YWR: Searching for Unsustainability

Disclosure: These are personal views, not investment recommendations to buy or sell a security. For investment advice seek professional help.

I used to find the word ‘unsustainable’ annoying.

I would hear it all the time.

A lot of enjoyable activities are ‘unsustainable’.

‘Unsustainability’ is an environmental term, but it shows up in investing too.

A common use case is:

So, and so company is making a lot of money, but those earnings and margins are ‘unsustainable’.

You will typically hear this from an analyst justifying why he/she has been too negative on a company which is doing surprisingly well. ‘Yes, they are doing well, but it’s unsustainable’. Apparently, the analyst has an understanding of the natural order of things and what the company or industry ‘should’ be earning.

Over time, I’ve trained my ears to perk up whenever I hear something is ‘unsustainable’, because more often than not there is an investment opportunity at hand.

What it really means is that a company or industry trend has changed and the consensus view hasn’t adjusted to the new reality. That’s the opportunity.

Also, because these surprisingly good earnings are ‘unsustainable’ the market doesn’t like to pay up for them, so usually you have both a positive trend and an attractive valuation (low P/E).

Hence, I’ve learned to like the word.

Unsustainable = Opportunity

Screening for Unsustainability

How can we systematically find these ‘unsustainable’ opportunities?

Thankfully, YWR has created a screen to identify 68 unsustainable opportunities (potentially, because you need to do your own work).

Methodology

Using the YWR Global Factor Model universe of over 3,000 stocks we screened for:

Companies with 0% or negative earnings growth over the next two years. Defined as FY3 EPS Estimates (2026) below FY1 (2024).

Analysts are estimating no growth, but at the same time revising up their forecasts. This is defined as positive EPS revisions for both FY1 and FY2 earnings.

YWR Estimate Revision Score above 40. I added this as an extra earnings revision check. The formula for the YWR earnings revision score is a bit of a secret sauce, but it tries to smooth out estimate changes from prior year kitchen sinking.

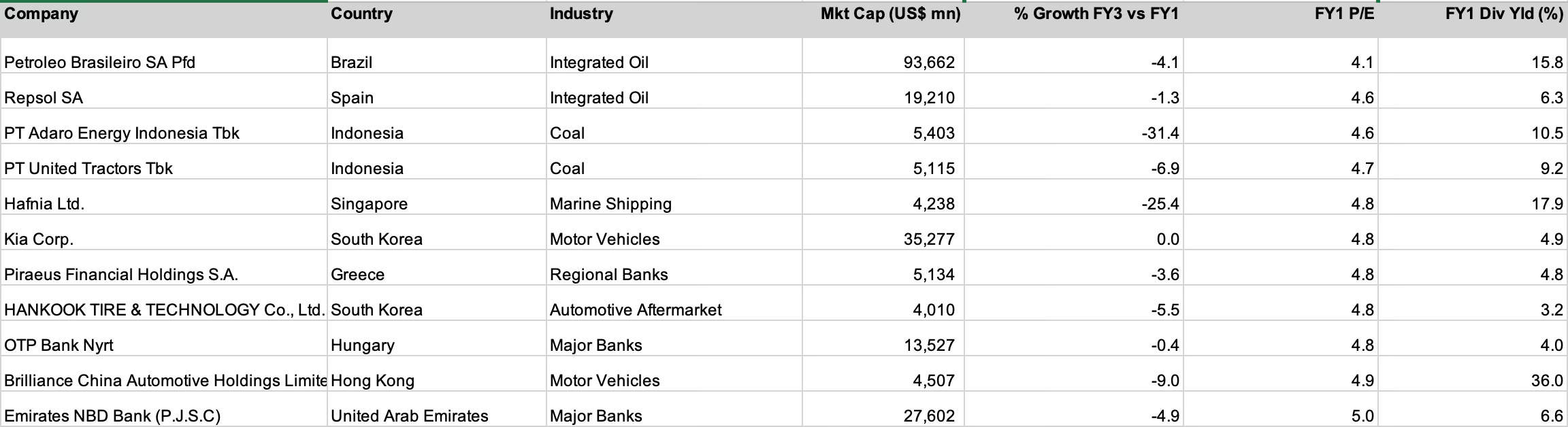

Below is a sample of 11 results from the YWR Earnings Unsustainability screen sorted by lowest P/E.

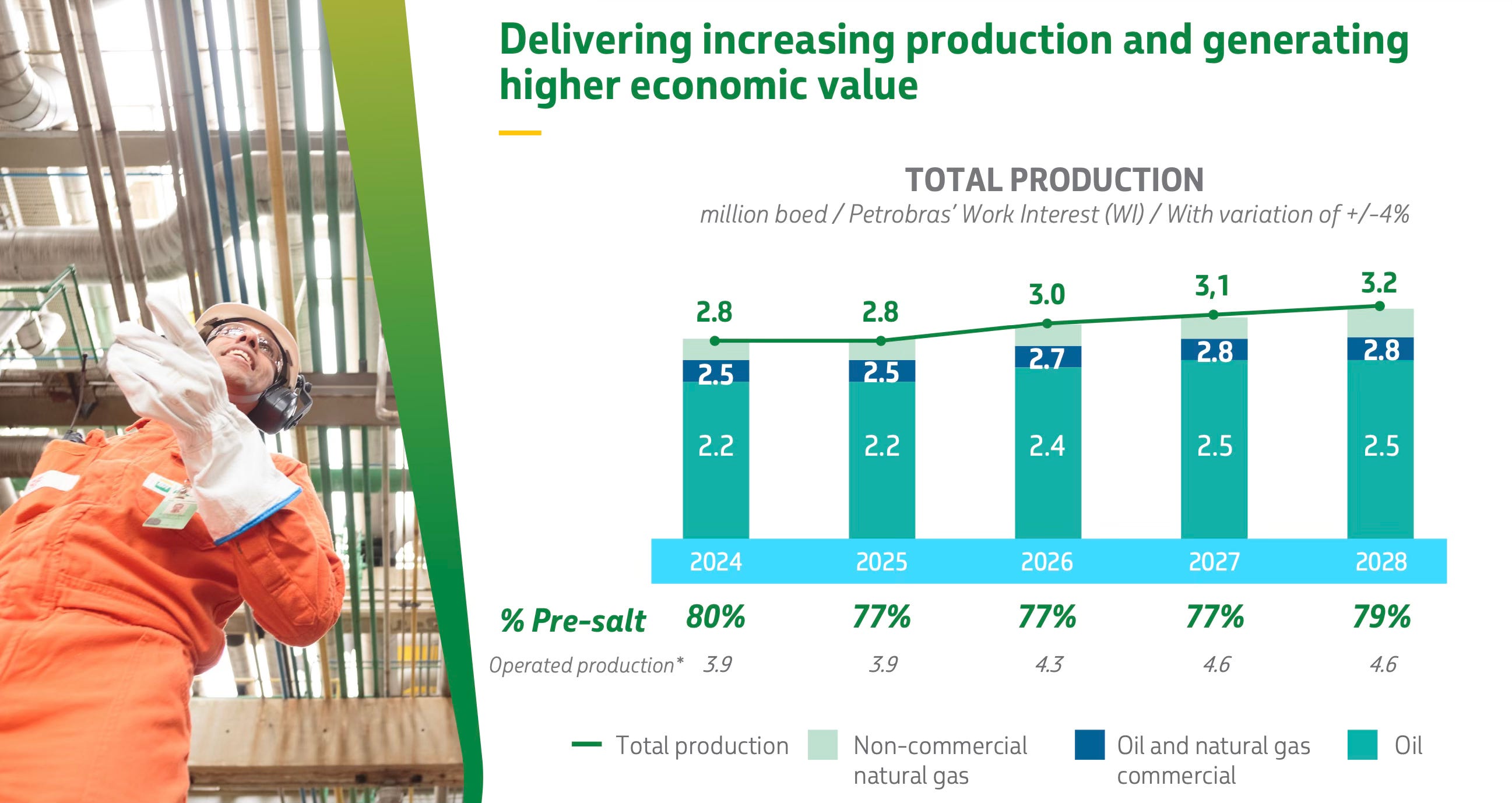

Petrobras is a good example of what we are looking for. PBR is trading on a P/E of 4x with a 15% dividend yield and earnings which are supposed to decline 4% over the next 2 years.

It’s interesting that Petrobras earnings are expected to decline over the next 2 years when they have one of the best production growth profiles in the industry as the FPSO’s are delivered and their Pre-Salt fields finally come on stream. Who knows the final dividend you’ll receive from Petrobras, but it’s likely to be a double digit yield on the current share price. See what I mean?

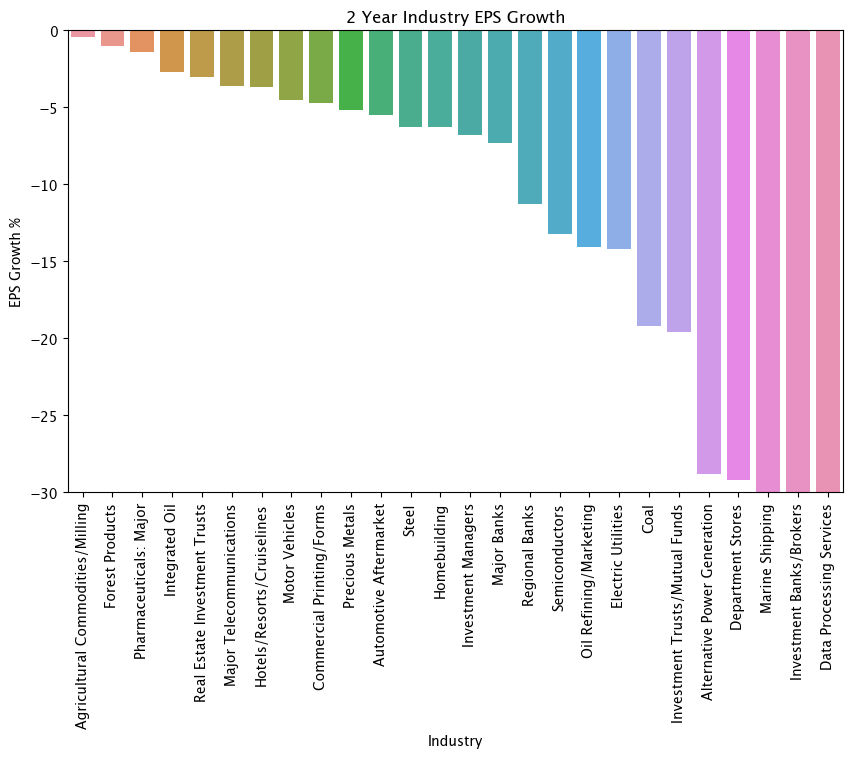

When we group the results by sector we see the top sectors for ‘Unsustainability’ are banks, shipping, utilities, gold miners, steel, department stores, oil stocks, REIT’s, coal and homebuilders.

European banks, gold miners, oil stocks… we love these sectors!

I think I’m starting to like shipping too. If we can’t stop the Houthis should can we at least figure out a way to profit from their attacks? Hafnia, for example is a chemical tanker business with a market cap of $4.2bn which has paid out $528mn in dividends over the last 12 months and locked in rates for rest of 2024 as well. You know who else likes Hafnia?

The two worst sectors for expected earnings growth are ‘Investment Banks and Data Processing’, but really this is a negative view on crypto. The ‘Investment Bank’ is Coinbase, a stock we greatly admire, (The Next Amazon), and ‘Data Processing’ is Marathon Digital, a crypto mining company. So apparently, crypto is ‘unsustainable’ too. If you’ve been a skeptic that should help make you like it.

These are the highlights but please review the screen results yourself. A link to the full screen is below.

BTW, all datasets, and earnings models used in the posts are also on www.ywr.world.