YWR: It's Happening...

We’ve been bullish for the last 3 years.

And will be bullish for 3 more (S&P 10,000, Is this the Biggie?)

Why is that?

What keeps us in the trade when everyone is wobbling?

Because we have a view on the credit cycle.

The best part is yet to come.

The Great Banking Winter (2010-2021)

We always talk about Central Banks, but it’s the commercial banking system which creates credit and money in the real economy.

What never got enough attention was the damage 0% interest rates did to the banking system post the GFC. And conversely, what investors are missing now is why higher rates now are such a change. And why banks will want to lend more than ever.

Post GFC commercial banks in Europe, the US and Japan were in the dog house. They were hated. The political zeitgeist was that 2008 could never happen again. Angry regulators reviewed everything about the crisis and spent years coming up with new rules for banks around operational capital and liquidity.

For the banks the rules were always changing and always getting worse. On top of this was the pressure to profits from negative interest rates. As a bank it was hard to make money.

It was a difficult period.

Banks did what they were told.

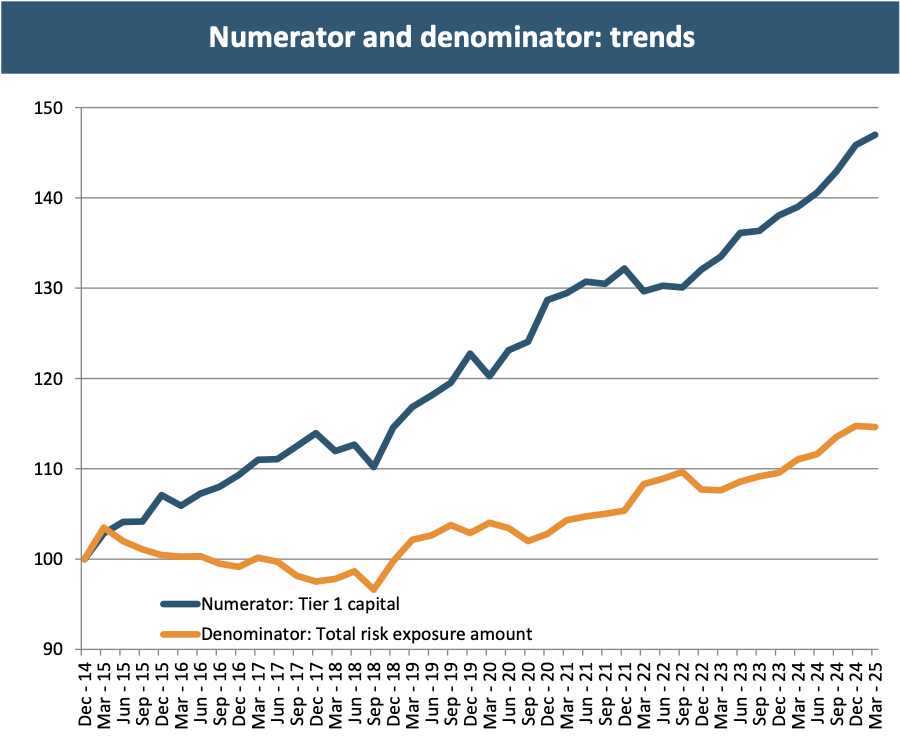

They built up Tier 1 capital and didn’t take risk.

This was the Great Banking Winter of 2010-2021.

Then in 2021 things changed.

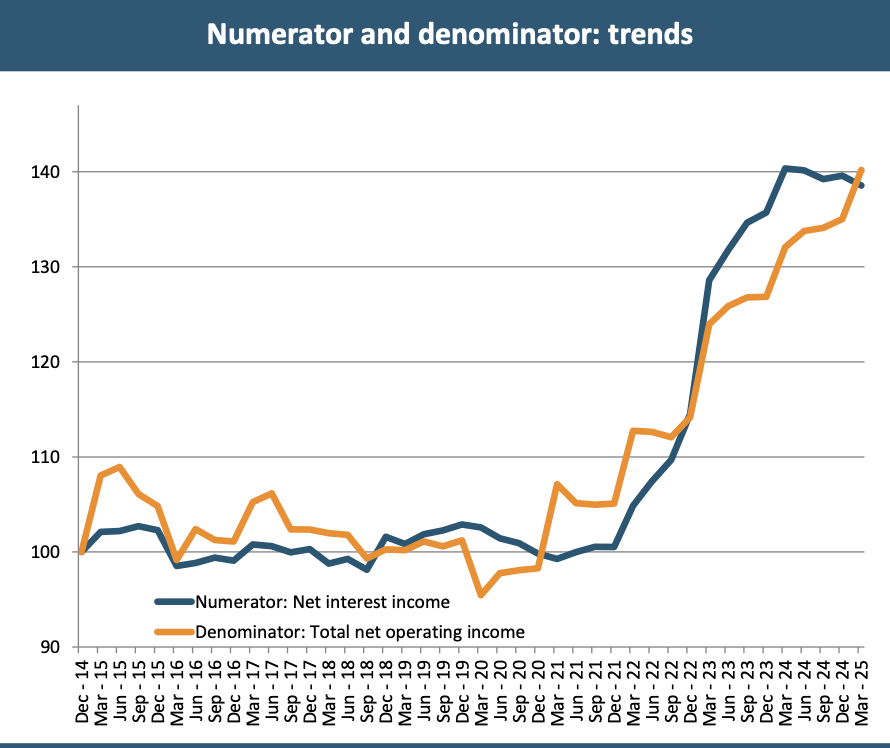

There was a sudden, and sharp increase in interest rates across the world. Bank profits boomed!

This sharp expansion in bank net interest margins inspired us to write How I learned to love European Banks in September 2021.

Our view was a multi-year banks trade was underway.

It got 1 like. Thank you Yonathan Daniel

The trade would have 2 parts.

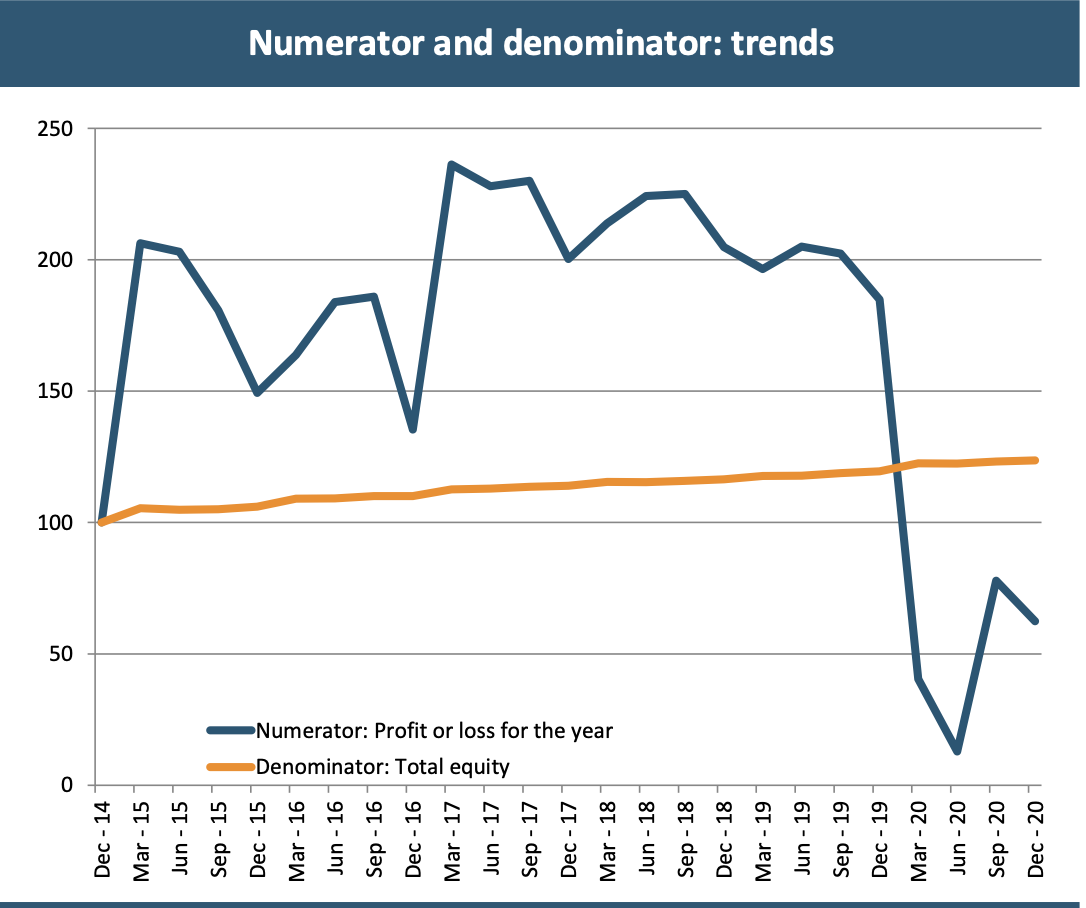

Part 1: Net interest margins and revenues would grow strongly. Contrary to consensus at the time our view was higher interest rates would not lead to NPL’s. Banks had not been lending for 12 years. You don’t get asset quality problems when you haven’t been lending. 2019 banking sector assets were still at 2007 levels.

Investors were massively underestimating the future profitability of European banks.

While banks would make record profits in Part 1, they would still be apprehensive about the macro economy and unsure whether these newfound profits were sustainable. Chicken Little. So in Part 1 banks would return the money to shareholders through dividends and share buybacks.

It’s taken a year longer than expected, but there are signs we are transitioning to Part 2.

Part 2 is when confidence returns, animal spirits kick in and banks start to lend again.

The pendulum finally swings back the other way.

The Lending Boom of 2026-2030