Investors lack imagination.

Investors underestimate the strength and duration of trends.

Words of wisdom from John Burbank.

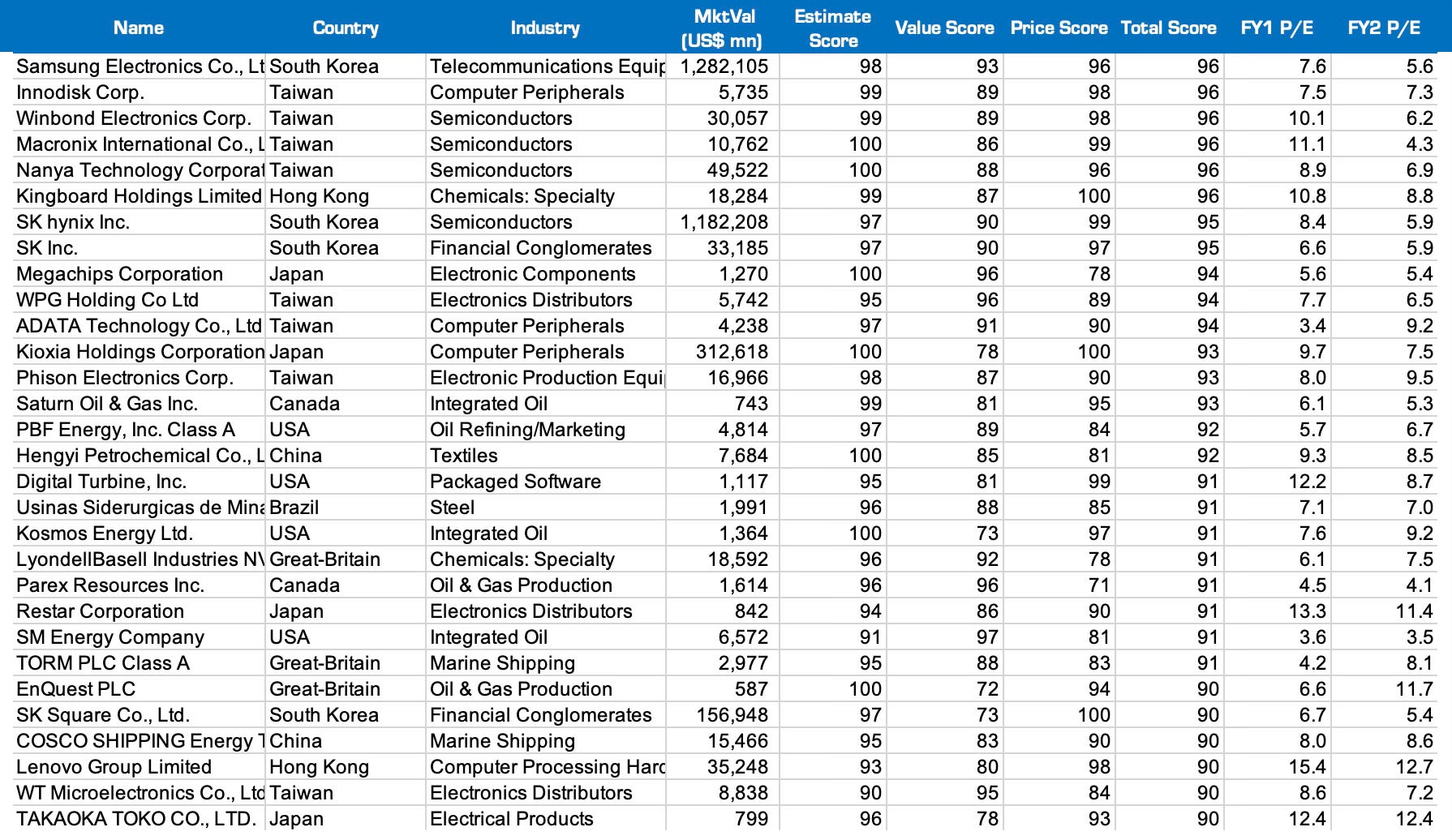

Below are the 30 best ranked stocks in the world.

We have some hard calls to make, but let’s start with the data.

As a reminder we are ranking stocks based on the % change to FY1 and FY2 earnings estimates for over 10,000 global stocks to create our estimate score. We then value companies relative to their sector (banks vs banks, tech vs tech) to create our Value score. Finally, we rank the % move in the share price creates our Price Score.

The best ranked stocks have high % changes to forward earnings estimates, have positive price momentum and relatively attractive valuations.

A link to the YWR Data Apps and the full rankings sheet is at the bottom of the post.

YWR Global Top 30

The global top 30 is full of memory, semiconductor and computer peripheral stocks from Taiwan, Japan and South Korea. The estimate data for the semiconductor and memory supply chain is off the charts. I’ve never seen a vertical move like this. Most trends evolve over years. This went vertical in the last 8 months.

What to do with memory and electronic component stocks?

First off, the ranking system is not a recommendation to buy stocks. It’s our global perspective tool so we know where estimates are changing in the world. So we know the big debates.

Now let me talk out of both sides of my mouth.

Buy case: Yes, the Taiwanese electronic component stocks have gone up a lot, but for all the euphoria they are still trading on <9x earnings. Where’s the bubble? This isn’t CSCO on 50x or JDSU on 100x. But then you say they should trade on 7x because there are no moats and these are commodity component suppliers… Are they though? Are they commodity suppliers, or are these component companies part of a multi-billion datacenter supply chain carefully curated over two decades by Nvidia where it takes years to delivery reliably and get into the club. And these established players are not about to be suddenly overrun by a new Chinese DRAM start-up, especially when AI supply chains are a matter of national defence.

And are we vastly underestimating where the multi-year demand from AI and soon robots? Is Earth turning into Cybertron and the demand for memory, semiconductors and electronic components will go on for years? Basically, AI and robots are a new alien species, which are just getting started, and the build out of the Transformer economy will change the world?

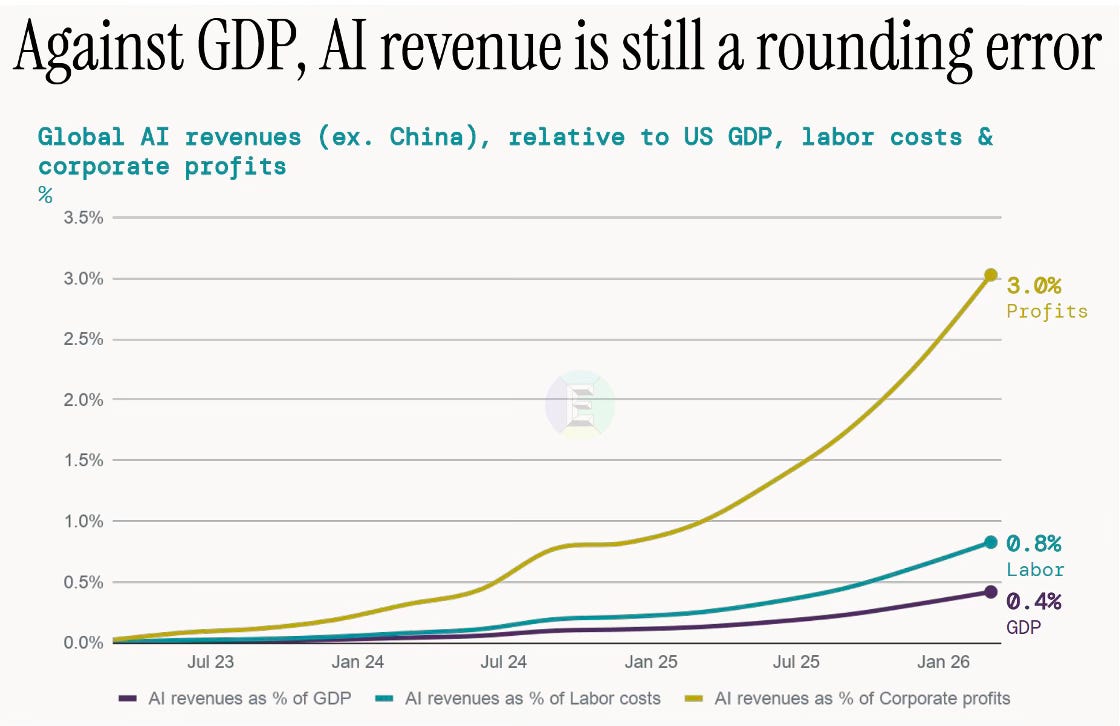

Another way of reframing how early we might be in AI. It’s the biggest technology ever and it’s only 0.4% of GDP. Like with Cybertron maybe instead of constantly calling it a bubble we are underestimating the scale of this.

BTW, I remember in 2004 when we kept calling China a bubble when it would grow 8% every year. We thought there was no way that could keep happening and kept expecting iron ore stocks to crash. And there were lots of super smart bear cases on China back then (still are).

But imagine if we could have gone back in time to our 2004 selves on the trading desk and said “Hi. sorry to interrupt your bubble conversation…. but I’m from the future…. and China is going to do this every year for the next 20 years..”

Imagine the perspective of knowing that even if everyone would have said you were crazy.

And another thing. Even if the 2nd derivative on datacenter spend goes to 0 (no growth) or slightly negative (a temporary pull back in new datacenter spend) do the stocks still go up because the valuations are effectively saying investors don’t believe the earnings estimates anyways, and when the actual profits come in the stocks start rerate to 10-14x earnings?

This is was a lesson from the European banks. The second derivative of earnings upgrades from the interest rate moves ended in 2024, but we held on because they were still too cheap. Since then the stocks have steadily rerated higher as the reality of the higher profitability played out, even though the estimates were barely changing.

Maybe in 2027 Samsung rerates to 11x earnings, or KRW 600,000/share, which isn’t extraordinary, but still another +70%. And Korean retail is right to get on board and buy it.

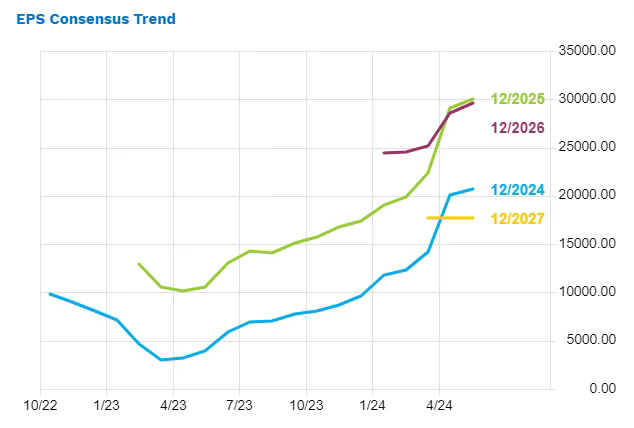

The bear case: Below is the forward consensus for SK Hynix in May 2024 when it first started showing up in the global factor model.

Go back in time and revisit the set-up. SK Hynix was announcing that 2025 would be great. That they were sold out of HBM chips.

Earnings estimate for 2025 were rising and despite SK Hynix saying HBM supply was sold out and going to grow 60%/year analysts still hated memory stocks, so they said it was a bubble. Their EPS estimate for 2025 was KRW 30,000 but the estimate for 2027 was below 20,000; ie profitability all comes falling down again after a 2 year burst.

That was the perfect set up.

Rising profitability, but analysts fading it.

Contrast that with the SK Hynix estimates today in the YWR Factor Model Data App (link at the bottom). KRW 180,000 for 2026, KRW 359,000 for 2027 and KRW 630,000 for 2028. The analysts are now onboard the bull market and predicting a 250% growth over the next 2 years.

Yes, SK Hynix is still cheap, if the numbers are right, but it’s a lot harder trade now. It’s a $1 trillion stock, the analysts are all bullish now, Korean retail is levered long and the company is selling $29bn in stock.

Yes, it will probably still work (and I still own most of my position) but it’s not fresh meat.

Instead, what’s a set-up now that looks like SK Hynix in 2024? Something where the company is making lots of money, the trend has changed and yet the analysts are fading it? Saying it’s a ‘1-off’.

Hmm… let me use the YWR Factor Model Data app to find one…

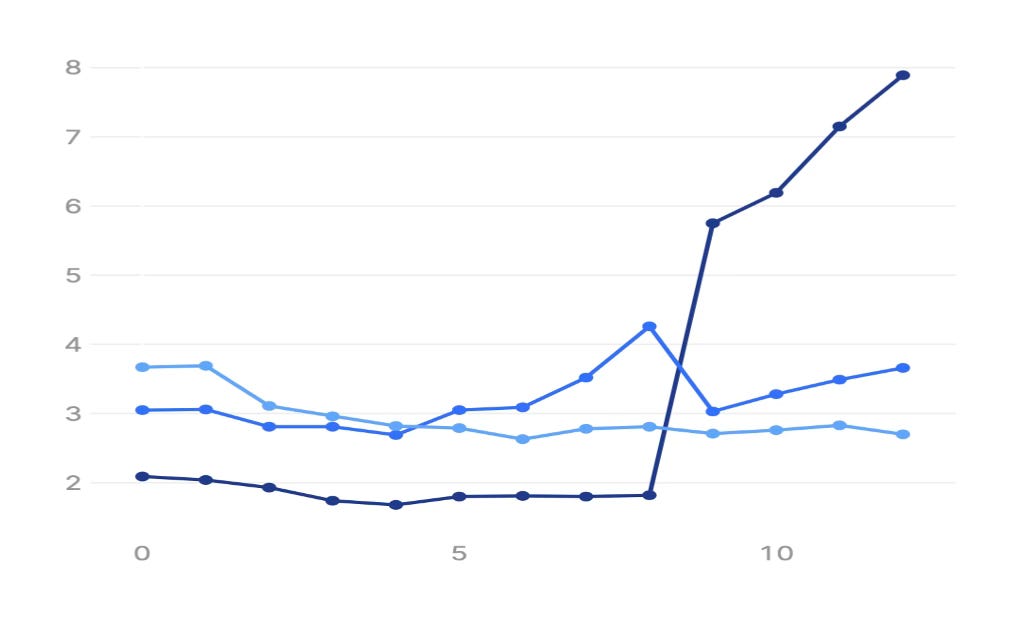

How about this?

Here’s a stock making record profits trading on 5x because the analyst say the earnings are unsustainable. The 2026 estimate is $7/share (and rising) but the 2027 EPS is back to $3.60 and then even lower in 2028.

Which stock is it?

Frontline. Tankers.

Massive disruptions from the Iran War which are stretching out tanker supply and forcing up rates. But the market thinks it is a one off.

All of energy is like this. Look at the earnings estimates for TotalEnergies and Shell. Strong 2026 but then 2027 is lower. Same thing for chemical stocks like Dow or Lyondell. Everything benefitting from the Iran War disruption has this pattern. Great profits in 2026, then it all goes lower in 2027.

US refiners are also benefitting.

But the market and the analysts are fading it.

So you want a SK Hynix 2024 set-up?

It’s in the energy space. The trade is that the Iran War disruptions are the start of a multi-year problem and it is going to take the world years, maybe even decades to re-architect global energy supply away from the Middle East (3 Trillion non-AI trends). And we’ve only seen Ch.1 of the energy price shock.

BTW, my favourite outcome would be that Iran becomes a new Dubai and the Middle East booms (economically) with the whole region synched up and growing. And I thought maybe with a combination of carrots and sticks that was possible. But, I’m slowly slipping into the view that Iran is a world changing intractable problem that is not priced in.

Back to the data.

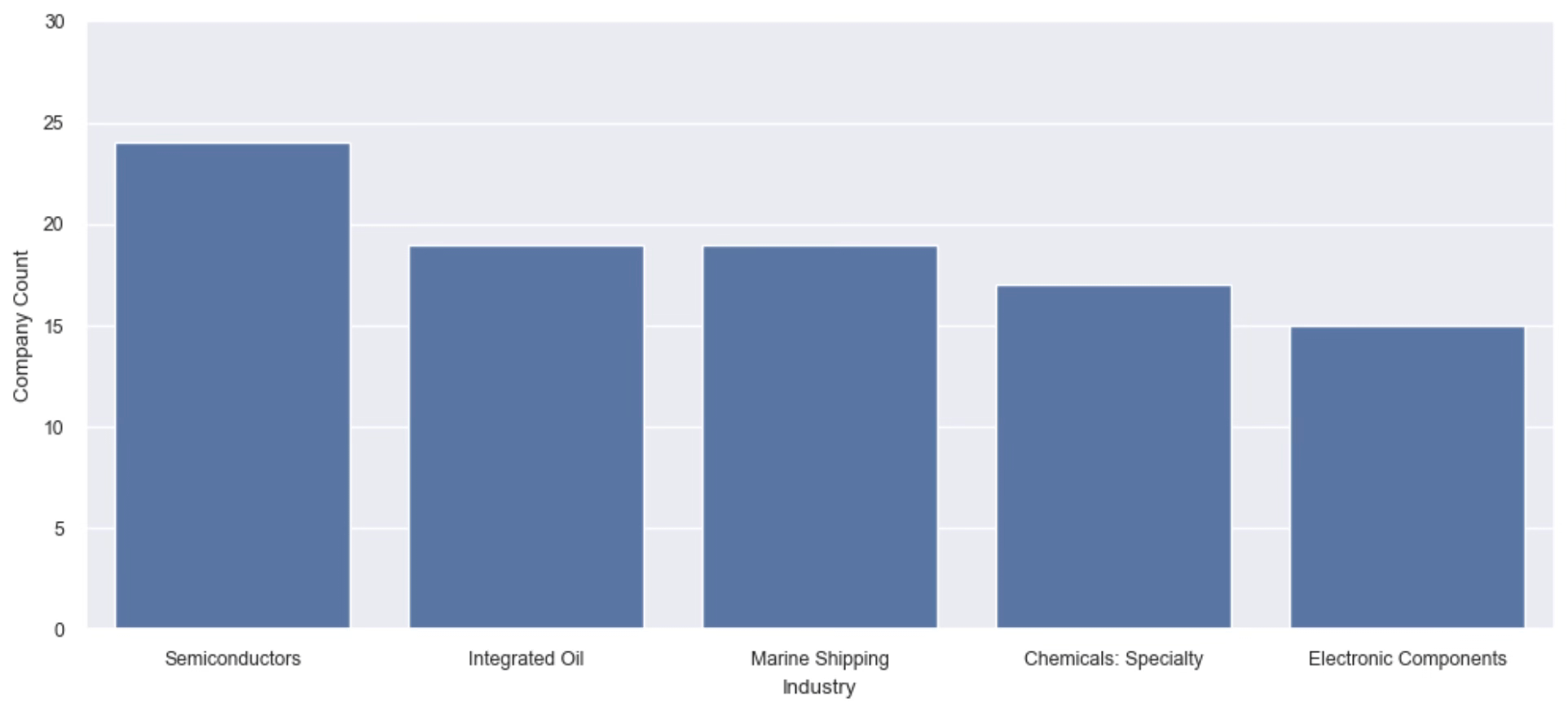

Top Ranked Sectors

The top 5 ranked sectors are semiconductors (#1) and electronic components (#5) which is the Cybertron theme. Computer peripherals is another top ranked Cybertron sector, but didn’t make the top 5.

But then Intregated Oil (#2), Shipping (#3) and Chemicals (#4) are the ‘US as the new Middle East’ theme.

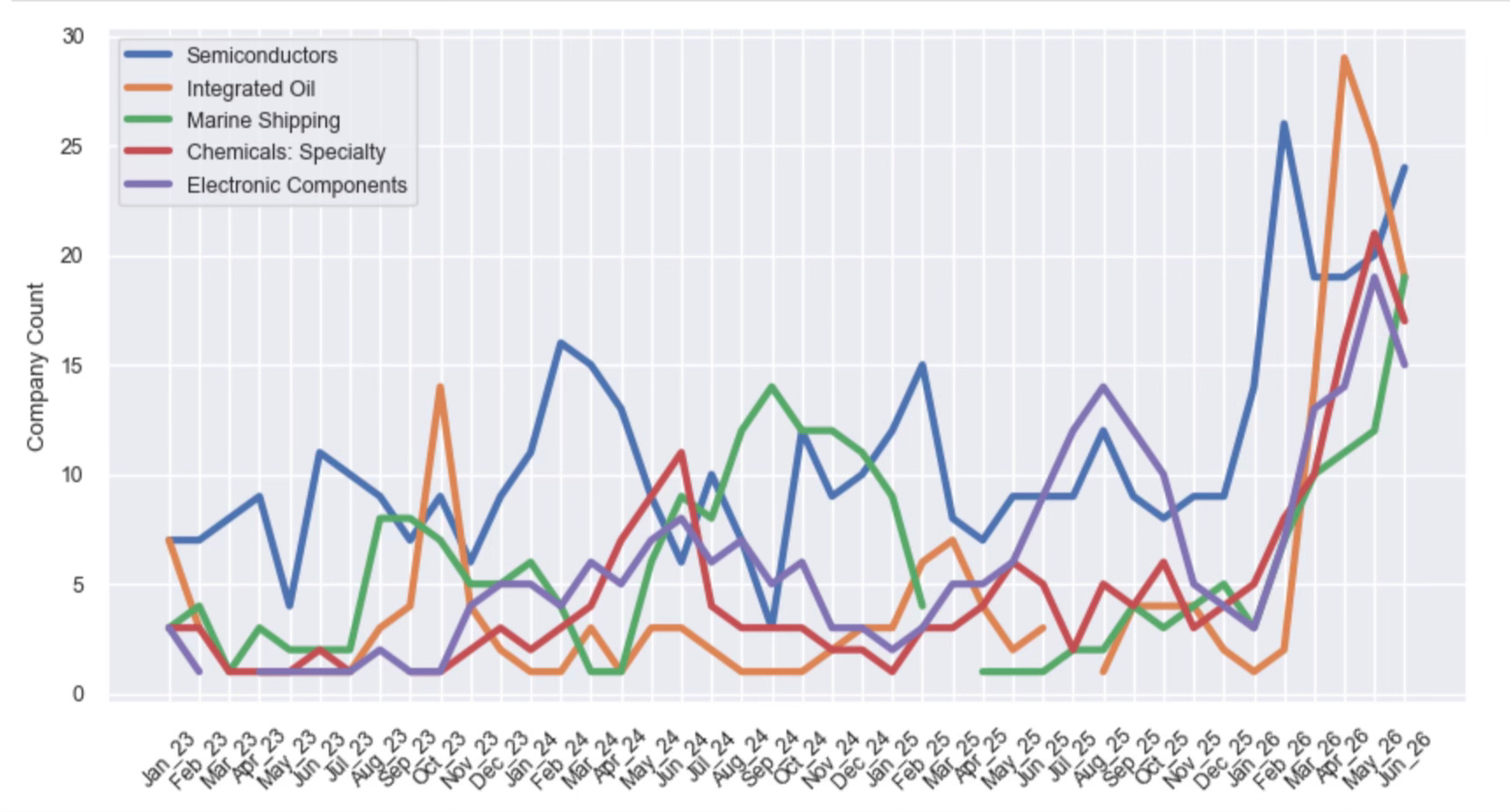

In the monthly progression chart below you can see (strangely) how all five themes started firing together at the beginning of this year. A previous multi-year theme which has completely dropped out is Major Banks.

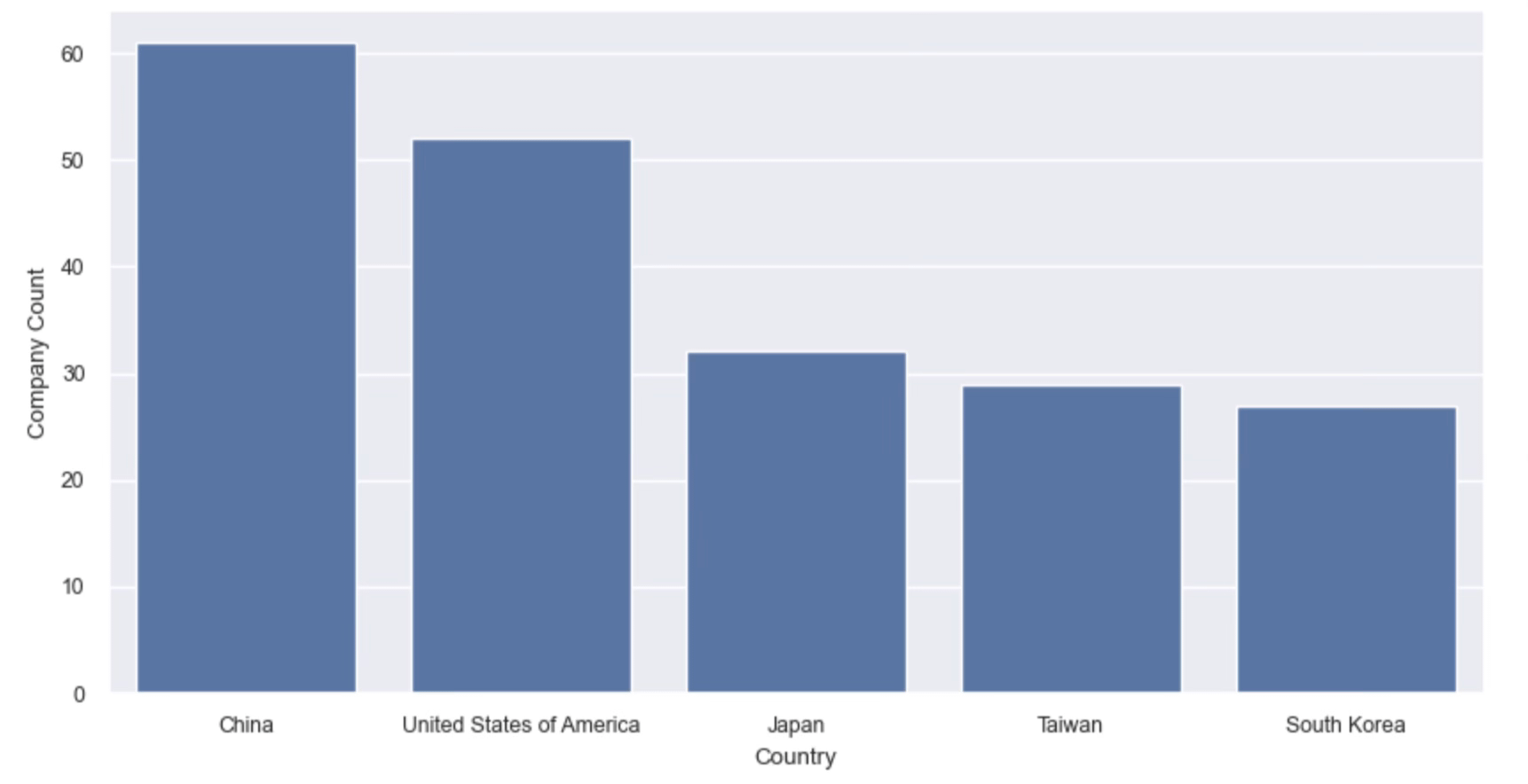

Top Ranked Countries

It’s strange to see China ranked so highly, when the FXI is -17% ytd (and driving me crazy), but when you look into the individual stock rankings in the YWR Rankings Sheet (link at the bottom) you see China has many stocks in electronic components, computer peripherals, semiconductors, shipping and chemicals; all the top industries. Unfortunately, a lot of them are A-shares (which is performing better).

The US is always in the top 5.

Then the last 3 countries are almost always there too. Japan, Taiwan and Korea. Like China they are exposed to all the top industrial themes.

Below are links to the rankings sheet with rankings for over 10,000 stocks as well as the Data App I use to show the estimate revision charts, which is highly useful.

I also include the global inflection ranking sheets to show where earnings have recently inflected. A lot of it is energy related. Contract drilling, oil and gas, oilfield services, coal.

Trucking companies and staffing companies are also inflecting upwards for some reason.

Be original, be imaginative, dig into the data, find the new themes and let me know anything interesting.

Erik