YWR: Killer Autos

Disclosure: These are personal market views and commentary only, not investment recommendations. For investment advice seek professional help.

Everyone needs to do more work on the enormous upside in car companies and auto parts makers. Like multi-x upside.

In the YWR Global Factor Model we know Banks are the leading sector. They’re historically cheap, beating estimates and the stocks are trending up. We’ve gone over repeatedly why this is happening, why it will continue, and why it is not 2008 again for banks.

Interview with CEO of Unicredit

The Upside Everyone is Missing in European Banks

How I learned to love European Banks.

But we need to do more work on autos, because they’re also screening well.

stocks prices are trending up,

earnings estimates are rising,

valuations are attractive,

nobody wants to own them.

What’s going on?

Why are estimates trending up and can it continue?

Is there something the market is missing?

Are you ‘consensus’?

The consensus view is autos are highly cyclical, and we are going to have a recession and ‘everyone knows’ you shouldn’t own a car company in a recession.

But the truth could be the complete opposite.

Steven Schlegel has written an excellent report on why autos are the most exciting sector in the market and the parts companies in particular will have multi-x upside. He is so excited he created a special purpose fund to play the theme where he has really analysed which companies are going to go up the most (parts companies).

Steve’s report is the best write-up I’ve seen.

In the Dirty Div’s portfolio we own Mercedes, but Steve makes me wonder if we need to buy more, or add another stock (maybe BWW or Porsche Holding). Steve would say get a parts company.

Below are some key charts from Steve’s report.

Global auto production has been in a 4 year downturn.

The SPR of Autos

Which has led to dangerously low auto inventories in the US. We talk about low oil inventories, but not the low car inventories. Inventory is less than 200,000 units, when often they are over a million units.

Lack of production and no inventory created an almost 50% surge in new car prices.

The lack of car production (and sales) since 2019 means the average age of cars in the US is increasing. Cars are generally lasting longer over time, but even so, we’ve had a surge in the age of the car fleet in the US. It hasn’t been this high since the 1940’s.

The 5 year auto boom!

Steve’s work on previous surges in the age of the car fleet suggest we could have a 30% increase in US car sales over the next 5-7 years from 15 million units/year to over 20 million.

The China Auto Boom: Act 2

Steve’s work also suggests even though China’s auto market is the biggest in the world, it still have much more to grow to catch up to other developed market peers.

China is a 25 million unit market, but Steve’s analysis (below) suggests it could grow to 40 million. Great for VW, MBG and BWM.

If US auto sales go from 15 million to 20 million and China goes from 25 to 40 we are going to have a multi-year auto bonanza.

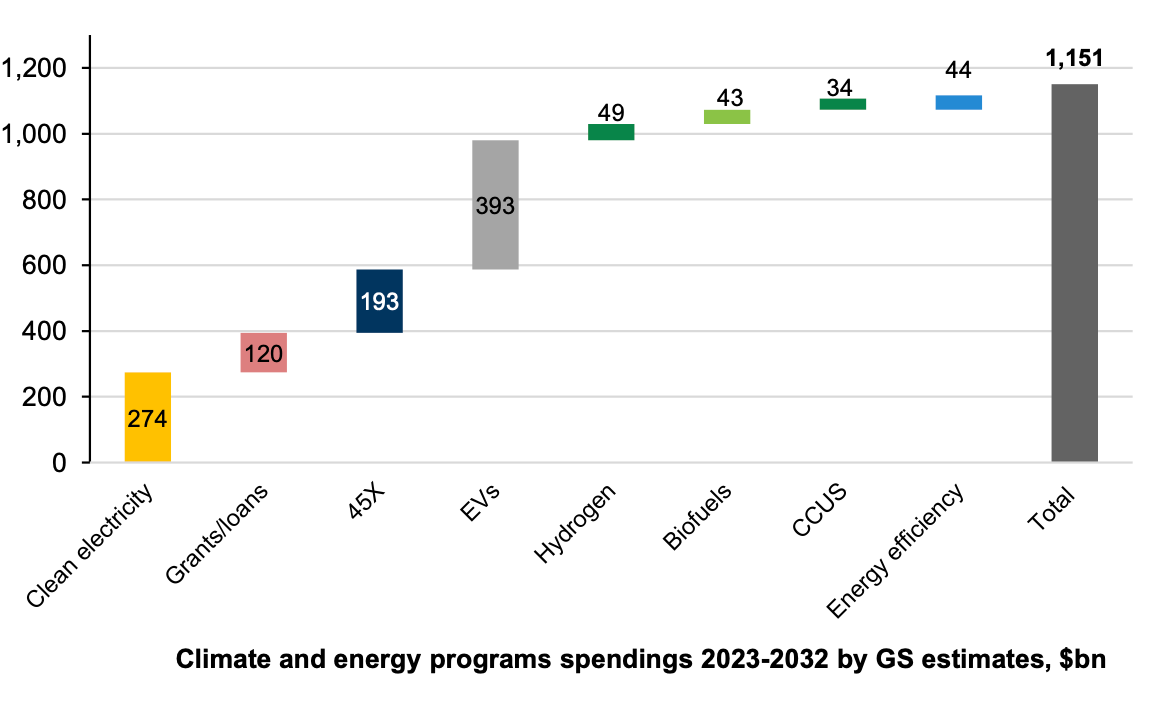

The cherry on top is that as part of Net Zero the government will pay you to buy a car. Goldman estimates the US will spend $395 billion on EV subsidies.

Auto bull case stack:

Super cheap stocks (5x P/E, 7% yield) that nobody likes or wants to own even though they are global luxury brands (MBG, BMW, PAH3, VOW),

Lowest auto inventories ever,

Oldest car fleet ever,

Global auto sales could grow +50% over 7 years (US, China plus a little India),

US government will pay you to buy an EV.

The link below is to Steve’s full 17 page write up on the sector. He thinks Magna has 165% upside and it’s his least favourite idea. That’s why he thinks this needs a fund.