YWR: PE/VC Q3 Deal Tracker

Situational Awareness; knowing what’s going on in the other asset classes. So every quarter we check in and review the top private equity and venture capital deals.

Full database at the bottom of the post.

But first a YWR Public Service Announcement: I’m going to be in Hong Kong next week from the 26th and would love to meet you. Can I buy you a coffee or a beer? Send me a message.

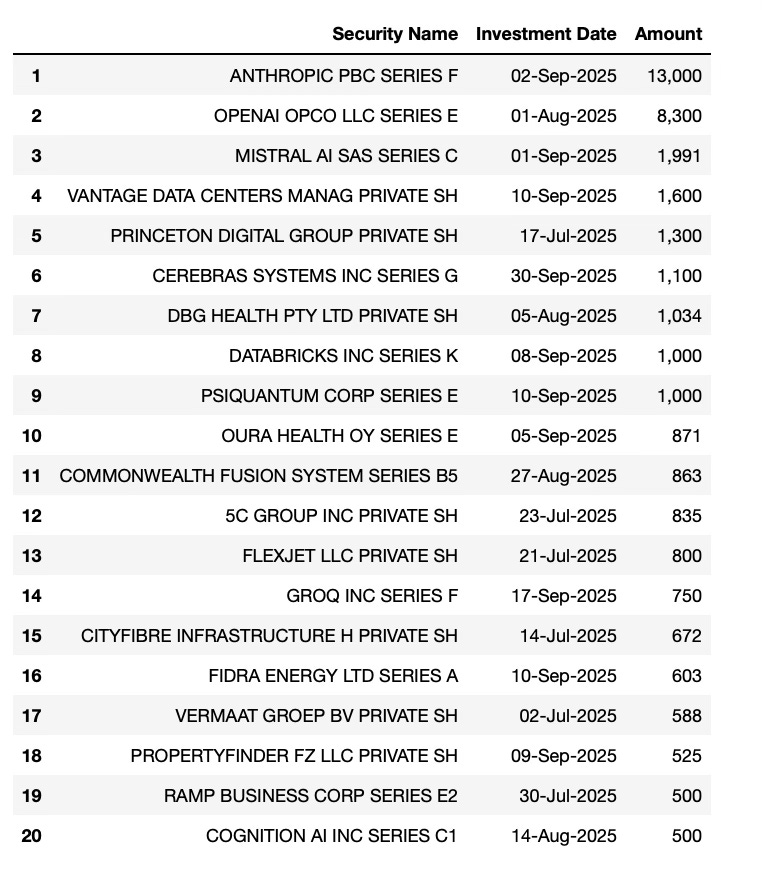

Top 20 Deals

Traditional PE deals often don’t disclose their terms, so our data for the top deals each quarter skews to growth/venture deals where the capital raise amounts are disclosed.

The OpenAI deal is data from a prior round so ignore it.

Anthropic’s: $13bn raise was the big deal of the quarter and pretty much everyone went in. You notice this trend of traditional asset managers like Fidelity, Baillie Gifford, T. Rowe getting more involved in private deals. And Jane Street. Interesting. I love Jane Street.

Along with ICONIQ, the round was co-led by Fidelity Management & Research Company and Lightspeed Venture Partners. The investment reflects Anthropic’s continued momentum and reinforces our position as the leading intelligence platform for enterprises, developers, and power users.

Significant investors in this round include Altimeter, Baillie Gifford, affiliated funds of BlackRock, Blackstone, Coatue, D1 Capital Partners, General Atlantic, General Catalyst, GIC, Growth Equity at Goldman Sachs Alternatives, Insight Partners, Jane Street, Ontario Teachers’ Pension Plan, Qatar Investment Authority, TPG, T. Rowe Price Associates, Inc., T. Rowe Price Investment Management, Inc., WCM Investment Management, and XN.

The hook is that Anthropic’s run rate revenue jumped from $1bn in March 2025, to $5 bn by August. Claude Code is where Anthropic is leading. Everyone says Claude Code is the best. Even Brad.

Claude Code has taken off—already generating over $500 million in run-rate revenue with usage growing more than 10x in just three months.

Mistral: I’d say Europe is completely missing the boat on everything, but at least there is Mistral and ASML who supported their EUR 1.7bn raise.

“ASML is proud to enter a strategic partnership with Mistral AI, and to be lead investor in this funding round. The collaboration between Mistral AI and ASML aims to generate clear benefits for ASML customers through innovative products and solutions enabled by AI, and will offer potential for joint research to address future opportunities.” said ASML CEO Christophe Fouquet.

It looks like Mistral is trying to carve out a niche as AI for the industrial sector.

Then of course there are the datacenter deals.

Vantage Data Centres: A $1.6bn raise to build out Asia Pacific datacenters led by ADIA and GIC. A lot of the money is going to go to expanding their JHB1 campus in Malaysia. Malaysia is becoming a hub for Asia-Pac datacenters.

Set on nearly 73 acres, the Johor campus, to be known as JHB1, will deliver more than 300MW of IT capacity across three cutting-edge data centers. The campus, located in the Johor-Singapore Special Economic Zone, offers dark fiber connectivity due to its close proximity to other data center markets in the region. It features sustainability-forward technologies, including direct-to-chip liquid cooling, and is on track to meet EDGE certification requirements.

Johor is fast becoming one of Southeast Asia’s most strategic data center hubs. Benefiting from its proximity to Singapore to capture spillover demand, competitive land and operating costs, and strong government incentives.

Princeton Digital Group: Another Asia-Pac data center deal with $1.3bn from Stonepeak.

5C Group: $835mn for datacenters from Brookfield and Deutsche Bank.

Cerebras is an interesting one. They built a supersized AI chip which they say is 20x faster than an Nvidia GPU. They are also building their own cloud (networked Cerebras datacenters) of CS-3 chips.

Sunnyvale, CA – September 30, 2025 – Cerebras Systems, makers of the fastest AI infrastructure in the industry, today announced the completion of an over subscribed $1.1 billion Series G funding round at $8.1 billion post-money valuation. The round was led by Fidelity Management & Research Company and Atreides Management. The round included significant participation from Tiger Global, Valor Equity Partners, and 1789 Capital, as well as existing investors Altimeter, Alpha Wave Global, and Benchmark.

As the fastest inference provider in the world, Cerebras will use these funds to expand its pioneering technology portfolio with continued inventions in AI processor design, packaging, system design and AI supercomputers. In addition, it will expand its U.S. manufacturing capacity and its U.S. data center capacity to keep pace with the explosive demand for Cerebras products and services.

“From our inception we have been backed by the most knowledgeable investors in the industry. They have seen the historic opportunity that is AI and have chosen to invest in Cerebras,” said Andrew Feldman, co-founder and CEO, Cerebras. “We are proud to expand our consortium of best-in-world investors.”

Databricks: Snowflake and Databricks and seem similar, but what strikes me is it seems Databricks is doing better as a private company, than Snowflake which IPO’d.

If Snowflake tried to raise $1bn right now the stock would die. However, in PE world, they love it if you raise money. Your valuation goes up. In December it was valued at $60bn, now it’s $100bn. While Snowflake is stuck at $85bn. They both seem to have a $4bn revenue run rate.

It’s cool that institutional investors in the US are throwing so much money at the hardest science problems in the world (quantum computing and fusion). The world will definitely benefit. I hope the shareholders do too.

PSI Quantum: raised $1 billion to build the world’s first fault-tolerant quantum computer. Cool promo video.

Led by funds and accounts managed by affiliates of BlackRock, along with Temasek and Baillie Gifford, this fundraising values the company at $7 billion and brings in new investors, including entities administered by Macquarie Capital, Ribbit Capital, NVentures (NVIDIA’s venture capital arm), Adage Capital Management, Qatar Investment Authority (QIA), Type One Ventures, Counterpoint Global (Morgan Stanley), 1789 Capital, and S Ventures (SentinelOne). The round also included participation from existing investors including Blackbird, Third Point Ventures, and T. Rowe Price Associates, Inc.

Commonwealth Fusion (CFS): I think the French will about die if Commonwealth Fusion or Pacific Fusion commercialise fusion first. France has hosted the ITER fusion project in the South of France since 1985 but the ITER reactor has defects in the cooling system and is decades behind schedule (no surprise). So Silicon Valley decided to take matters into its own hands. CFS is targeting power to the grid in Virginia by 2030.

“CFS offers investors the clearest path to bringing commercial fusion to the world — and an unprecedented opportunity to make a real impact as global demand for power accelerates with electrification and increased use of AI and data centers,” said Ally Yost, Senior Vice President of Corporate Development at CFS. “Along with the promise of energy independence and security, fusion power will help to expand energy access, and with it, improve quality of life.”

Of course, the promise of free energy brings in every possible investor in the world, including lots of Japanese. So why only raise $863mn?

New investors in CFS include (in alphabetical order): Brevan Howard Macro Venture Fund; Counterpoint Global (Morgan Stanley); Stanley Druckenmiller;FFA Private Bank (Dubai) Ltd.; Galaxy Interactive, a venture platform within Galaxy Digital Inc. (NASDAQ: GLXY); Gigascale Capital; HOF Capital; Neva SGR (Intesa Sanpaolo Bank); NVentures (NVIDIA’s venture capital arm); Planet First Partners; Woori Venture Partners US; and others committed to the mission of commercializing fusion energy.

A consortium of 12 Japanese companies led by MITSUI & CO., Ltd. and Mitsubishi Corp. also participated. The Japanese consortium included Development Bank of Japan Inc.; Fujikura Ltd.; JERA Co., Inc.; JGC JAPAN CORP.; Mitsui Fudosan Co., Ltd.; Mitsui O.S.K. Lines, Ltd.; NTT Inc.; Sumitomo Mitsui Banking Corp.; Sumitomo Mitsui Trust Bank Ltd.; and The Kansai Electric Power Co., Inc.

They join existing CFS investors who increased their stakes, including Breakthrough Energy Ventures; Emerson Collective; Eni; Future Ventures; Gates Frontier; Google; Hostplus Superannuation Fund; Khosla Ventures; Lowercarbon Capital; Safar Partners; Eric Schmidt, former CEO of Google; Starlight Ventures; Tiger Global; a large state pension fund and others who support CFS’ leadership in this energy transition.

Finally, I’m going to mention the CityFiber deal. It’s kind of boring (fiber, so 1990’s), but notable that the deal included a debt facility from the UK Wealth Fund. The Wealth Fund is the UK’s effort to invigorate tech investment in the UK. It looks promising, but it looks like it has the typical internal conflict of whether this is about investing in technology or ‘NetZero’. Hopefully, they can shake the NetZero nonsense and be more like the Middle East funds.

CityFibre, the UK’s largest independent full fibre platform, has reached agreement with its shareholders and existing lenders on a major £2.3bn financing round, accelerating its next phase of growth.

The financing includes £500m in new equity secured from CityFibre shareholders, Infrastructure at Goldman Sachs Alternatives, Antin Infrastructure Partners, Mubadala Investment Company and Interogo Holding, underscoring their continued commitment to CityFibre’s long term strategy and the company’s role in providing critical digital infrastructure across the UK.

CityFibre has also agreed a committed £960m expansion of its existing debt facilities, supported by lenders including ABN AMRO, BBVA, Crédit Agricole CIB, ING, Intesa Sanpaolo IMI CIB, Lloyds, the National Wealth Fund, NatWest, SEB and Société Générale.

Side note: Are our European banks starting to lend again?

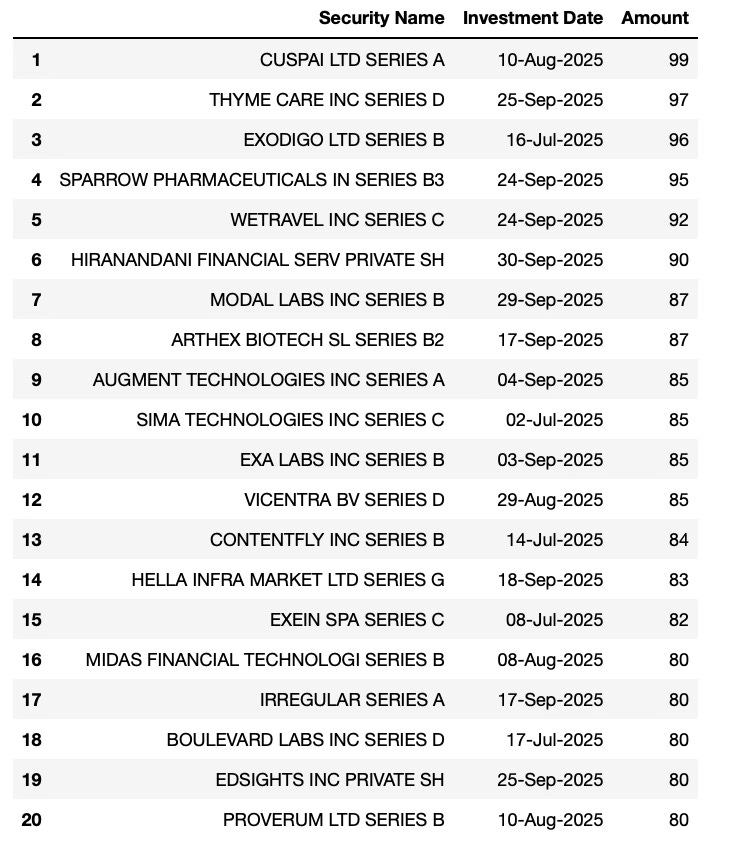

Top Deals under $100mn

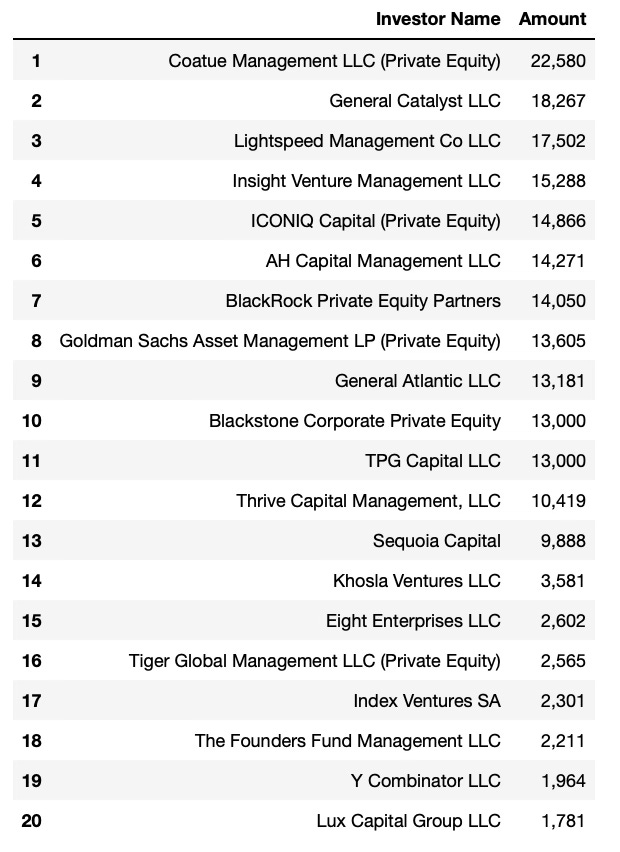

Most Active Funds Q3 2025

The way I calculate the most active funds each quarter is flawed, but I do it anyways. It’s the sum of the deal values for every investment round where a fund was involved. So if you were in the Anthropic deal this quarter it makes you look the most active.

ICONIQ is a great success story. Love it. And amazing they have grown to the point of leading the Anthropic deal.

Lightspeed also seems to be on the up.

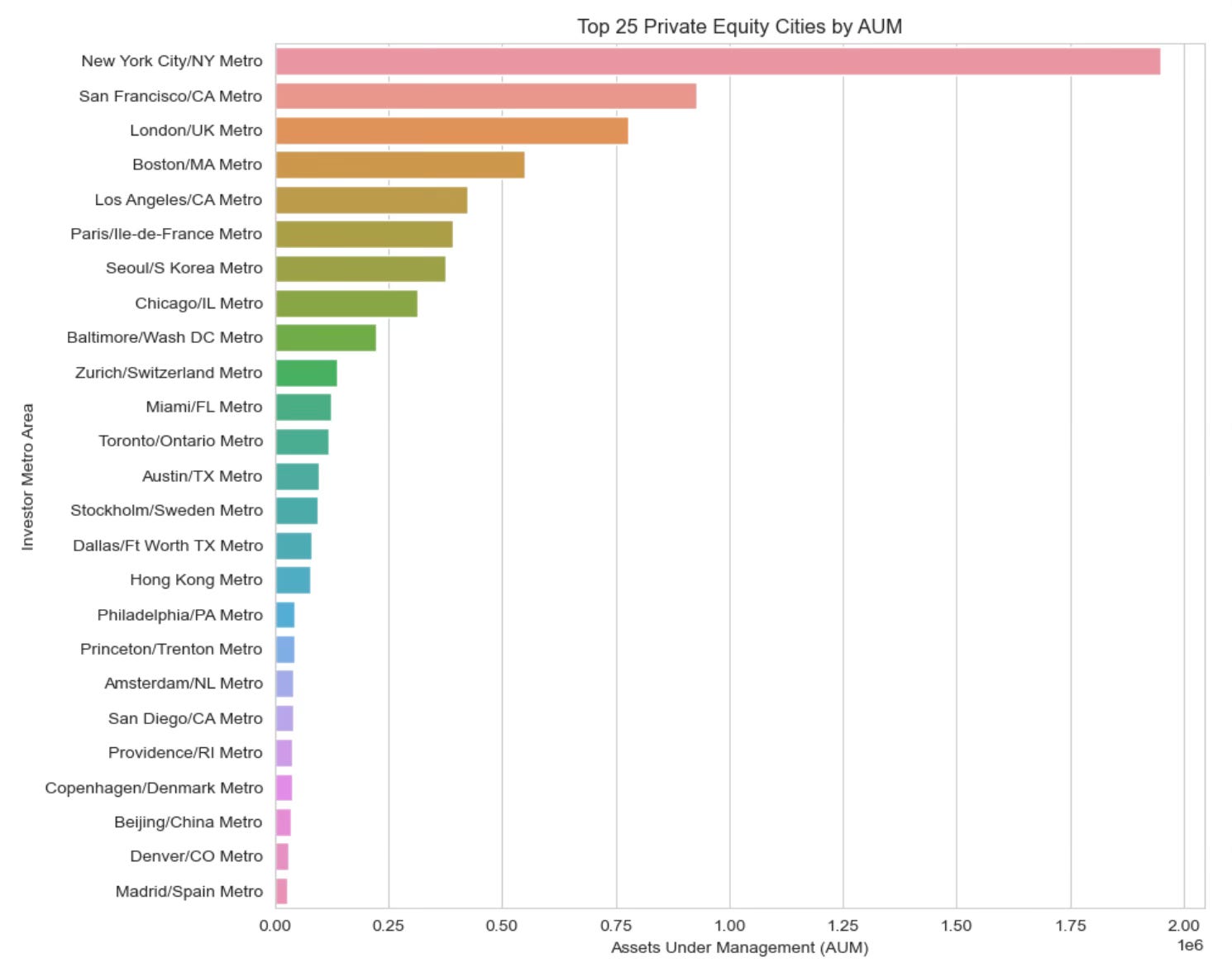

Top Cities for Private Equity and Venture Capital

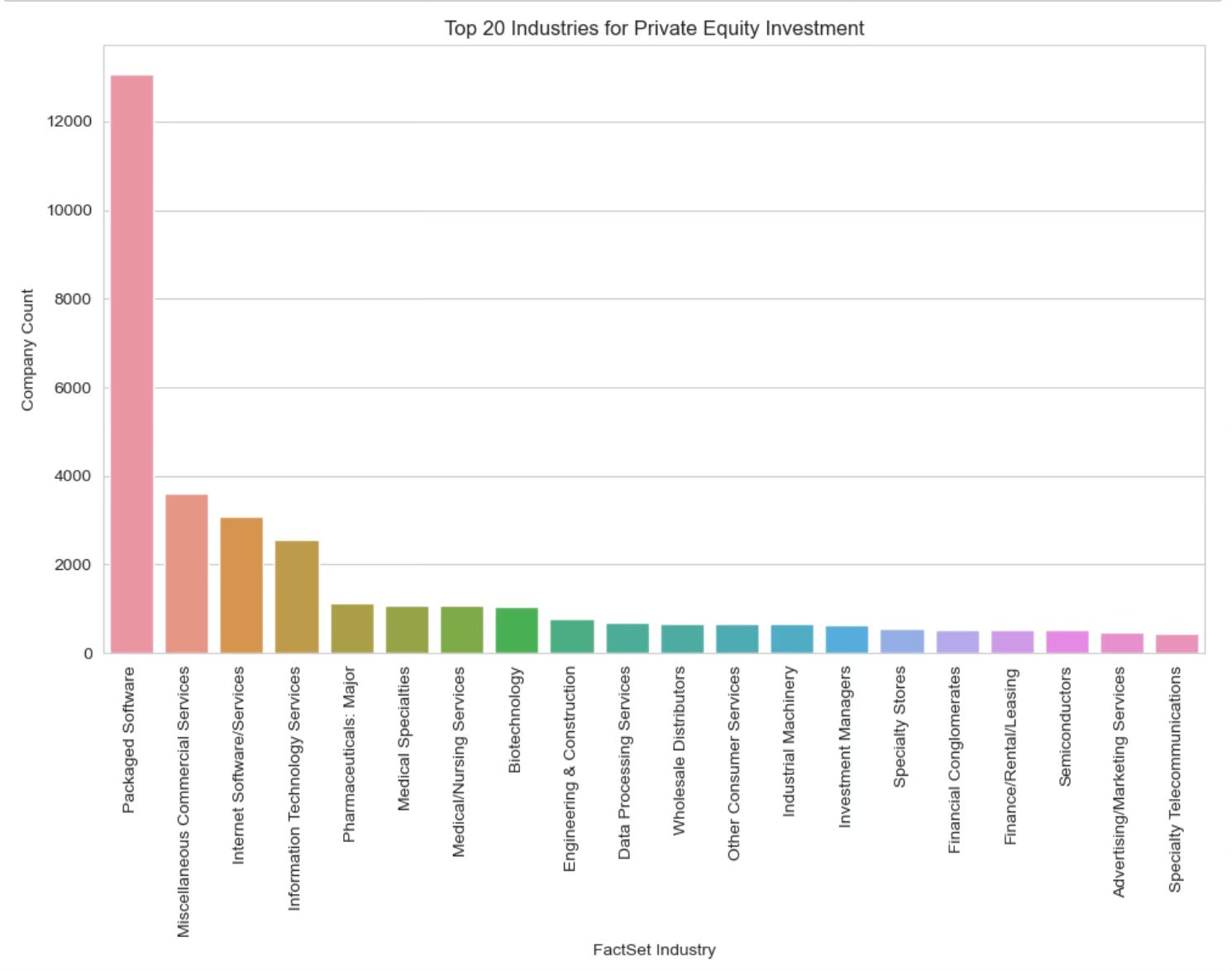

Top Industries for PE and VC investment.

This is where I go through 47,000 PE and VC fund holdings by industry. You see that 40% of the investments are in software, internet, or IT services (18,723 companies).

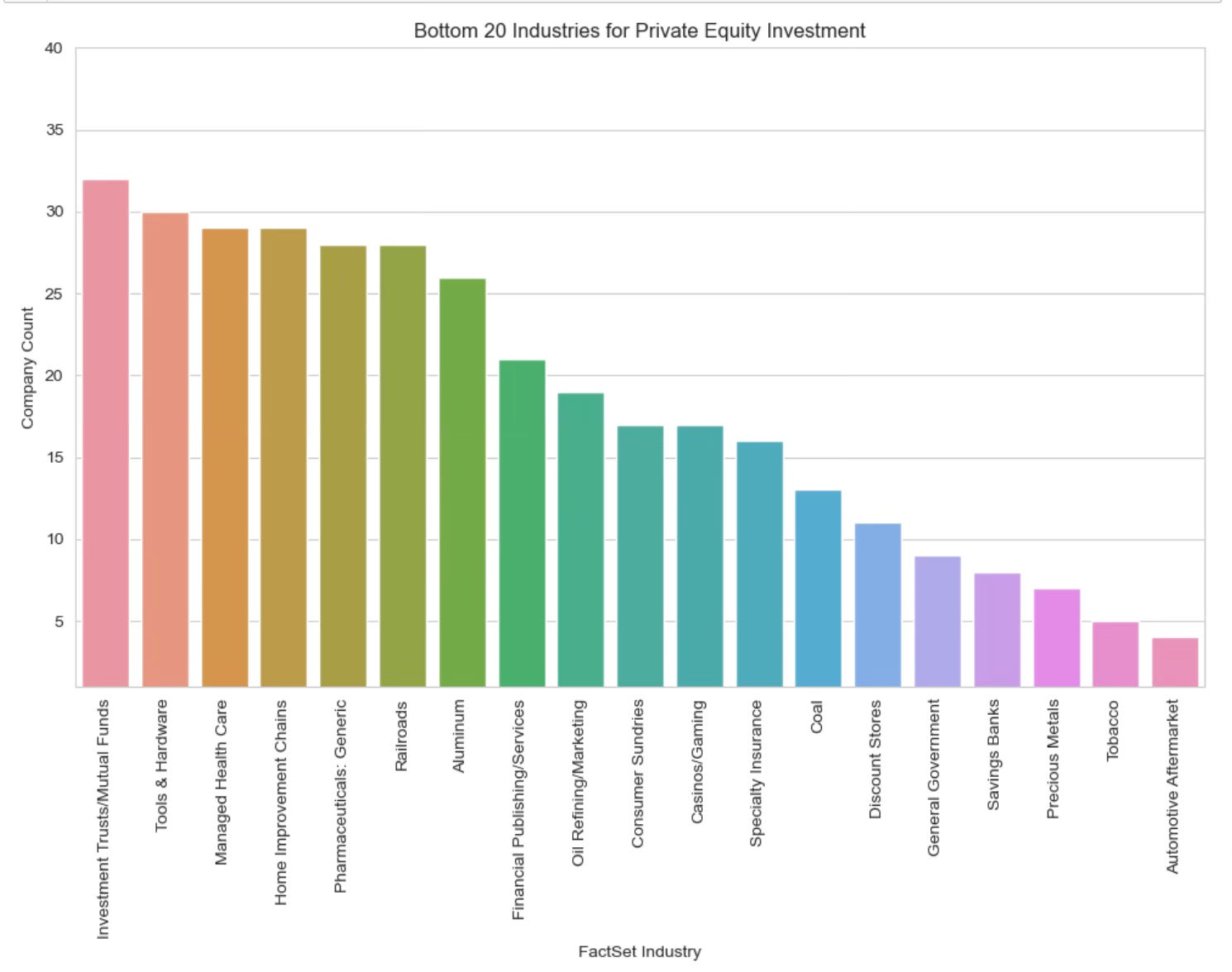

Then you look at the bottom 20 industries. This is where PE/VC doesn’t invest. Automotive parts, gold miners, specialty insurance, railroads, managed healthcare…. I’m hesitant to give advice, but couldn’t these older industries be interesting in the future? Maybe they don't suck up enough capital.

Below is a link to the data with all the deals during the quarter.

Take a look on your own. Sometimes you find interesting things. Like did you know TPG bought the Boston Celtics?

Full deal database for Q3: