YWR: The Baidu Setup

This is Not Investment Advice. Always speak to a professional.

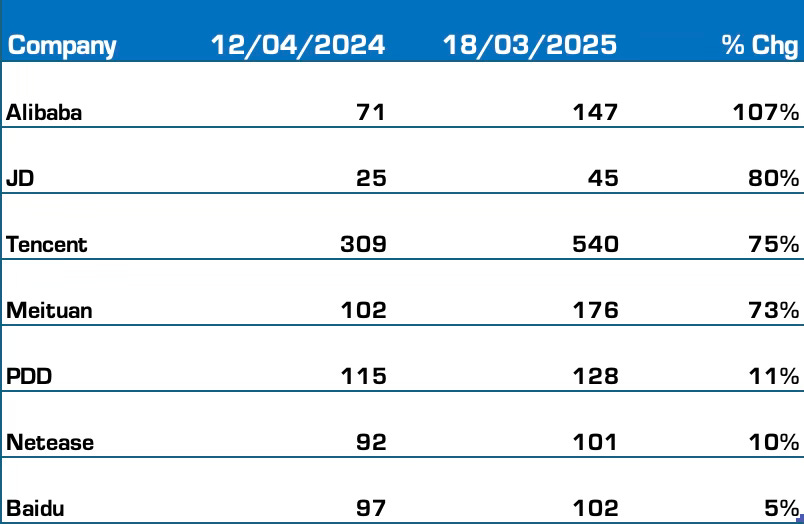

In April last year StirlingAI and I brought you Unleash Cash Dragons!

The crazy investment idea was to go all in on the hated Chinese tech stocks.

We pitched 7. Personally, I bought Alibaba, Tencent and Baidu.

Alibaba and Tencent have been great, but Baidu ‘The Google of China’ has been the worst (+5% and no dividend).

Baidu has been a total dog. And yet I’ve kept it because of the valuation and the work they are doing in AI and Autonomous Driving.

I kept thinking maybe Baidu Dog would one day have its day in the sun.

Well, at the risk of jumping the gun and getting positive too early, the sun might finally be starting to shine.

Baidu might even be reinventing internet search.

The shares look interesting here. Let me tell you why.

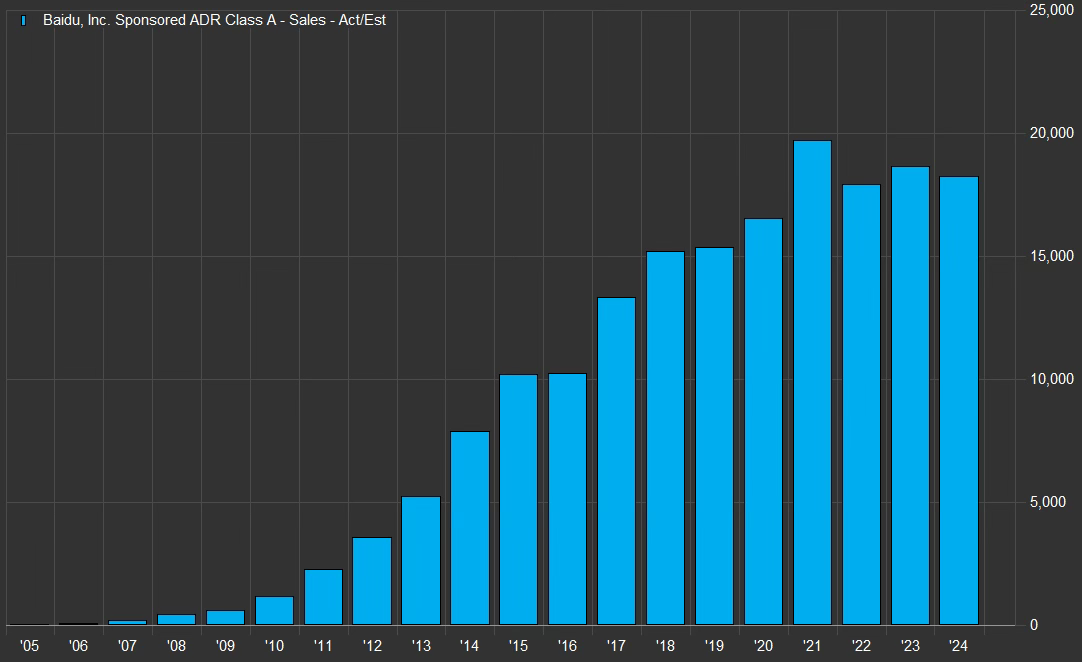

Baidu’s Growth Problem

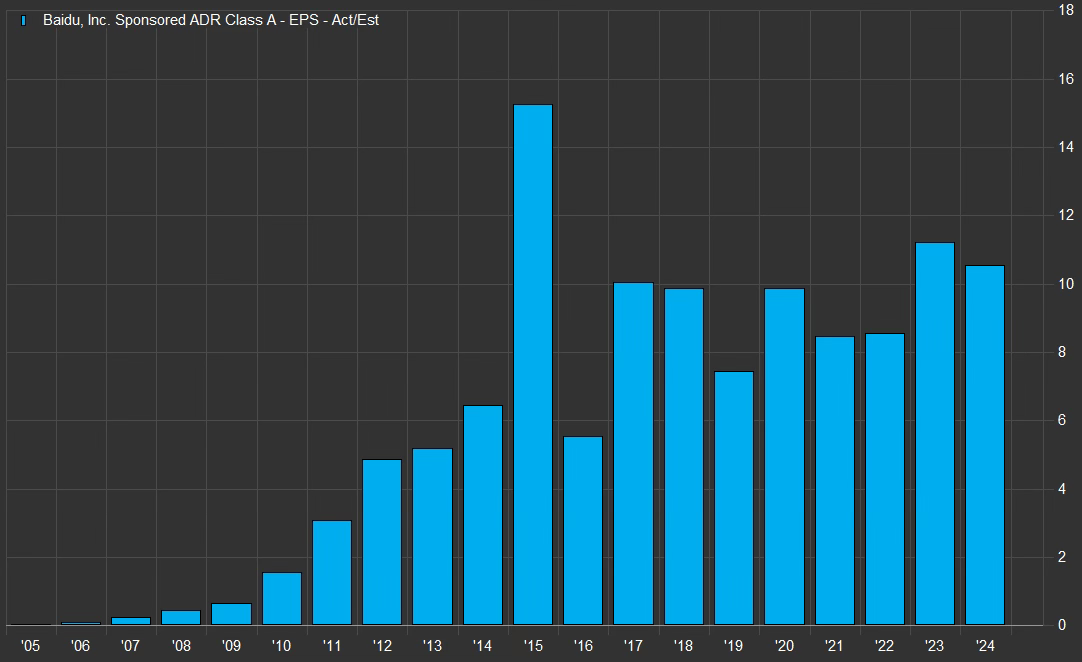

While sales have made some progress Baidu’s EPS has gone ex-growth.

EPS

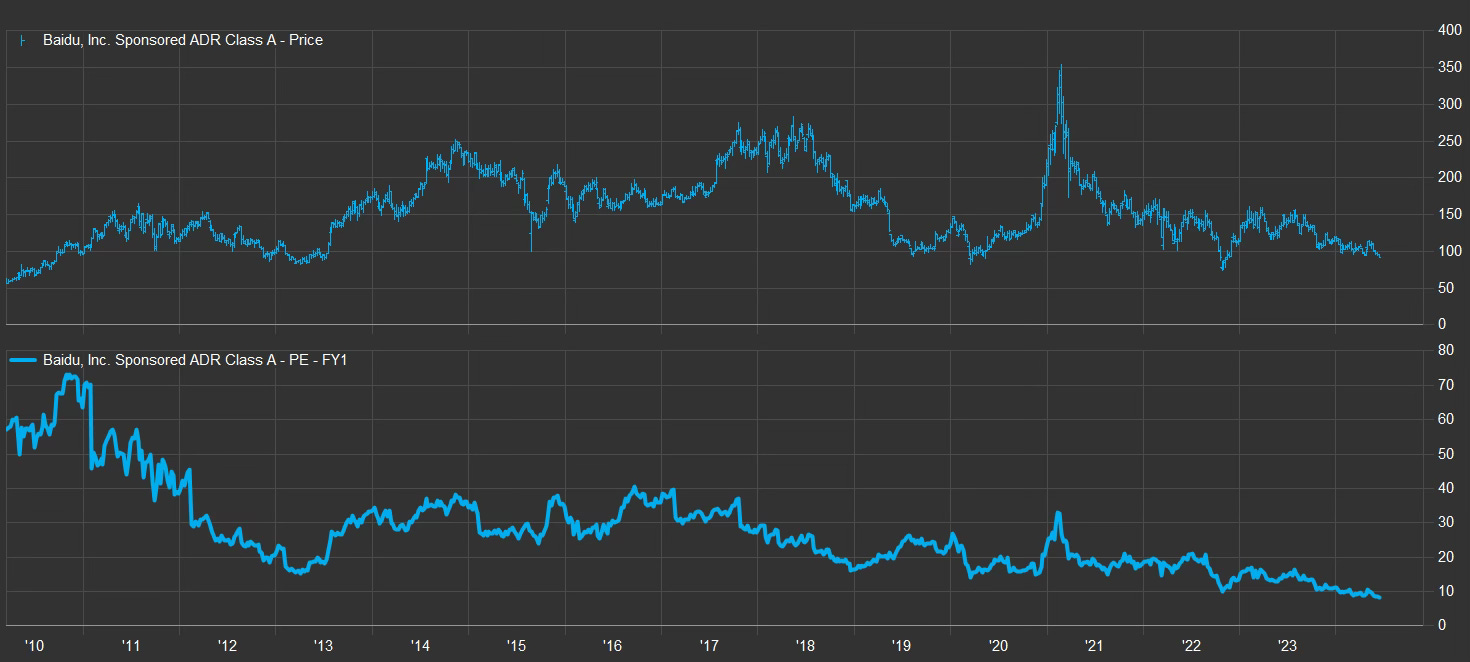

Share price and P/E Valuation

Baidu ADR’s peaked in 2017 at $250. Since then the shares are -60% to $100 with the P/E at 10x.

Growth might be a little slow, but Baidu’s valuation is extreme. The P/E is 10x and the company has $21bn in net cash, deposits and ST investments. That’s 60% of the market cap. And yes they are returning some of this capital.

In 2023 Feb 2023 Baidu announced a $5bn share buyback through 2025, of which only $1.7bn has been completed. That leaves $3.3bn, or 9% of the market cap to buy in the last 9 months of 2025.

Interesting. But still a ‘value trap’

So what’s the underlying growth problem?

The Self-Destruction of Paid Search

The problem is Baidu’s paid search business (online marketing services), or ‘The Google of China’ as they say. Baidu’s online marketing business has 3 problems.

The first, long standing problem is that consumers in China search for internet services using a variety of services. They use Baidu’s paid search, but also WeChat and internet influencers. WeChat’s mini-programs are especially strong. As a result Baidu doesn’t dominate internet advertising in China the way Google does in the rest of the world.

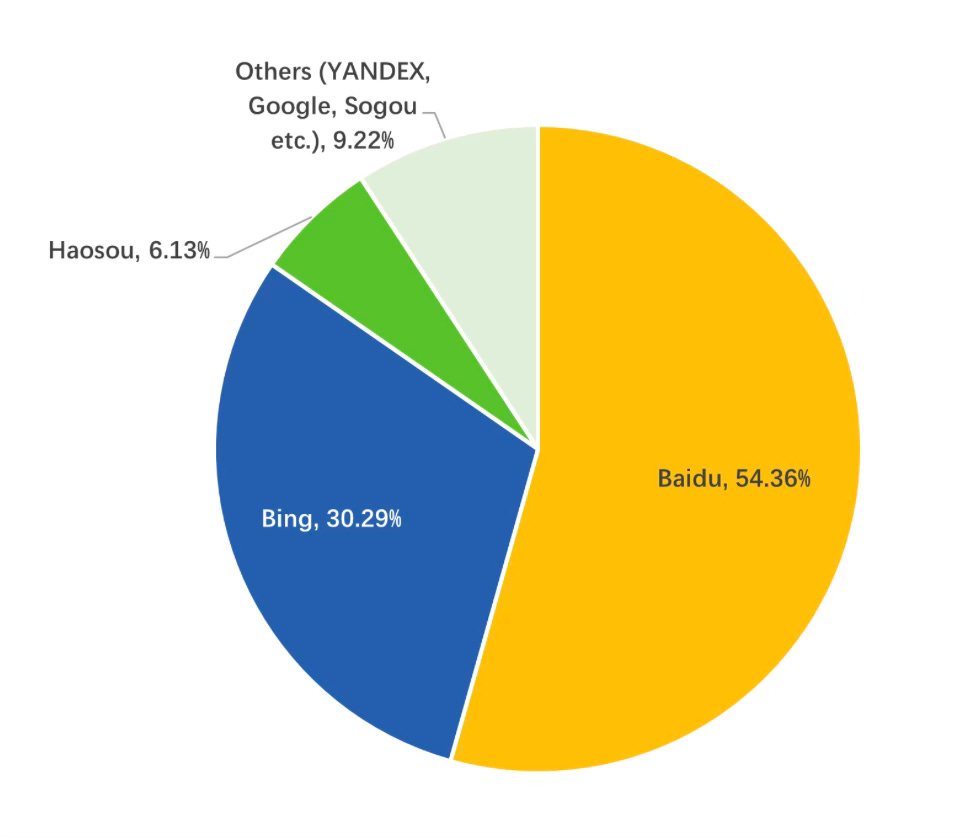

Second, Baidu has been losing market share to Bing, which now has 30% market share up from 5% in 2020.

The third problem, and it’s a heads up for Google, is the use of AI driven results in paid search. In Q4 22% of Baidu’s search results were AI generated. This is up from 18% in Q3. These AI search results are a turn off to advertisers. Why pay for clicks if the clicker is an AI and the end customer never sees your ad or page?

Users like the AI driven results, but the more you use them, the more it turns away advertisers. But Baidu keeps trying to grow AI driven results anyways. It’s like Baidu is imploding itself.

Or maybe ‘disrupting’ itself is a better word.

What’s the bull case?

This all sounds terrible.

A value trap with an ex-growth business losing market share to Microsoft.

What’s the bull case and how are they reinventing paid search?

How do we make money?

I see three growth drivers unfolding and upside to $150 ($BIDU).