YWR: USA All The Time (USAATT)

I’m going to say something terrible.

I hope the market gods don’t kill me for this……

…but in the future will International Markets matter anymore?

Or matter much.

I mean long-term.

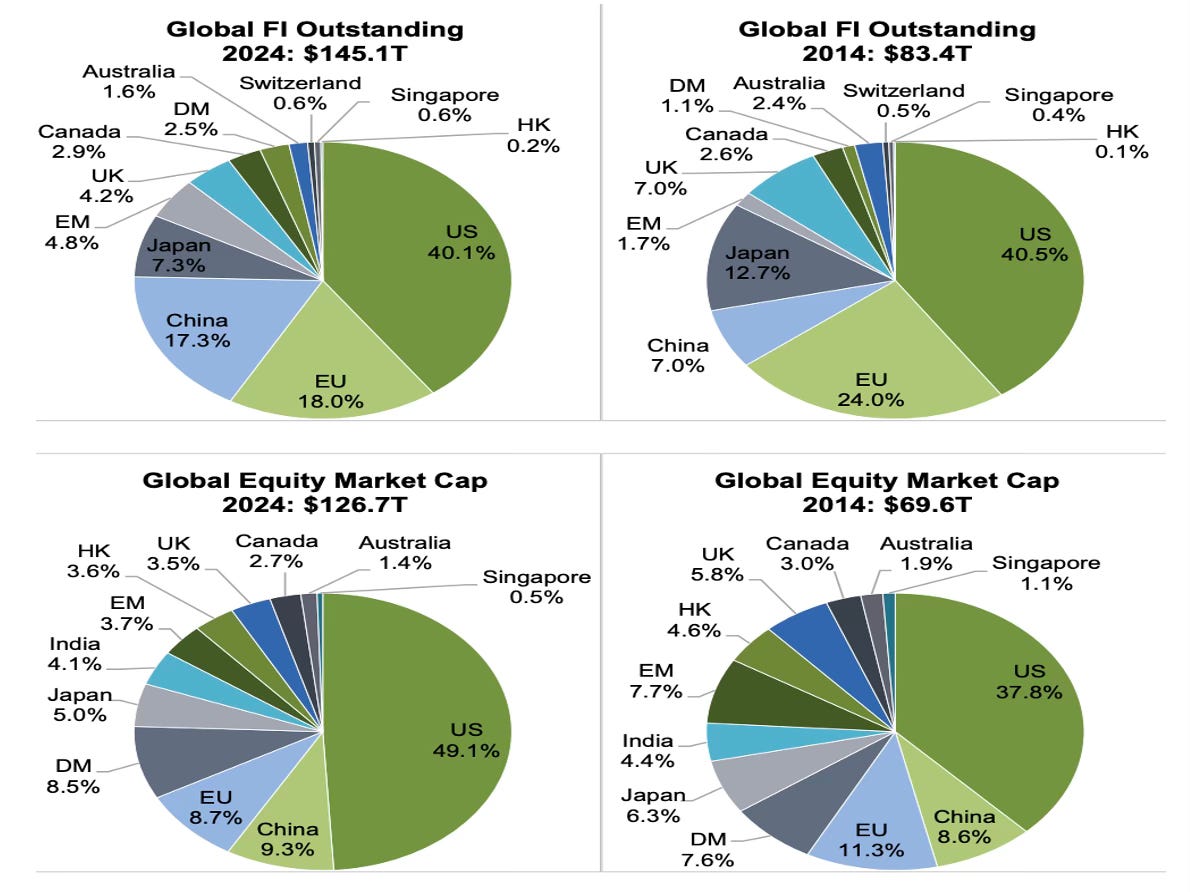

This chart from 3 Non-AI Trillion $ Trends is stuck in my head.

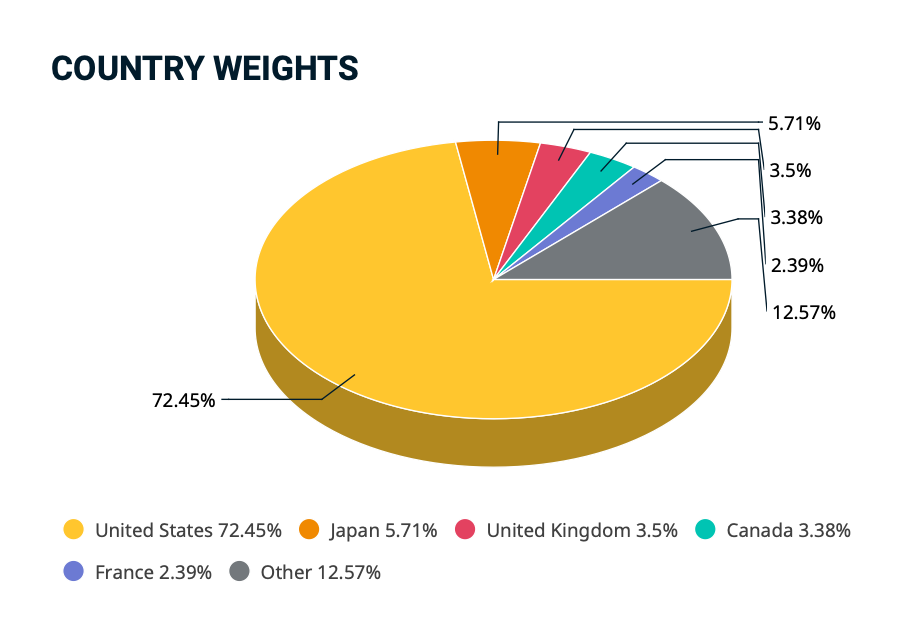

In 2014 it used to be the US was a big stock market (38%), but there were lots of other important markets too. Now the US is 49% of global market cap and all the other markets are a lot smaller.

The UK for example, has gone from a respectable 5.8% to just 3.5%.

And that was 2024. With semis going vertical and the IPO of Spacex the US in 2026 must be closer to 55% of global market capitalisation. After OpenAI and Anthropic IPO will it be 60%?

Capital markets have network effects. Liquidity begets liquidity. And network effect businesses are usually winner takes all.

In the years ahead will international markets become irrelevant to global allocators?

Or, will investing ‘internationally’ mean buying an ADR on a US exchange?

The US Capital Markets Ecosystem

The US supports its capital markets in a way you don’t see anywhere else. Markets are a religion. This relentless attention to the health of the US markets is why they keep growing, innovating and taking market share. It’s a US soft power.

There is also a whole ecosystem to support US capital markets.

Take the lifecycle of a start-up.

The US has the biggest PE/VC industry. These PE/VC firms back the start-ups which later go on to IPO or issue debt. If you are an aspirational start-up founder it’s best to be a Delaware corporation located in the US to get funded.

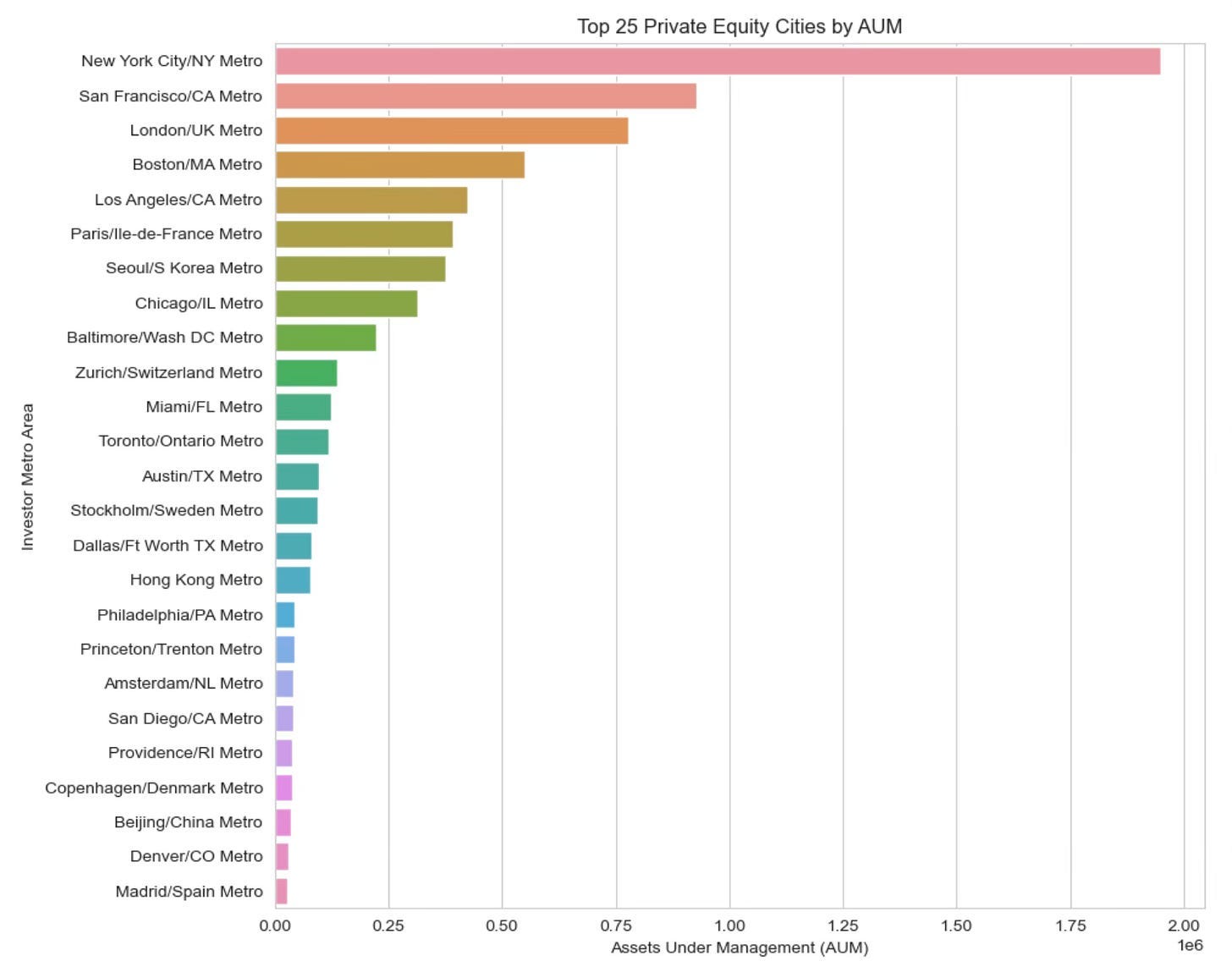

NY City by itself has almost $2 trillion in private assets under management (PE/VC Q3 2025 Deal Tracker). NYC, SF, Boston, and LA are big cities for the PE industry. 6 of the top 10 cities in the world are in the US.

US Start-up → US Venture Capital → US IPO

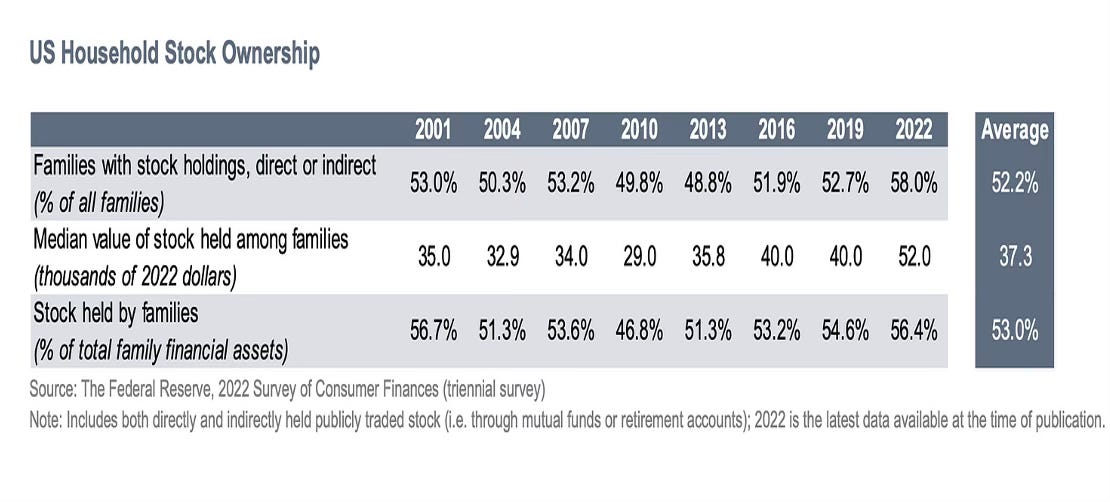

The US also has the world’s biggest army of retail investors. 58% of US households invest in stocks with an average holding of $52,000 (and that was on the market lows in 2022).

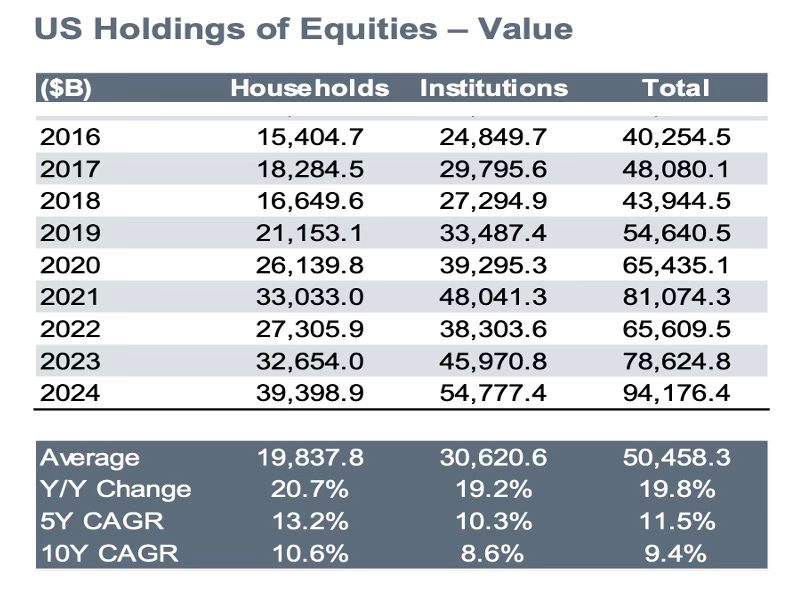

The US investing pool is the world’s biggest with $94 trillion in equity AUM between individual investors and investment funds.

The other advantage to the US market is that it’s one currency, one reporting standard, one ticker format, with low trading costs. There is also the best offering of derivatives products if you want to lever things up, change the payoff structure or isolate different parts of the trade. This is why US securities work well for complex quantitative trading strategies. When you take these quant strategies to other markets there are lots of edge cases and exceptions to troubleshoot.

In the end it’s easiest to just trade the US.

Liquidity begets liquidity.

The Americanisation of TotalEnergies

TotalEnergies is a great case study. I’ve been a long-time shareholder and have followed their multi-year pivot to become more of an American company. Total has always had a lot of US shareholders of their NYSE listed ADR, and it annoyed CEO Patrick Pouyanne that despite similar growth metrics Total still traded at discount to Exxon and Chevron because it was European.

So Total started making small changes like doing their annual capital markets days in English in New York. They also increased their US operations in Texas to make the business more American.

Here’s Pouyanne deciding Texas would be their new second home.

“I love Texas. Texas is a country. We want to invest in the U.S. But the U.S. is so big. It’s so huge that, in fact, we are completely lost, you know? And in fact, you know, for us, you know, we invest in the U.S. in LNG and in electricity. And in fact, the perfect land is Texas, where we are building a new plant, Rio Grande LNG, where we are developing gas plants and renewables. And there is a lot of space. So, yes, it’s a big country. It’s a growing demand of electricity. So it’s a nice place.”

“You know, we were heavily involved in Russia. And I decided to take actions. And we choose American, as I would say. I said, OK, look, my colleagues, forget Russia, because this war is just has some—many implication. We need to continue. We are one of the top three energy player. If we want to continue to be among the top three, it will not come—it will not come from Russia. Let’s go to the U.S.” Source: CFR

There’s the killer line.

If we want to be top 3 we need to be in the US.

Then in 2025 Total converted their ADR share to a full US listing to be the same as Exxon and Chevron.

Total feels the pull of the US. They feel the need to operate in the US, have offices in Houston, be listed on the NYSE, and have access to US capital..

European banks are the same. They all want to have access to US retail funding. It’s why Barclays keeps building its US consumer bank and why Santander just sold a bank in Poland to buy Webster Bank for $12 billion. And any European investment banking operation has to be in the US (50% of the global fee pool). And you see it with the Japanese banks all highlighting how they are getting more active in US capital markets and trying to be like JP Morgan or Goldman Sachs.

It’s the same for global tech companies. How can you not be in Silicon Valley? And what kind of a tech company are you if you aren’t listed on the NASDAQ?

And the same with Biotech. You have to be in Boston, SF or San Diego.

Across industries international companies see the trend. If you are listed in the US, operating in the US, and known to US investors you have structurally better access to capital.

It’s reflexive. Traders want to be able to trade any security in US$’s on a US exchange. This exerts gravitational pull on the top international companies to also be listed and operating in the US. This further reinforces the two-sided attractiveness of US capital markets. It has both the investors and the issuers. And as an international company if you aren’t there you’re missing out.

Which is why you see the markets like the LSE consistently losing issuers who move to the US.

The Death of the LSE

If our theory is correct it will be hard for the LSE to stage a comeback. The risk is UK public companies remain a hunting ground for US PE firms to acquire quality businesses on the cheap. Getting taken out is a nice one time benefit for shareholders, but the other public UK companies don’t feel like being in a death spiral where their future is to be taken out by private equity. They feel pressured to move to the US before it is too late.

Bright new start-ups out of Cambridge or Oxford might operate in London, but end up listing in the US.

Everything trades in the US.

In 2040 will US listed stocks be 75% of global market cap?

And what are the market structure implications of this?

It’s not so hard to imagine. In the MSCI World index it’s already 72%.

If US markets are >70% of listed market cap does a US investor really care about the 3.5% of stocks in the UK or 2.4% in France?

And will the top UK and French companies just relist on US markets to remain competitive? Like Total?

There is also the subtle effect of the portfolio manager saying “Do I really need to do a research trip to the Netherlands? I’ll just see ASML at the Goldman semiconductor conference in NYC.” So he never makes the trip and never sees the 3 smaller Dutch companies that would have filled out his day in Amsterdam.

In December last year I met a large US pension fund which doesn’t even look at international markets. I thought it was a bit limiting at the time, but I’m starting to wonder if maybe they are right and this could be a trend.

Norges has come to the same conclusion. Here’s Paul Marcussen based in New York saying how Norges wants to be structurally overweight the US forever.

“We don’t give official market outlooks. But if I want to bet on the US versus Europe over the next 20 years, my money would be in the US. It has the innovation, it has the creativity, it has the willingness to let people fail and pick themselves up and try again, which we don’t have in Europe.” Source: top1000funds

It doesn’t mean international markets can’t work for a few years, but it says guys running hundreds of billions of dollars have made a top down decision they are allocating most of their billions to US markets. And if you aren’t in that bucket, it’s hard to attract their money.

What is the long-term effect of this?

Structural US Premium

This could mean a steady gravitational pull of fund flows towards the US and away from international and EM markets. The US becomes the platform where everything gets traded. US and International.

It means international markets would still have good years, but the bull markets would become shorter and fewer.

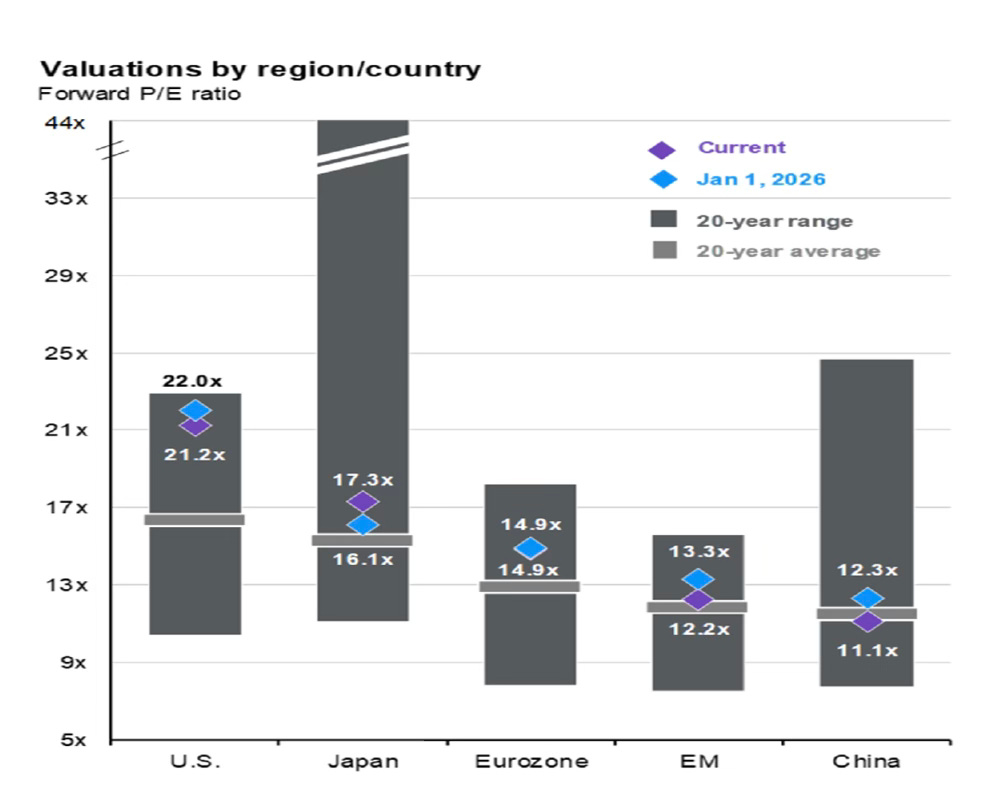

You would also expect to see a widening valuation spread between US and international markets. A persistent premium for US securities reflecting the better liquidity and market structure.

Isn’t this what we are seeing already?

Look at the global valuation chart below from JP Morgan. I used to look at this chart and think it showed how international market valuations are attractive. What a deal?

But that view might miss the structural changes underway. The surprise for investors might be that the valuation difference is not mean reverting.

Through the lens of our ‘USA all the Time’ not being listed in the US is like not being on Facebook. It makes perfect sense that US valuations are near the top of their 20 year range. And it makes sense that international stocks are near the bottom of their 20 year ranges even though we are in a global bull market. The valuation difference might even get wider in the years ahead. Extrapolating things into the future; in 2040 does the US trade at 27x while Europe trades at 12x?

How do we make money?