YWR: Stop caring about 'Earnings'

The Buffet Paradigm Shift

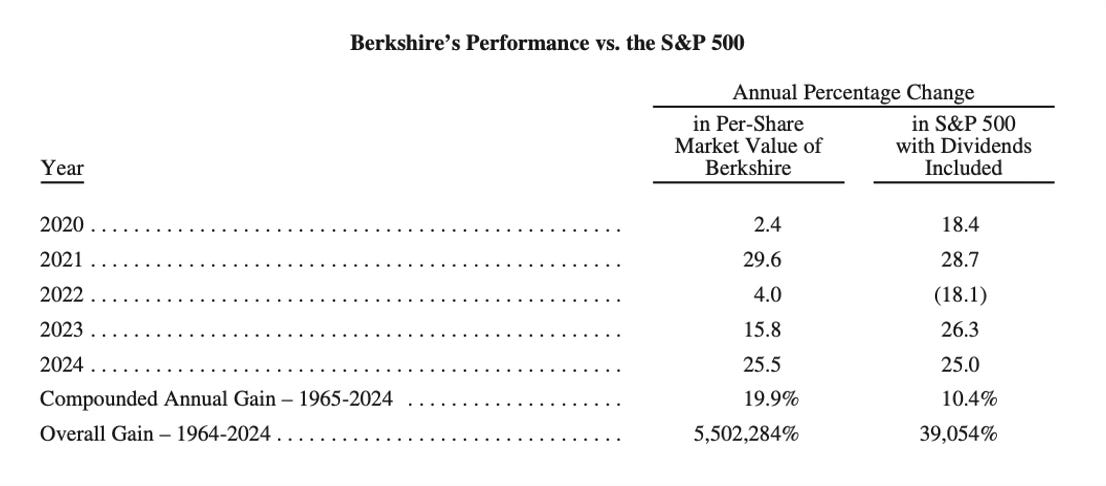

In 1965 Warren Buffet pioneered a new concept.

The no dividend company.

It was profound.

Every Wharton MBA knew the value of a company was the Net Present Value (NPV) of the dividends it would pay to shareholders in the future. I mean why else would you own shares in a company?

What would be the point of a share if it didn’t pay you money?

And yet, Buffet promised to never pay any dividends ever.

Instead, the money would be reinvested into buying more businesses. It was a compounding machine.

Nowadays it’s not revolutionary to see the value of Berkshire Hathaway, but think back to how radical this idea must have seemed to traditional finance analysts in the 1960’s.

Buffets’s insight was that paying dividends exposed investors to taxes on those dividends. There was tax leakage. Over time the compounding engine was stronger if Berkshire retained that money and reinvested it for the shareholder. The value would be captured through the Berkshire Hathaway share price, not the dividends.

This was a paradigm change for investing.

This ‘no dividend ever’ company would go on to become incredibly valuable and outperform all other companies in the S&P 500 for the next 60 years!

The Bezos Paradigm Shift

I will argue Jeff Bezos shifted the finance paradigm again, we just haven’t formalised it.

Buffet created the ‘No Dividend Company’

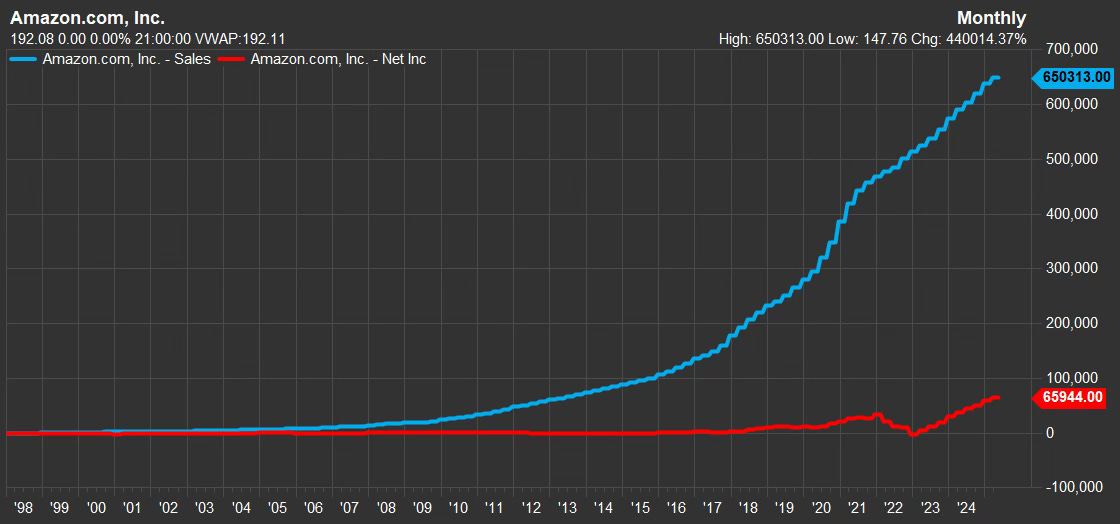

Bezos created the ‘No Earnings Company’

Bezos takes Buffet’s insight to the next logical step.

If dividends are a drag on compound growth because the shareholder has to pay tax, then reporting ‘earnings’ is also a drag. Reporting ‘profits’ exposes the company to corporate tax. These ‘taxes’ are money which could be better spent on new growth projects.

Bezos could never tell you he was doing this, but what if in September of each year he would have a private sit down with his CFO. Together, discreetly, they would do the numbers and figure out how to make sure there were no profits at the end of the year.

The CFO would say, ‘Jeff, online sales are tracking higher than expected and we are projecting a $200 million pre-tax profit this year.”

And Bezos would say ‘OK. Ramp up the two new moonshot projects we came up with and spend that $200 million. Start the online movie business idea, and start that server infrastructure platform idea.”

And so surprise, surprise, when Amazon reported results, sales would be better than expected, but at the bottom line, no profits.

Bezos can’t say this openly, but he’s thinking, “Why am I going to give the government $60 million in taxes that can be better spent on more growth projects?”

He can’t say that’s what he’s doing, so you have to read between the lines that that’s what is going on. The whole point is to not show profits and use the money to invest in growing the business. If the competitors want to focus on reporting profits and paying taxes, over the long run that’s their disadvantage.

And for investors if you said you didn’t like Amazon because the P/E was too high, you are missed the whole move. For decades. The P/E was always going to be high. It wasn’t a bug. It was a feature. It’s like saying you don’t like Berkshire Hathaway because it doesn’t pay a dividend.

The past paradigm was earnings and free cash flow.

The new era is state as little earnings as possible and use the money to grow the top line and create network effects which make you the dominant player. The value will be captured in the share price. And no tax leakage on earnings or dividends.

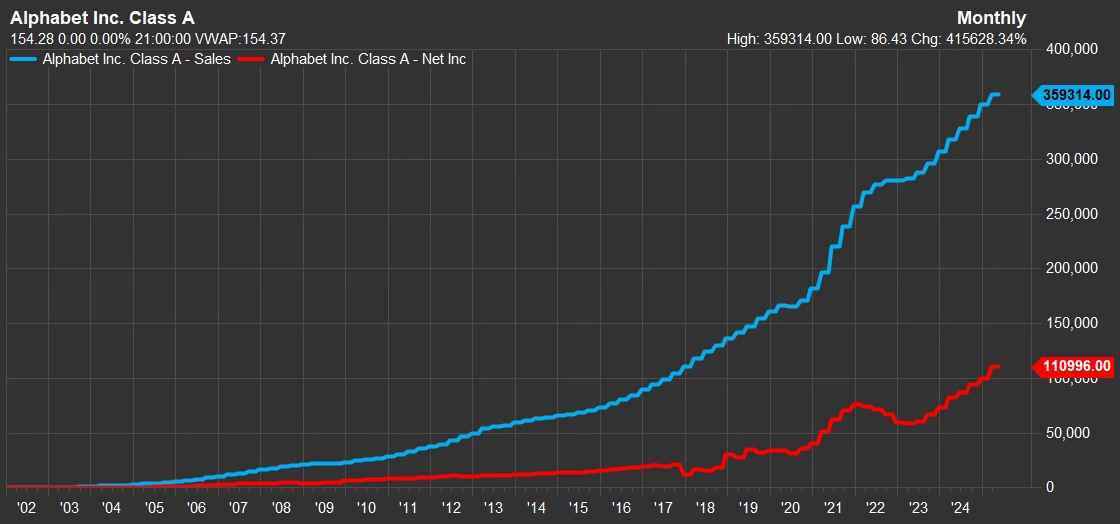

You see this pattern in some of the biggest tech winners.

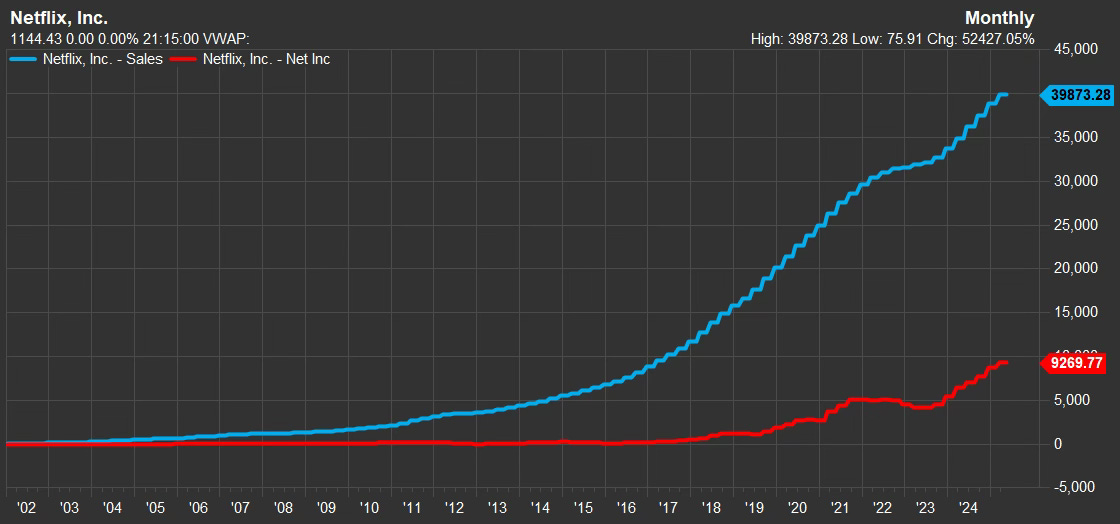

Look at Netflix. Same thing up until 2020.

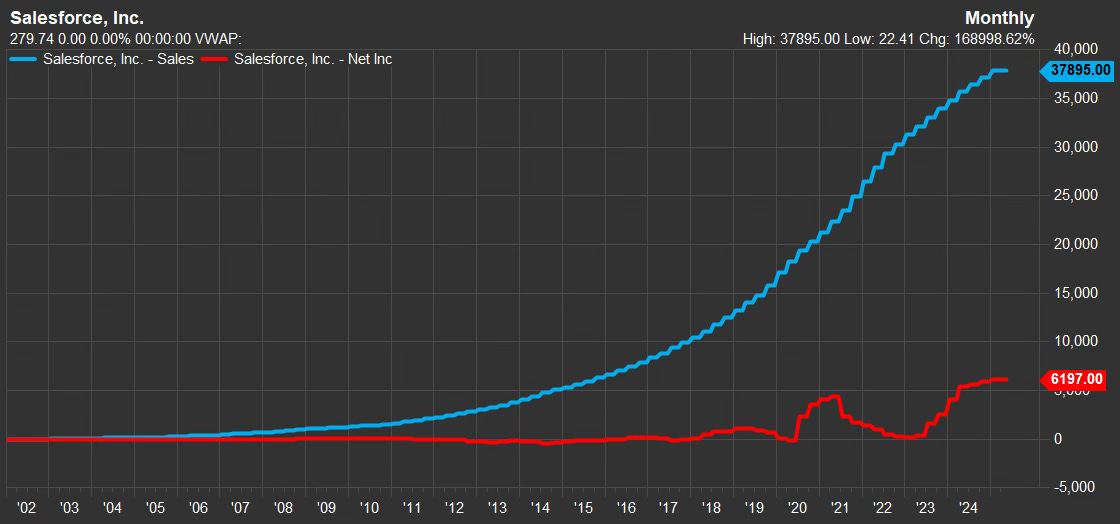

Salesforce

Why do these companies take on so many big growth projects? Because they need to spend the money.

Rethinking the Underperformance of Active Management

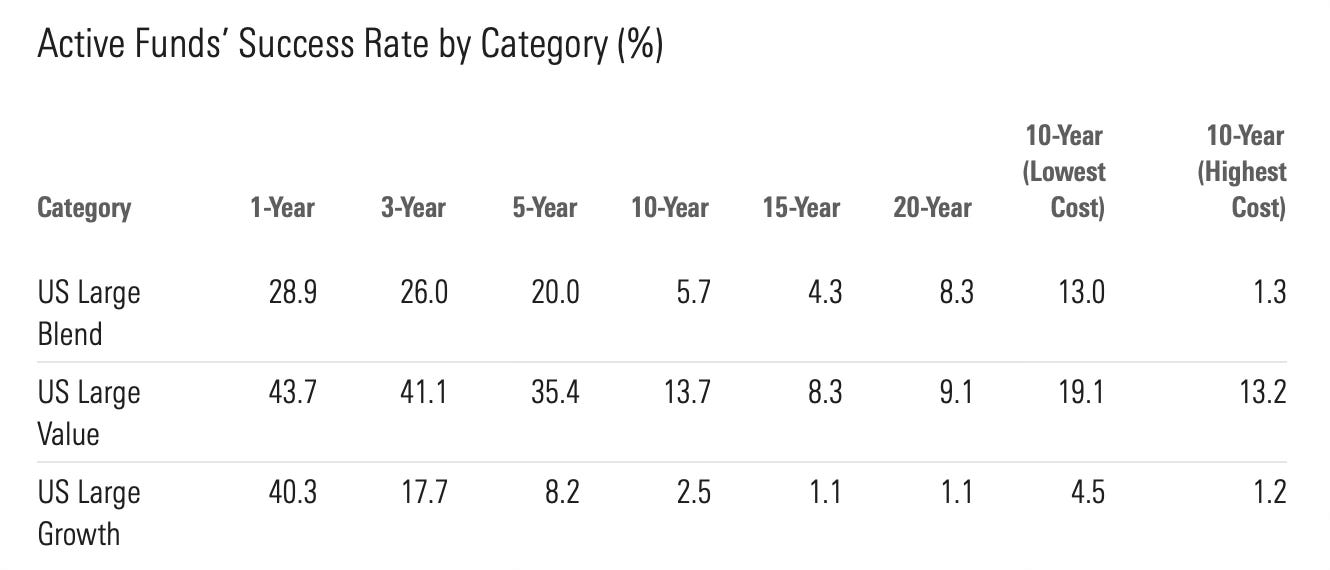

Over the last 10 years only 2.5% of US active managers investing in large cap growth have outperformed their benchmark.

2.5%!!! That is insanely bad. How can it be that bad? How is it actually possible?

I mean statistically 100 monkeys would do better than that. There has to be something systemically wrong with the active manager.

Do you want know why I think 97.5% of large cap managers underperform the index?

They will say it is the passive inflows, but that’s an excuse. The money is going into passive because the active managers are missing all the best stories in the market. Passive flows are a byproduct of the actual problem.

The problem with active managers is they are focused on earnings based metrics to pick investments. P/E’s and NPV.

They need to stop obsessing about earnings and creating tables for their investment committee meetings where they line up 10 companies in a row and show how they are investing in the one with the lowest P/E or the highest dividend yield.

The paradox of the last 20 years is what looked like the most ridiculously valued companies performed the best.

The fundamental analyst thinks companies are trying to maximise earnings (and NPV), but actually the smartest companies are doing the opposite.

But if you see what the growth companies are doing, the thing they can’t tell you or the US government they are doing, then you suddenly understand why it works.

Have a great weekend.

Erik

This is a banger

Thanks for this Erik - I love how often your articles challenge my preconceived notions.