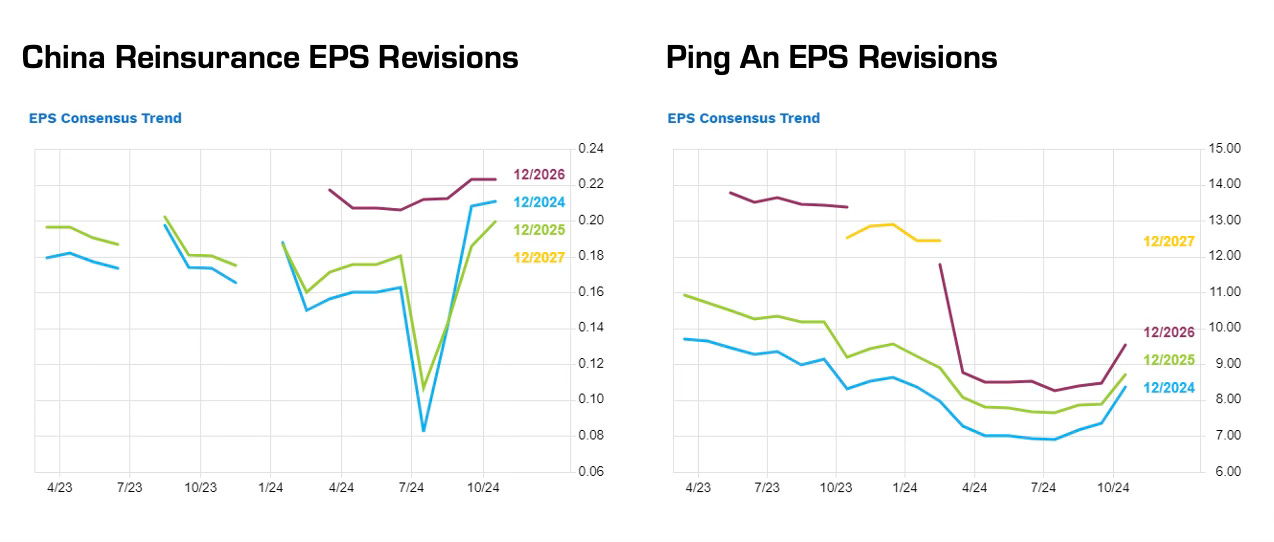

Underwriting is solid and premiums are growing, but when you go into the results the delta is exceptional investment returns from the equities in their investment portfolios. Chinese insurance companies are benefitting from the rising markets.

Our play on this same theme is HKEX (our China FOMO play).

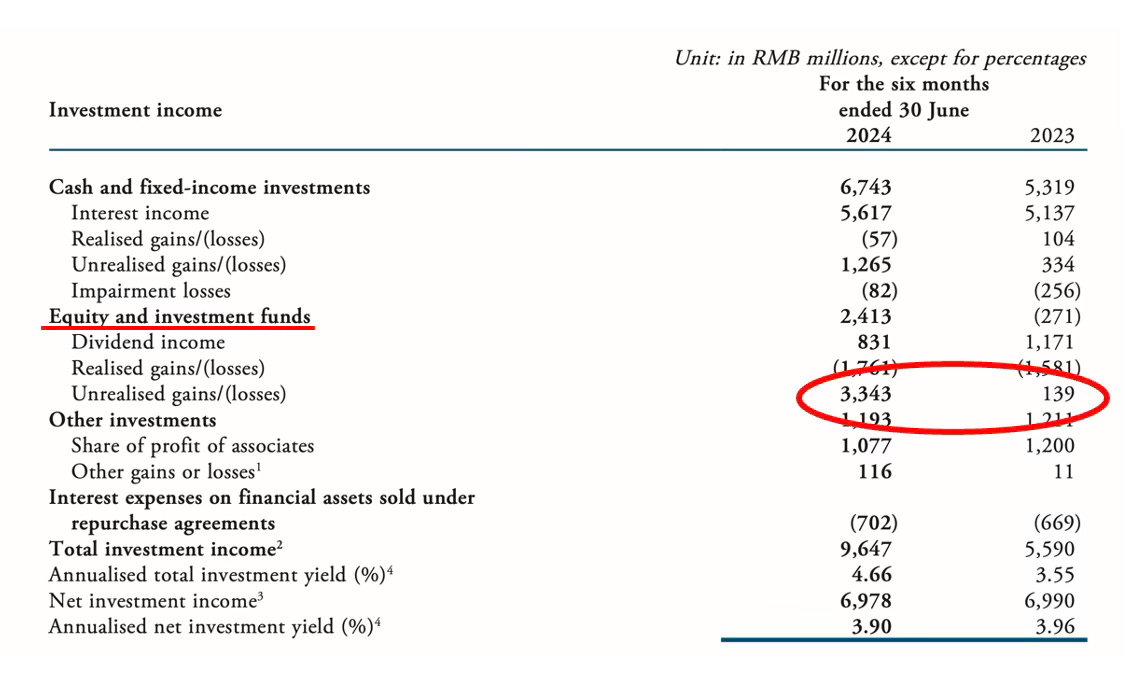

China Reinsurance 1H Investment income. Notice the equity gains.

Ping An Q3 2024 Earnings. Notice the surge in investment income.

I have to say, it’s amazing that Ping An is trading on a P/E of 5.5x…. this used to be a China darling.

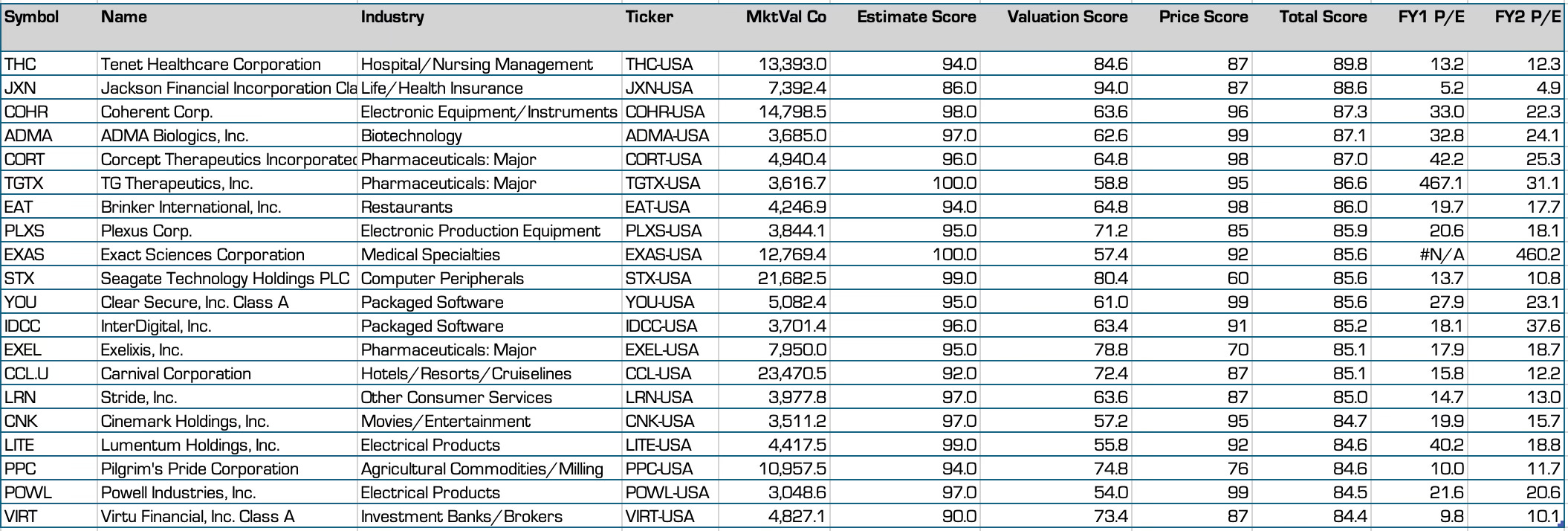

US Listed Top 20

Many of you just care about the US, so here is the US top 20.

You can filter the full database at the end of the post if you want to see more US names.

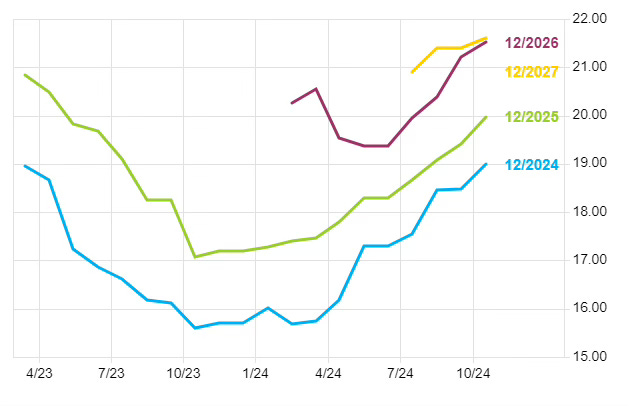

Tenet Healthcare

Tenet has come up before and we highlighted it back in June. It’s an interesting private hospital roll-up play.

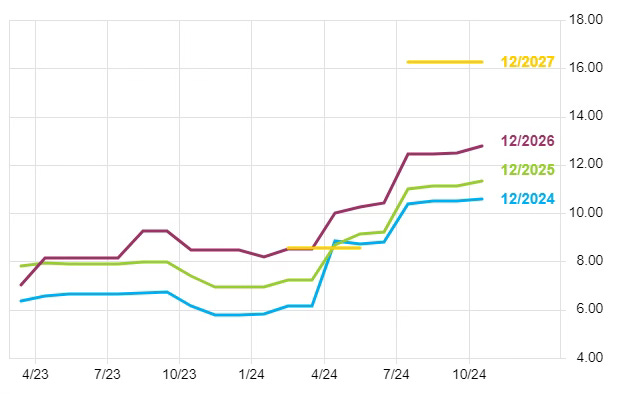

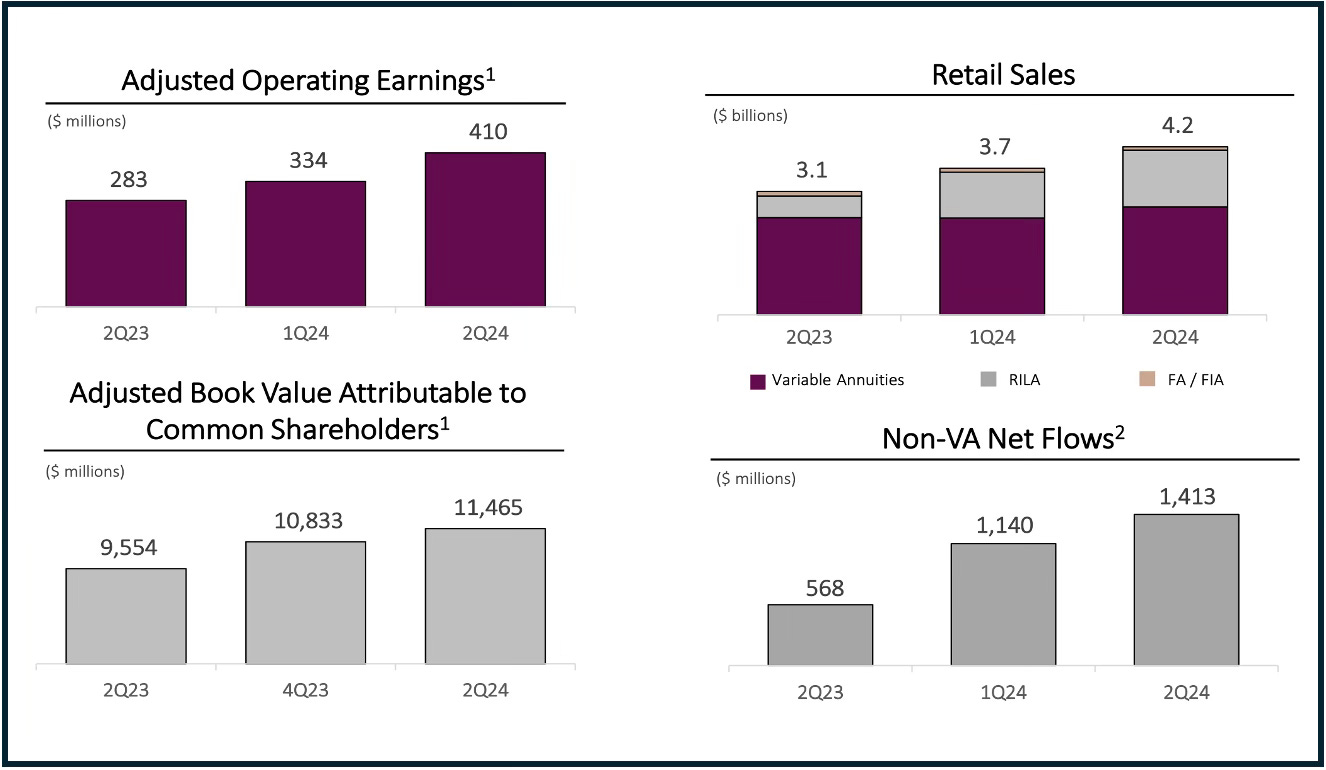

Jackson Financial (JXN)

We bought Jackson for the Dirty Dividend portfolio back in April 2023 (A Friday Money Maker) and it’s done well. Jackson continues to benefit from:

Higher US equity markets (its variable annuity business is basically an equity fund management business),

Growing sales of registered index linked annuities (RILA’s). RILA’s are the insurance industry’s version of structured products and are quite popular (RILA sales +163% yoy). Like with structured products I suspect they is a lot of profitability buried in this “equity upside with limited downside” insurance product.

EPS also benefits from a falling share count while the business grows.

Jackson is trading at 5x earnings and a top position in the Dirty Dividends Portfolio.

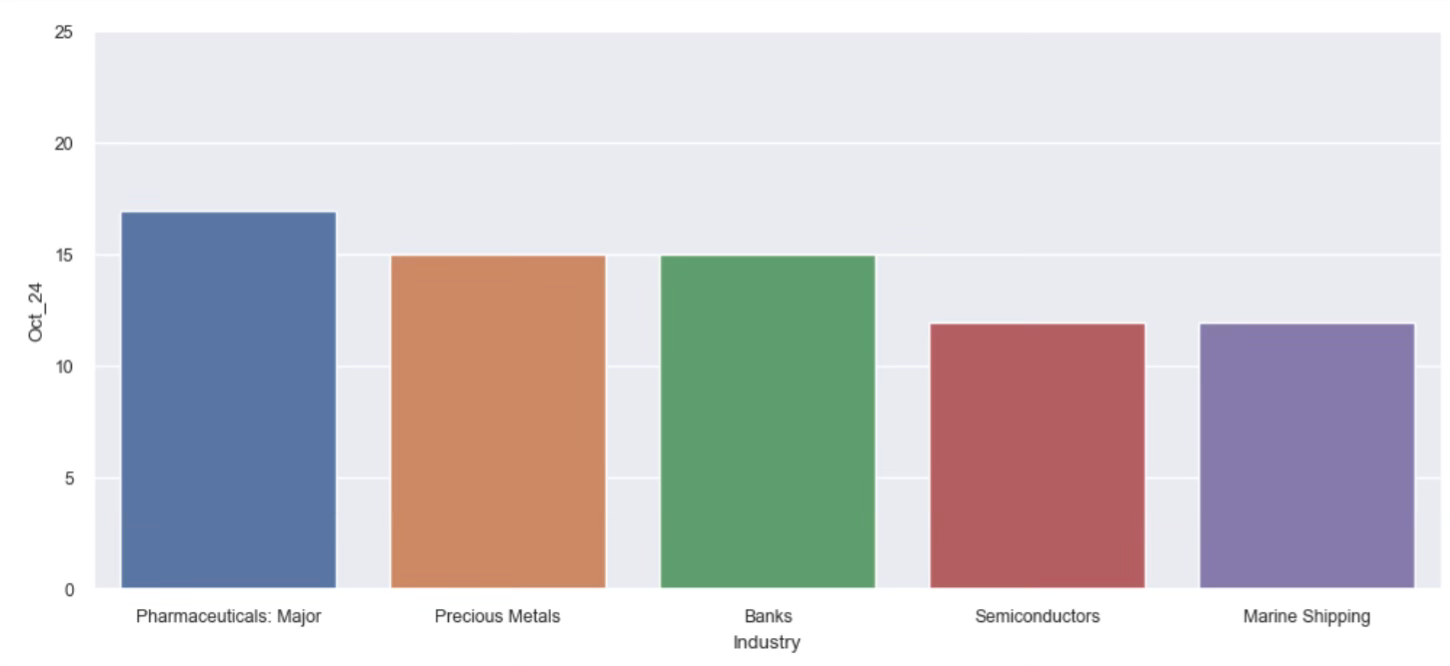

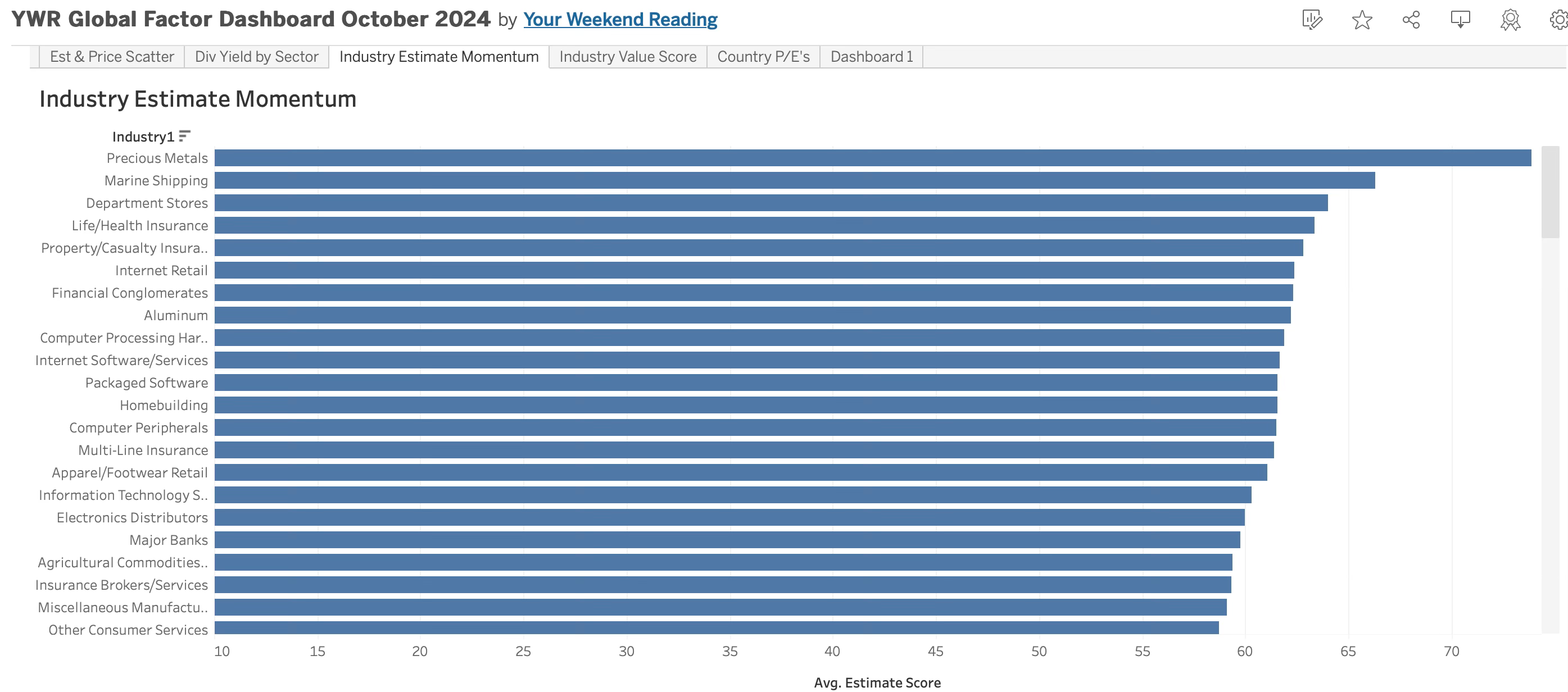

Industry Trends

The industry level upset is that banks have dropped to 3rd place behind Pharma and precious metals. You’ll have to go through the data sheet to see what is going on in Pharma, because it’s not the names you would expect (Orion Oyj? Exelixis?)

When it comes to pure estimate momentum (not including valuation) precious metals and shipping have the highest earnings revisions. Insurance is also notable and another sector where nobody is paying attention.

With the YWR Tableau dashboard (link at the bottom of the post) you can click into each industry group and see which stocks are driving the estimate momentum.

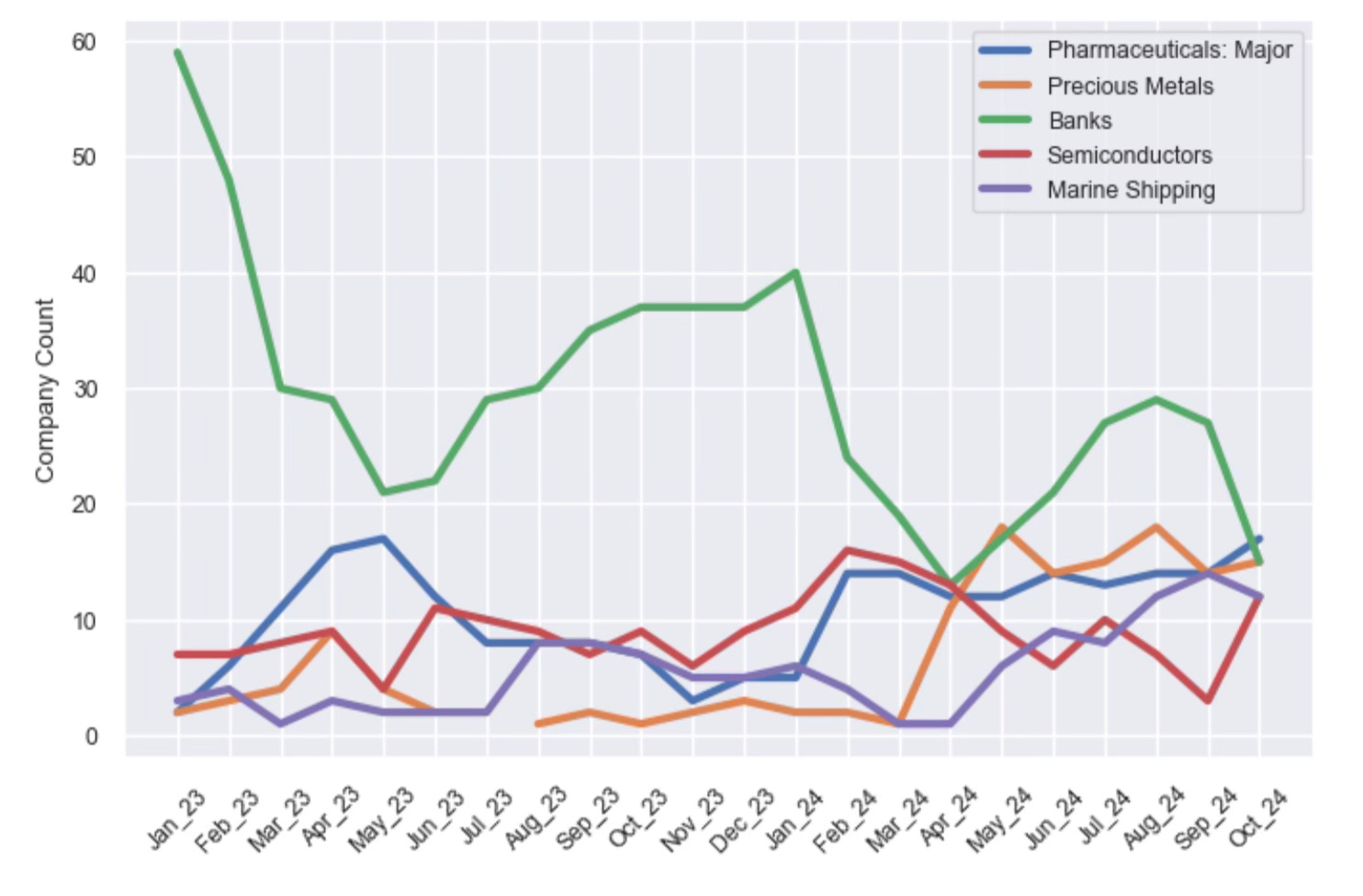

In the monthly trends chart below we see the steady loss of estimate revision momentum in the banks. Analysts have finally caught up to the idea that net interest margins will be higher and loan losses will be low (it’s not the GFC again).

Which means the new, new is precious metals and marine shipping.

The momentum in semiconductors is not coming from the names you are thinking. Yes, there’s Taiwan Semi and Micron but the rest are Chinese names. Again, check the data file below.

And we have to figure out why Pharma is scoring so well.

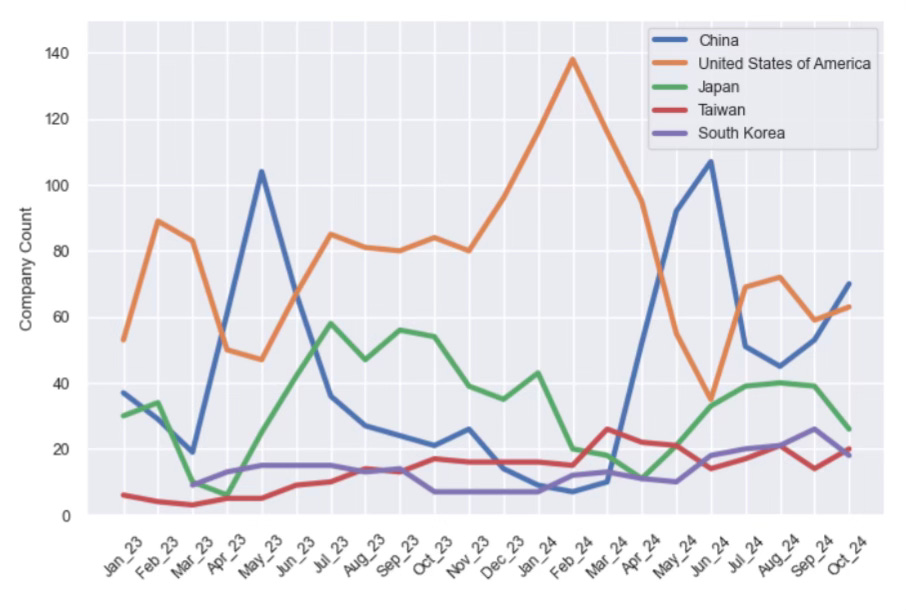

Country Trends

When we look at the top 300 stocks globally, China has the highest representation. China was previously scoring well on valuation, but now also scores well on earnings revisions (shipping, insurance and semis) and price momentum.

In the monthly trend chart (below) you see how the leadership has been flip flopping between China and US.

Taiwan, Japan and South Korea have consistently been in the top 5. We call China, South Korea, Japan and Taiwan the New Europe.

Just below the top 5 Canada scores well because of all TSX listed gold miners.

Below are links to:

YWR Global Factor Model database for October

YWR Tableau Dashboard