YWR: PE/VC Q2 Activity Update

Sorry for the PE/VC overload this weekend, but it’s time to review the Q2 deals and look for opportunities in the trends.

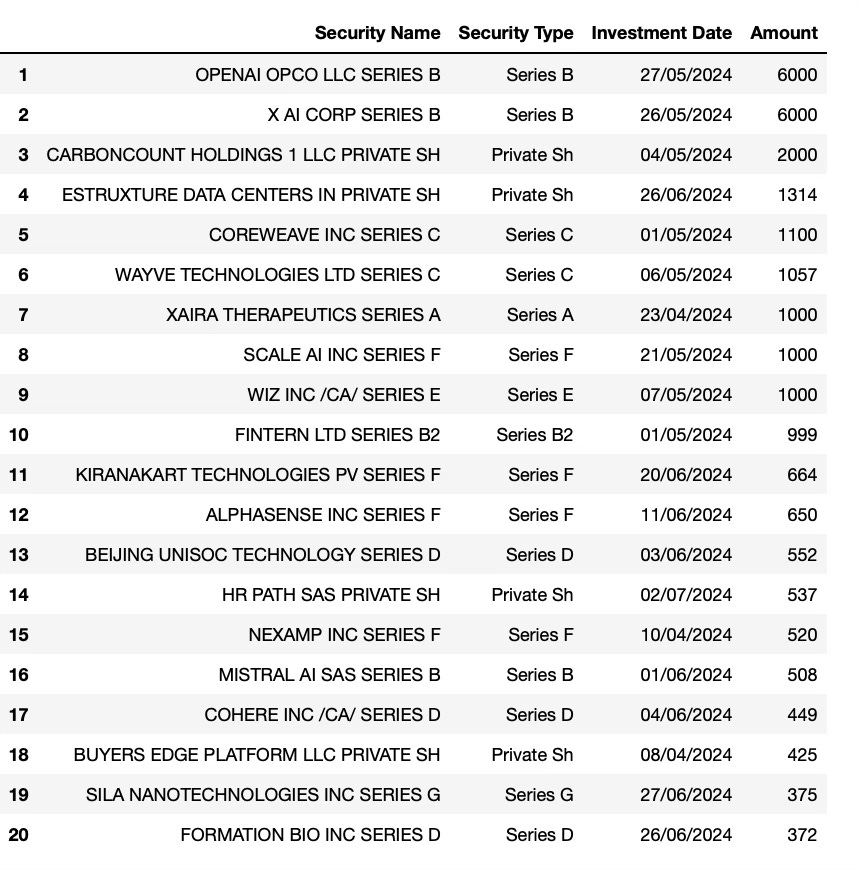

Top Deals in Q2 2024

There were 227 deals in Q2 with a stated value over $50 million. In Q1 it was 188.

At the bottom is the link to the full deal dataset.

The RAD (renewables, AI, datacenters) trend we saw last quarter continues.

Lots of big AI deals.

According to the FacstSet data Open AI raised $6bn in a Series B, but I don’t see any news or press releases on this.

X AI raised $6bn at a valuation of $24 billion. Not bad for a company that was founded 1 year ago.

xAI is pleased to announce...

Our Series B funding round of $6 billion with participation from key investors including Valor Equity Partners, Vy Capital, Andreessen Horowitz, Sequoia Capital, Fidelity Management & Research Company, Prince Alwaleed Bin Talal and Kingdom Holding, amongst others.

xAI has made significant strides over the past year. From the announcement of the company in July 2023, to the release of Grok-1 on X in November, to the recent announcements of the improved Grok-1.5 model with long context capability, to Grok-1.5V with image understanding, xAI’s model capabilities have improved rapidly. With the open-source release of Grok-1, xAI has opened doors for advancements in various applications, optimizations, and extensions of the model.

PE money continues to pour into renewables.

Carbon Count Holdings is a partnership between KKR and Hannon Armstrong Sustainable Infrastructure Capital (ticker HASI) to invest $2bn in clean energy projects.

HASI and KKR have each made an initial capital commitment of up to $1 billion to CCH1, to invest up to an aggregate of $2 billion in clean energy assets over the next 18 months. HASI will source the investments for and manage CCH1, remain the interface with its clients, and measure the avoided emissions of all investments in CCH1 using its proprietary CarbonCount® scoring tool. These investments will be consistent with HASI’s existing investment strategy which is focused on behind-the-meter, grid-connected, renewable natural gas and transport projects.

Data centres continue to suck up a lot of money.

Estruxture a Canadian datacenter company raises $1.3bn to build data centres in Canada.

TORONTO AND MONTREAL, CANADA – June 19, 2024 – Amid soaring global demand for data storage and the processing of vast amounts of digital information, Fengate Asset Management (“Fengate”) and eStruxture Data Centers (“eStruxture”) are pleased to announce the completion of a groundbreaking $1.8 billion CAD transaction, setting a new standard for innovation and growth in the Canadian technology sector.

Coreweave is an AI hyperscaler (datacenters). They raised $1.1bn from Coatue and have raised $14bn in financing over the last 12 months with debt financing from Blackstone. Note they are also going to set up a London office and invest $1.25bn in the region.

CoreWeave Secures $7.5 Billion Debt Financing Facility led by Blackstone and Magnetar

Reinforces CoreWeave’s market position as the AI hyperscaler

Builds on CoreWeave’s significant momentum, evidenced by over $12 billion raised from equity and debt investors over the last 12 months

Historic financing builds on the Company’s recently announced $1.1 billion Series C and $2.3 billion debt raise in 2023

Investment represents one of the largest private financings in history

New funding will be used to support the market’s unprecedented demand for CoreWeave’s specialized AI cloud infrastructure

“CoreWeave is building the infrastructure to power the AI innovations that are already changing how businesses operate in the global economy,” said Michael Intrator, CoreWeave CEO and co-founder. “The caliber of investors in this large debt financing round is a powerful testament to both the insatiable market appetite for AI infrastructure and their belief in CoreWeave’s ability to deliver cutting edge innovation for the largest AI labs and innovators at scale. And we are really just getting started – our ambitions are to help reshape the cloud landscape, accelerate the AI race, and power the next generation of AI innovation that is changing the course of history.”

Wayve (Autonomous driving)

Wayve announces a $1.05 billion Series C investment round led by SoftBank Group (“SoftBank”), with contributions from new investor NVIDIA and existing investor Microsoft, to accelerate its mission to reimagine autonomous mobility through embodied intelligence.

Xaira (AI biotech) raised $1bn from Foresight Capital and ARCH Ventures.

“The models understand protein chemistry very well at this point,” he says. “We think we are making progress towards understanding chemistry at its core, so we can generate matter of all kinds, not just protein matter.”

Scale AI, an AI data foundry raises $1 bin from everyone.

Today, we’re announcing that Scale has closed a $1B financing transaction at a $13.8B valuation. The financing, a mix of primary and secondary, is led by existing investor Accel with nearly all of our existing investors participating: Y Combinator, Nat Friedman, Index Ventures, Founders Fund, Coatue, Thrive Capital, Spark Capital, NVIDIA, Tiger Global Management, Greenoaks, and Wellington Management. We also are excited to welcome new investors: Cisco Investments, DFJ Growth, Intel Capital, ServiceNow Ventures, AMD Ventures, WCM, Amazon, Elad Gil, Meta, and Qualcomm Ventures.

WIZ, cybersecurity for data centres raised $1 billion at a $12 billion valuation, led by Andreessen Horowitz, Lightspeed Venture Partners, and Thrive Capital.

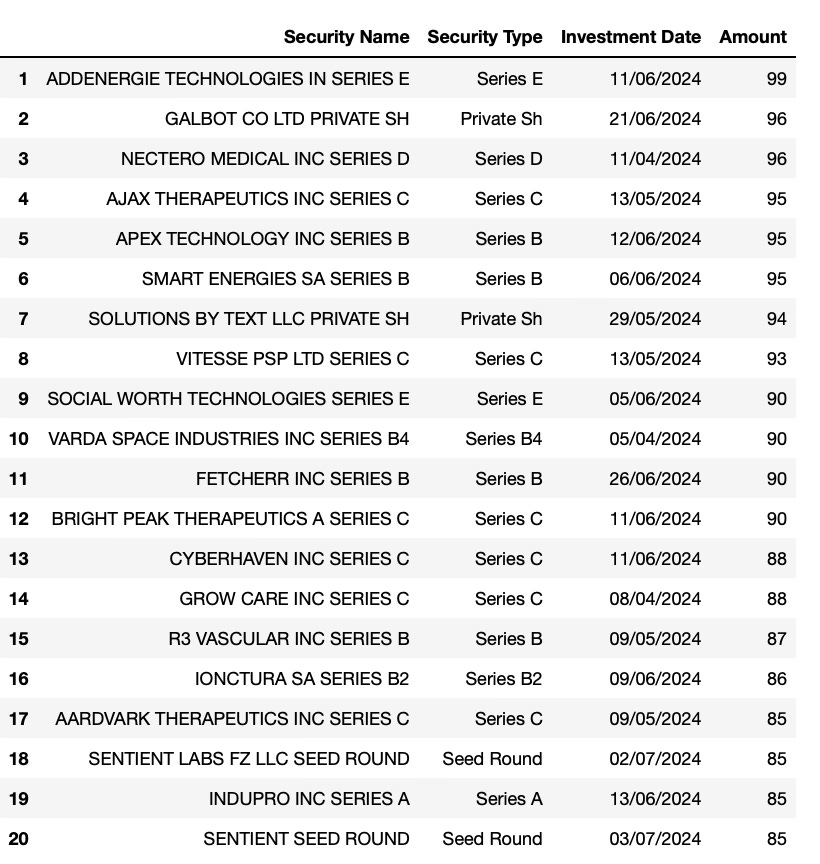

Top 20 Deals under $100mn

Again, the full deal dataset is available at the bottom.

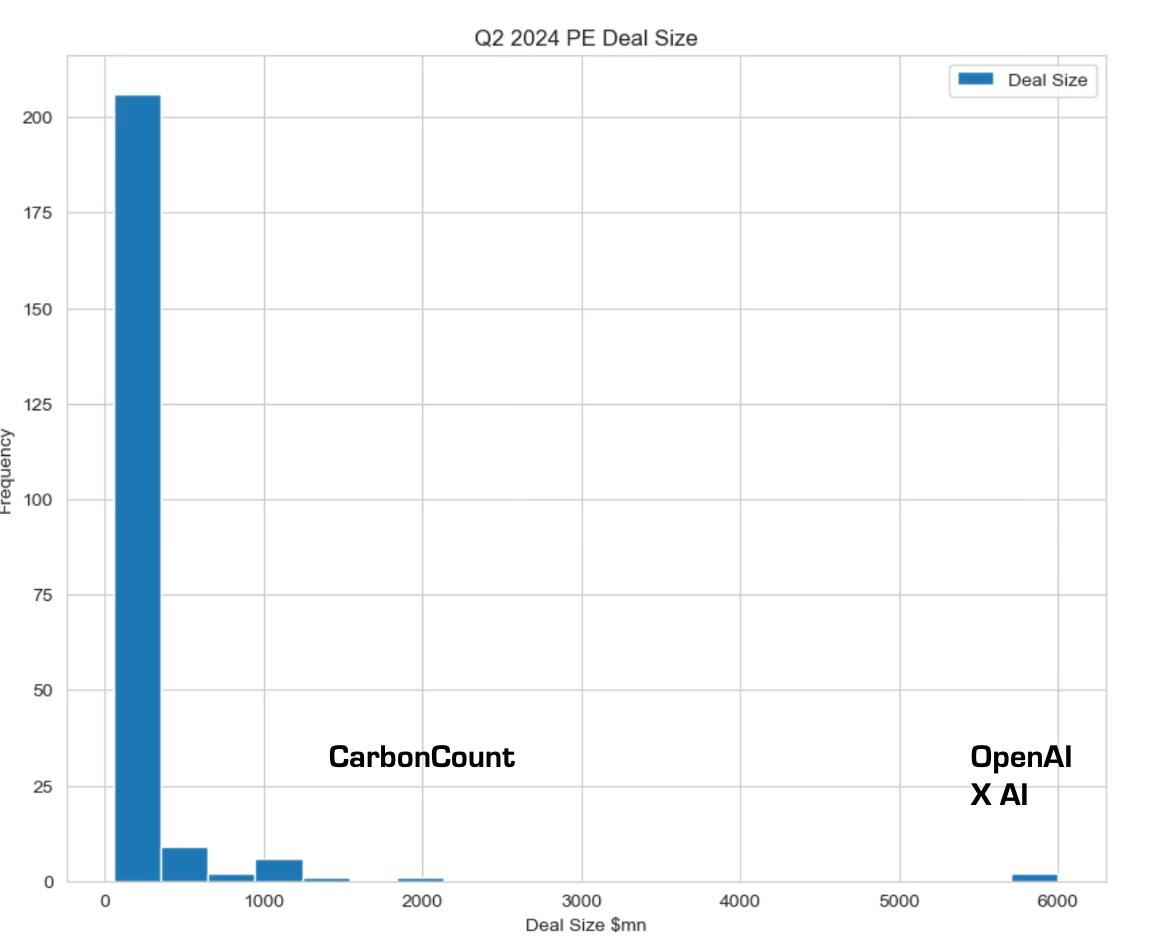

Histograms of Deal Activity by Size

As you can see the OpenAI and X AI deals are outliers.

This quarter is notable for the number of $1bn deals.

Most deals are below $100mn.

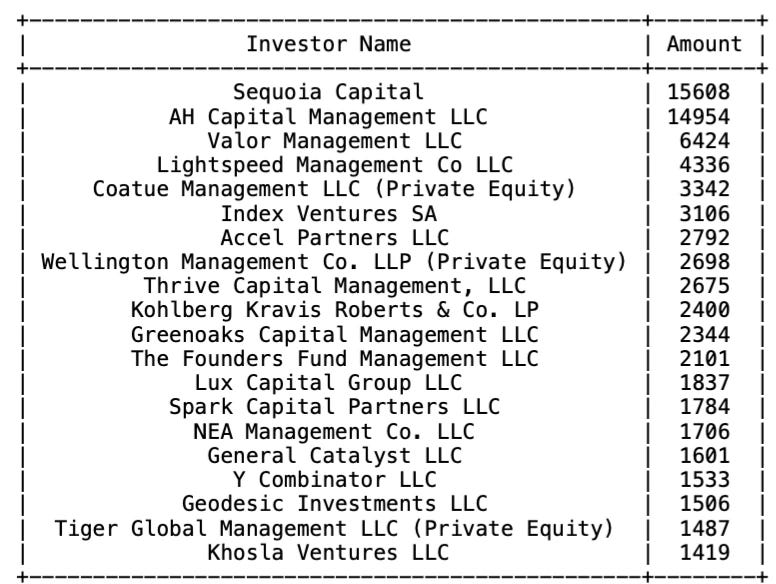

Most Active Funds Q2 2024

To calculate fund activity I sum every deal where a fund is participating. The data doesn’t show each fund’s $ participation in a deal, so funds participating in big deals, like the Open AI and X AI deal, come out looking as most active.

There were 227 deals in Q2 2024 with a stated value over $50mn.

Sequoia was the most active firm in Q2 followed by AH Capital.

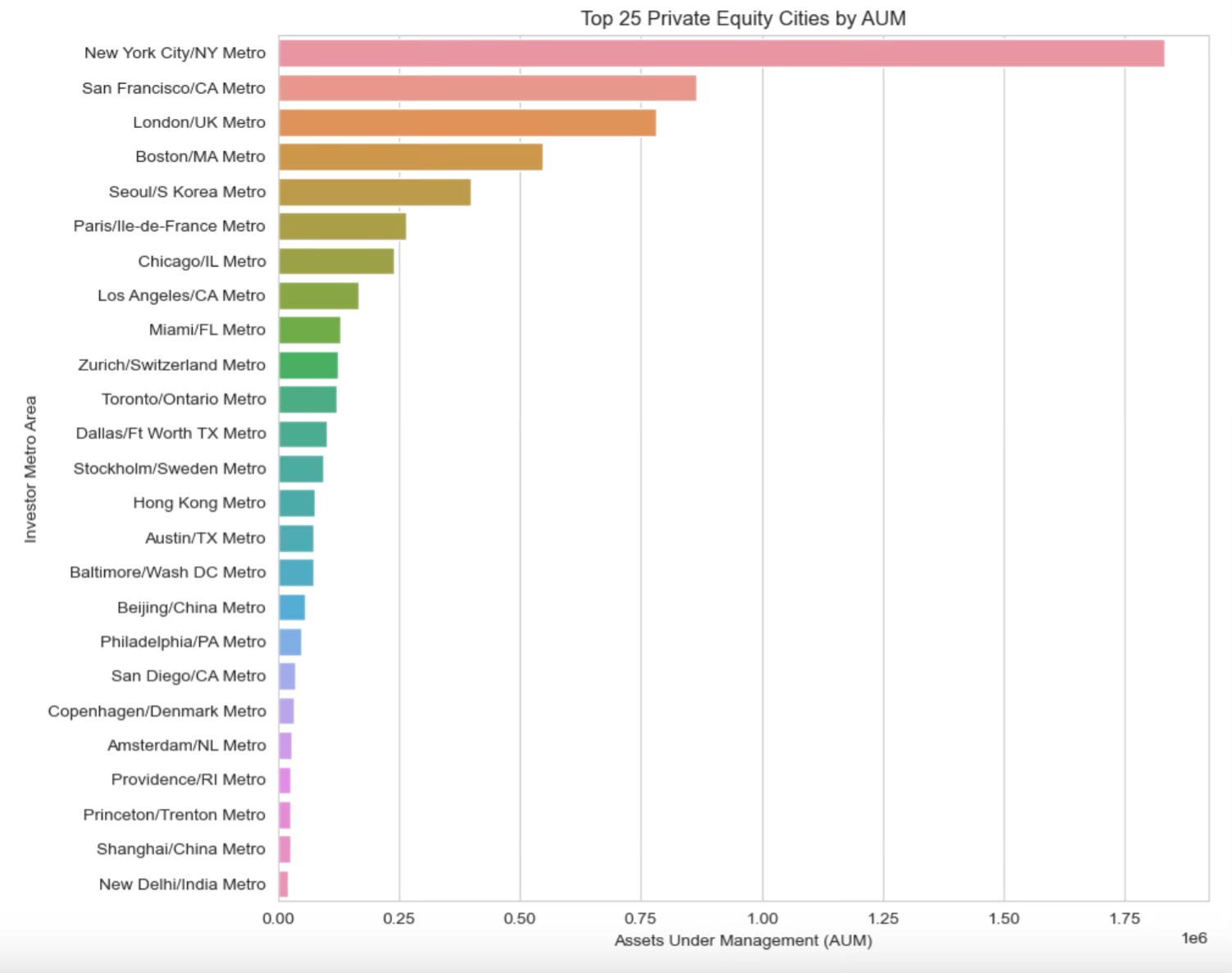

Biggest Cities Globally for Private Equity and VC by AUM

We grouped 931 global PE & VC firms by city and AUM.

If you were wondering about New York, it doesn’t seem to be going anywhere.

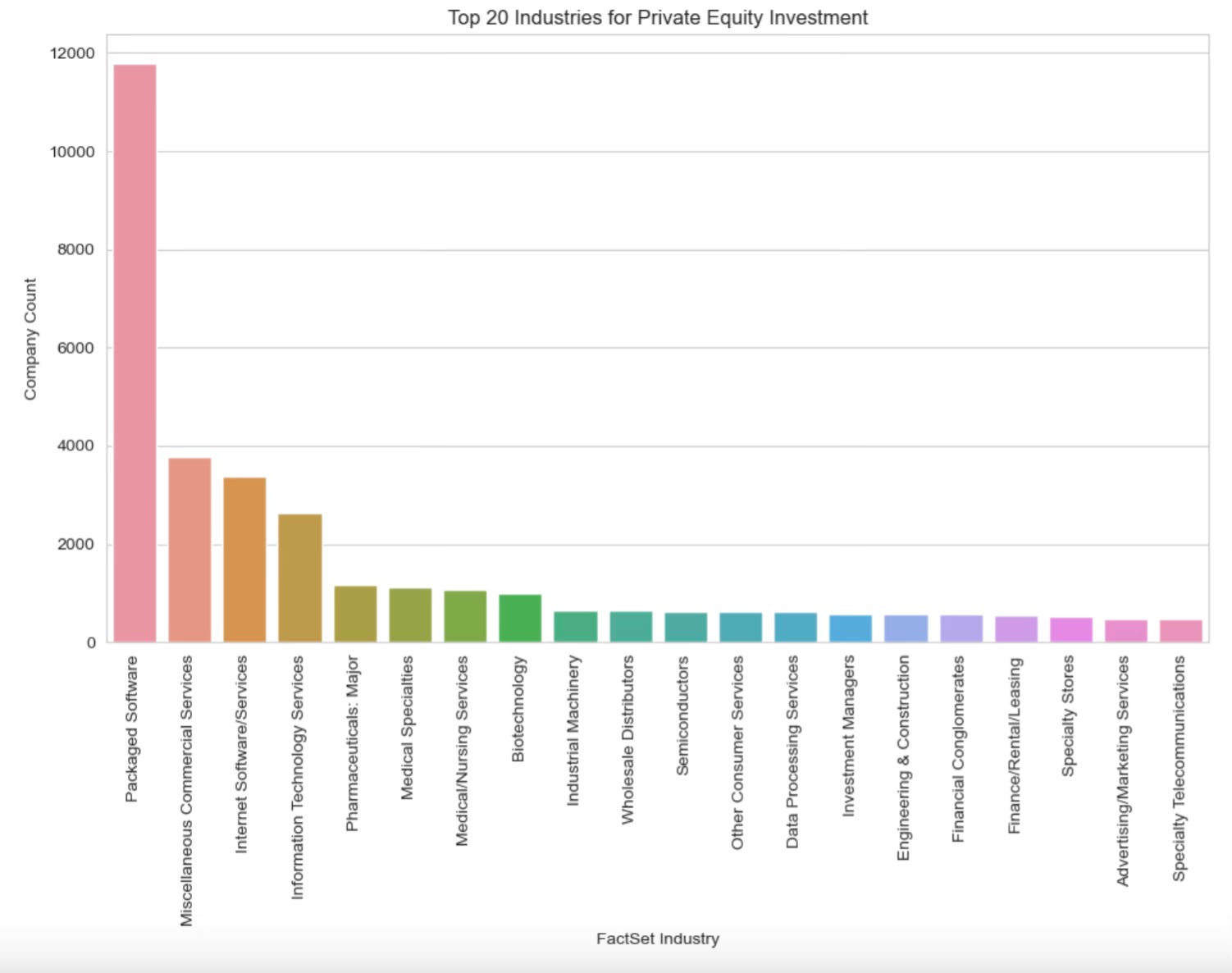

Favorite Industries for PE & VC Investment.

We grouped 45,900 PE & VC portfolio companies by Industry.

Software is by far the favorite industry (over 11,700 portfolio companies).

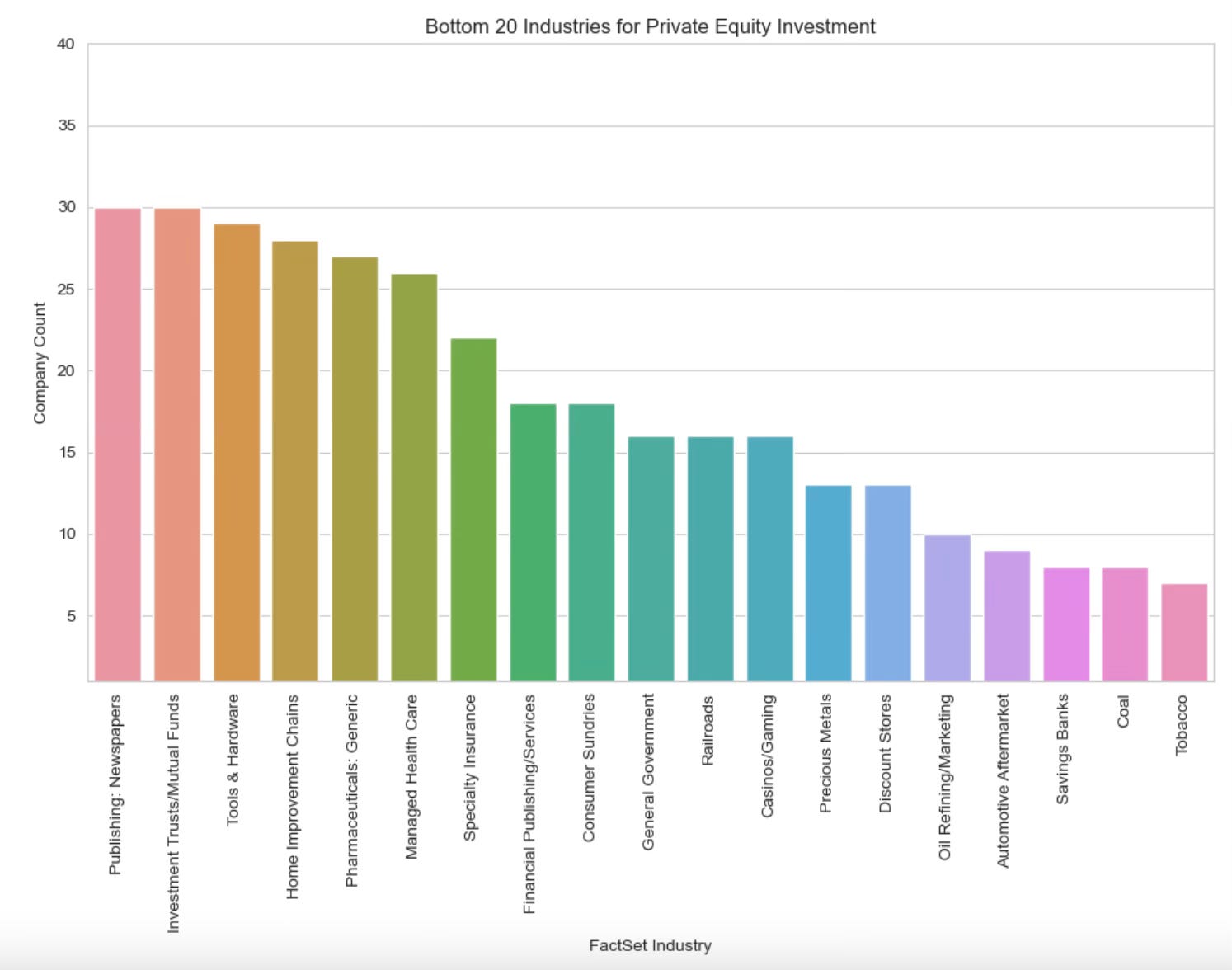

Least Favorite Industries for PE & VC Investment

Everything YWR owns. tobacco, coal, refining, precious metals, casinos, and insurance.

It’s also interesting that managed healthcare is on the list. That’s another sector we are starting to get interested in (Tenet)

Below is a link to the full Q2 2024 deal spreadsheet.

You can sort by deals, or by PE/VC firm activity.

It’s about 2,900 line items.