YWR: 3 (Non-AI) Trillion $ Trends.

“How many years do I have left in the memory bubble?”

“Should I shift my exposure more to inference?”

“Am I underestimating the demand for Neoclouds?”

“Is it too late to buy optical connectors?”

And on and on….

AI, AI, AI. It’s all anyone talks about.

It’s fine. It’s warranted. AI is a massive trillion $ trend.

But it might be time to consider some other trends.

The AI 2nd Derivative

Think back to May 2024. May ‘24 was when Nvidia blew everyone’s minds with guidance that Q2 revenues were going to grow +52% quarter on quarter ($7.2bn → $11bn).

It was our first big signal that datacenter capex was going to skyrocket.

Unimaginably.

The rest was history.

Hyperscaler Capex grew from $240bn to $416bn in 2025. Then earlier this year, when we thought we had a handle on things and 2026 capex would be $600bn, everyone came out in April and upped the numbers again. Now we are forecasting almost $1 trillion in Capex by 2028.

The problem is it’s hard to see how AI Capex surprises again from here. Or to the same magnitude. Or, to a magnitude which isn’t already priced in.

The big tech companies are already spending all of their operating profits on capex and beyond. Google did an equity raise, to fund AI, which is kind of unimaginable. Google needing to raise money? And the rumour is Meta might raise money too. And Michael Burry is pointing out all off balance sheet SPV’s and lease agreements also being used to fund datacenters.

I’m not saying this is all going to crash. I’m saying many of the financing levers have been pulled (operating cash flows, off balance sheet financing, capital raises) and the big tech companies are hitting spending constraints.

There are also practical constraints. Even if companies wanted to spend $1.5 trillion on datacenters it’s increasingly hard to find communities to host these data centres or utilities able to power them. It’s going to be hard to spend the money.

We are hitting the near term financial and physical limits on AI spend.

Maybe I’m wrong, but it feels like a lot of the big AI capex surprise has happened.

So why not find on some new trillion $ trends?

Trillion $ trends nobody is positioned for.

Non-AI Trillion $ trend #1: Re-architecting global energy supply

What if Iran is unfixable? I know there is a deal in the works, but will any deal really last? It reminds me of that old Montana saying.

You can’t straighten a crooked stick.

What if we have an angry troll controlling the Straight of Hormuz who can’t be dislodged? Removing the IRGC requires a full scale occupation of Iran, which nobody wants to attempt. Unless, maybe the IRGC collapses of its own accord. Or, maybe like North Korea it just goes on for decades.

It increasingly looks like the future is a prolonged state of conflict and insecurity in the Persian Gulf.

Maybe traffic through the SOH improves, but never returns to 15 million bpd of oil or 112 bpm of natural gas (20% of global LNG). But it’s not just oil and natural gas. 30% of global urea, 20% of ammonia, and 8% of aluminium flow through the SOM. The Middle East built up a massive petrochemical and refining complex to get more value out of their raw commodities.

It’s hard to imagine a world without the Middle East at the heart of energy supply, but maybe we need to start.

Start with pipelines to Turkey and Israel. Does Saipem get billions of dollars of orders to build alternative routes? Does Turkey become a new refining and energy hub?

And Dangote Refinery in Nigeria. Does Nigeria become an important petrochemical hub. Safely tucked away in the Gulf of Guinea.

The problem with Isreal, Turkey and Nigeria though is they are not on the road to India and Asia. How do you fuel Asia if not from the Middle East? The only answer I can think of is more Russia. Does this force some kind of a peace deal with Russia?

An obvious beneficiary is everything in the Gulf of America. The Gulf of America is the world’s new gas station. In Qatar Changes Everything we highlighted the LNG Terminal plays (LNG, VG, NEXT). But the refiners and chemical plants also benefit.

In our YWR estimate monitoring tools these are all the sectors with the highest momentum in the world. Refining, oil and gas, chemicals, coal, aluminium. Everything that comes out of the Middle East.

And what about floating LNG plays like Golar. If we are trying to replace Qatar is the cheaper, faster option to set up floating LNG in Africa? And what are the beneficiaries of floating LNG construction? Do all your semiconductor bottleneck analysis on the shipbuilding industry.

Oil and gas, and chemicals are the obvious plays.

But there will be many creative 2nd derivatives. What happens with airlines? Do the Middle East carriers benefit because they can access stranded jet fuel at low prices, or do traveler’s not want to route through the Middle East? Does Turkish Airways benefit?

Turkey is one to consider because it comes up a lot when you start thinking how energy and trade flows might change and who will benefit.

Do renewable stocks benefit? Do Chinese solar stocks start to work?

I don’t have all the answers. I just want to get us thinking about the size of this trend. Because it’s world changing and the big the big funds haven’t even begun to play it.

Non-AI Trillion $ trend #2: Developed Market Banks

Following on from Non-AI trillion $ trend #1 we are eventually going to have high energy prices.

Inflation and interest rates have been notoriously hard to predict, but all the signs are there that the combination of high levels of government spending, AI capex, industrial reshoring, tariffs and now an energy supply shock is going to lead to higher inflation. We already had a 4% CPI print.

It seems likely that with 4%+ inflation US 10 years could be at 6% soon, and the Fed will be raising rates at least 75bps. The ECB just raise rates and the Bank of Japan is preparing to raise rates too.

And who benefits from higher interest rates?

The banks. Yes, the are pluses and minuses, and the timing of how it all plays out depends on how each bank is positioned, but broad brush, higher interest rates are good for banks. It’s a lot easier to make a 2% spread with 10 years at 6% than it is when they are 4%. And possibly we are going to yet again underestimate the change in interest rates and how much banks will make. Like we did post-COVID.

Banks are another sector the big funds don’t want to own, and yet DM Banks have been one of the best performing trends in the world. The best performing trend nobody talks about.

Banks are making more money from higher interest rates, but the second effect is their risk appetite has improved. Banks are lending again. We see it in the Federal Reserve H.8 statements and it is coming through in the results.

Take Mitsubishi UFG. Do you want to know who is quietly sucking up datacenter debt? It’s the big monster banks in Tokyo. In The Godzilla Trade we wanted to know where the Japanese banks would point their liquidity firehose. Turns out data centers are one of the sectors.

· Leading global financial

across both public and private markets, etc.

services

Equity ratio

. Product supply

Learn MS's advanced expertise

16%*2

approx.

capabilities

AI, cybersecurity, etc. (including secondment)

24%

Collaboration Areas: Further Deepening and Expanding

US

Asia

· MS equity compensation platform

Established 2 domestic PO

Financing for

Collaboration on

investment trusts*4 (FY25)

WM

AI-related infrastructure

convertible bonds in

MUTB

Number of Participants

AM

Taiwan

approx.35,000

MUFG

MS

Global IB

USD 8.5Bn

Total approx. USD 4Bn

. Improved price competitiveness by

introducing MS SOR*3 in MUeSS

AuM of Japan equity fund for

overseas market: YoY x2

Mar 26

New collaboration via

Global Markets

Joint Marketing

. FX trading: Doubled volume of

· Sharing MS's U.S .- leading expertise

transactions with institutional investors

in AI and cybersecurity etc.

expertise

Exchange

Product

Customer

for 2 consecutive years

· 24 round-table discussion by MS

structuring

CoreWeave

capabilities

base

. Japan Equity Research Ranking*5

management - including WM

MS

MUFG

No.3

for 2 consecutive years

3

3

branches in Tokyo, Osaka &

Nagoya*6

*1 Based on net revenues in 2025. ISG: Institutional Securities, IM: Investment Management, WM: Wealth Management *2 Equity in earnings / consolidated

book value (MUFG's holding of MS's net asset and goodwill. Includes preferred shares. ¥4.3tn as of end Mar 26) *3 MS's smart order routing

*4 Morgan Stanley US Equity Insight Strategy Fund/ Emerging Markets Debt Opportunity Fund *5 MSMS Rankings by Extel (2025-2026)

MUFG 17

*6 Rolled out across bank branches (WM) and a wide range of areas including cybersecurity and IT, with TB and Securities also participating")

Morgan Stanley originates the debt and MUFG either owns it or sells it on to Japanese insurers.

MUFG’s slide deck highlighted something else interesting.

MUFG were trying to show how they can rerate to be more like Goldman Sachs and JP Morgan (also shows you they intend to take on a lot more risk to be a global player), but what it highlighted instead was European banks. Barclays and BNP are earning the same ROE as MUFG but trading 40% cheaper.

If you want to bring together global data centre capex funding, plus replacing the Middle East infrastructure funding, plus higher interest rates in a sector that is cheap and nobody owns it’s global banks.

Banks are your second Trillion $ Non-AI trend.

Non-AI Trillion $ trend #3: China

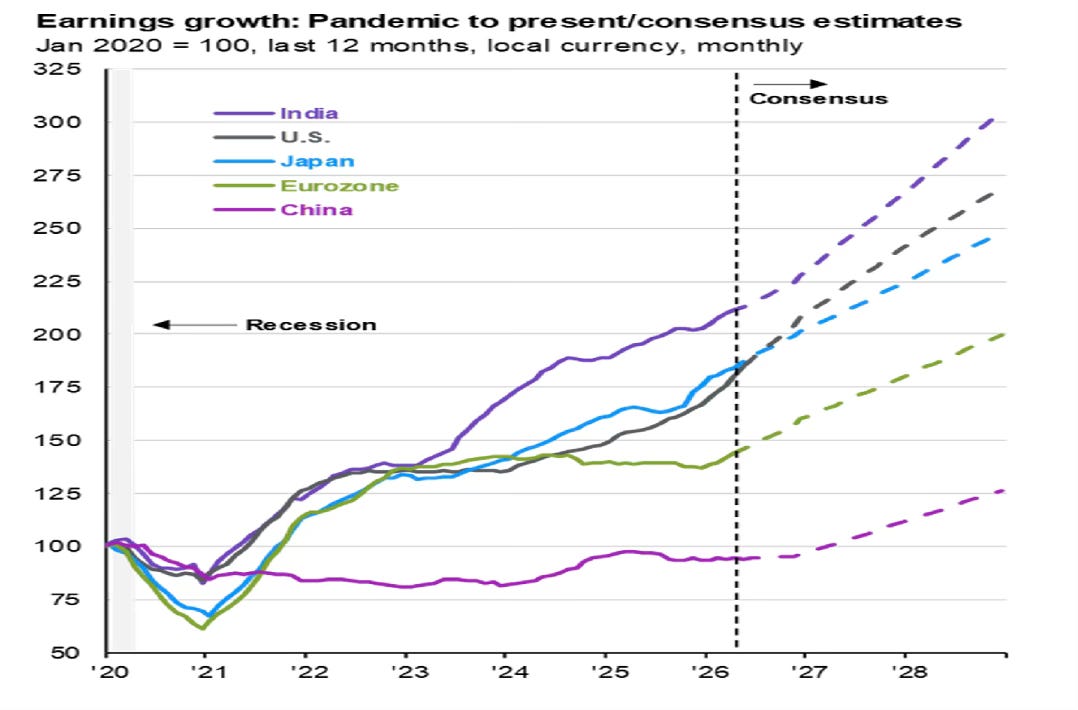

What’s the second biggest market in the world, which nobody owns, which is also the cheapest and is at an earnings inflection point?

The JPM chart below confirms the same inflection point we discovered in Hang Seng on the Launchpad. Chinese earnings are about to inflect upward and start growing again after the multi-year property crash.

I will admit I thought this EPS uptrend was supposed to start sooner, and it kind of did, but what I did not expect was the implosion in Chinese online retail earnings at big earners like Alibaba. Bank sector earnings are already recovering.

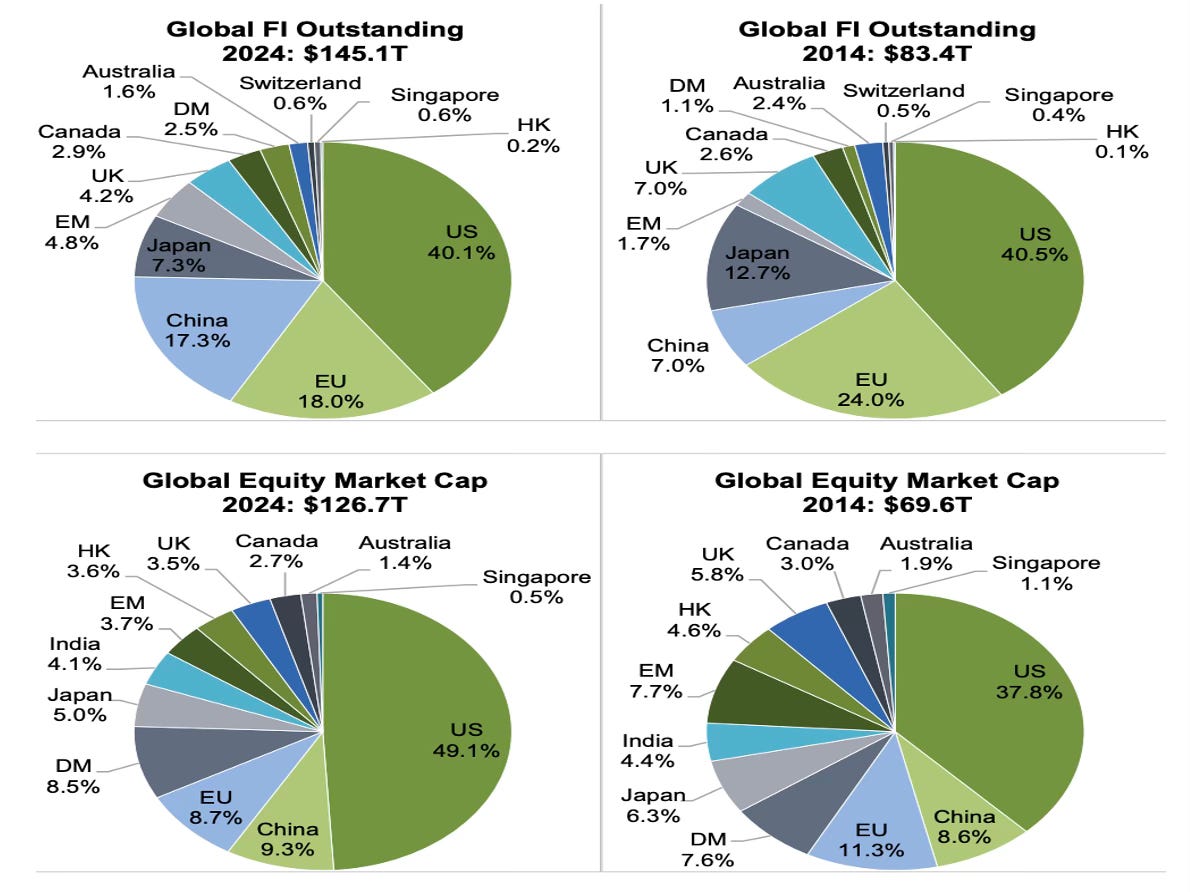

As a side note take in the significance of the chart below. What is the only equity market which has been able to grow its market share over the last 10 years in the face of the US equity juggernaut?

US equities are 49% of global market cap, but China is the second biggest market in the world for both equities and fixed income (almost) and growing. And nobody owns it.

And question. Does China benefit from the rearchitecting of the world energy supply? They are already leaders in renewables. Do their construction companies benefit too?

Does HK originate a lot of this new infrastructure finance in Turkey, Nigeria and the Middle East?

Yes. Chinese equities have been frustrating this year, but I can’t unsee what looks like a big set-up.

Spread your wings.

So there you go.

Three trillion $ non-AI opportunities that your peers are not focused on.

Please share your thoughts.

I feel these three trends are going to intertwine a lot.

Have a good weekend.

Erik

Claude Opus 4.8 disagrees with your numbers. It says:

"The US makes up roughly 60–65% of global stock market capitalization as of early 2026, by far the largest single share. Let me give you the rough breakdown of how the major markets compare.

The US sits around 60–65%. Behind it, the next largest are typically Japan (~5–6%), China (~3–4%, mainland and Hong Kong listings combined), the UK (~3–4%), and then France, India, Canada, Germany, and Switzerland each in the roughly 2–3% range. India's share has been climbing in recent years and now rivals or exceeds the major European markets depending on the index used.

A few things worth flagging given how the numbers get cited. The exact figure depends heavily on the index provider and methodology. The MSCI ACWI (which is free-float adjusted and excludes most frontier markets) tends to put the US near 63–66%. The broader FTSE All-World or total-market measures that include more of China's domestic A-shares pull the US share down somewhat. China is the big methodology swing factor because a large portion of its market is state-owned and not free-float, so float-adjusted indices understate its gross market cap considerably."

That 60-65% is in line with other numbers I have heard over the last year which is why I bothered to ask the AI.

You know my take on China … 🇨🇳

ps: what do you see on Alibaba online retail earnings?

I see modest growth last few quarters but must be missing something

Thanks Erik