YWR: The University Endowment Train Smash

I could see the makings of a train smash, but didn’t have time to do more work on it until last weekend.

Earlier this month I was going through the major college endowment investment reports for YWR’s MegaFund Positioning Review and I noticed something surprising.

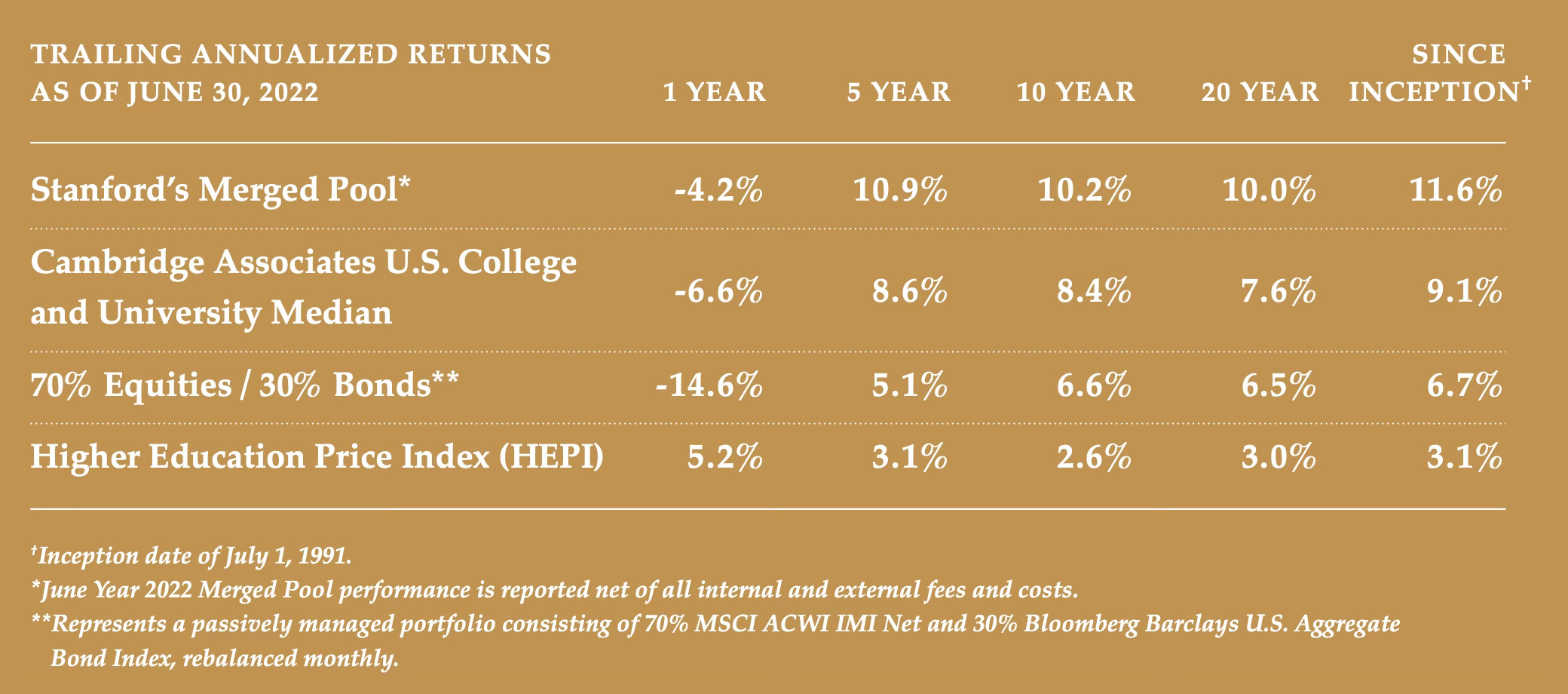

The top endowments have been doing extremely well; averaging performance of 9-10% p.a. Like clockwork.

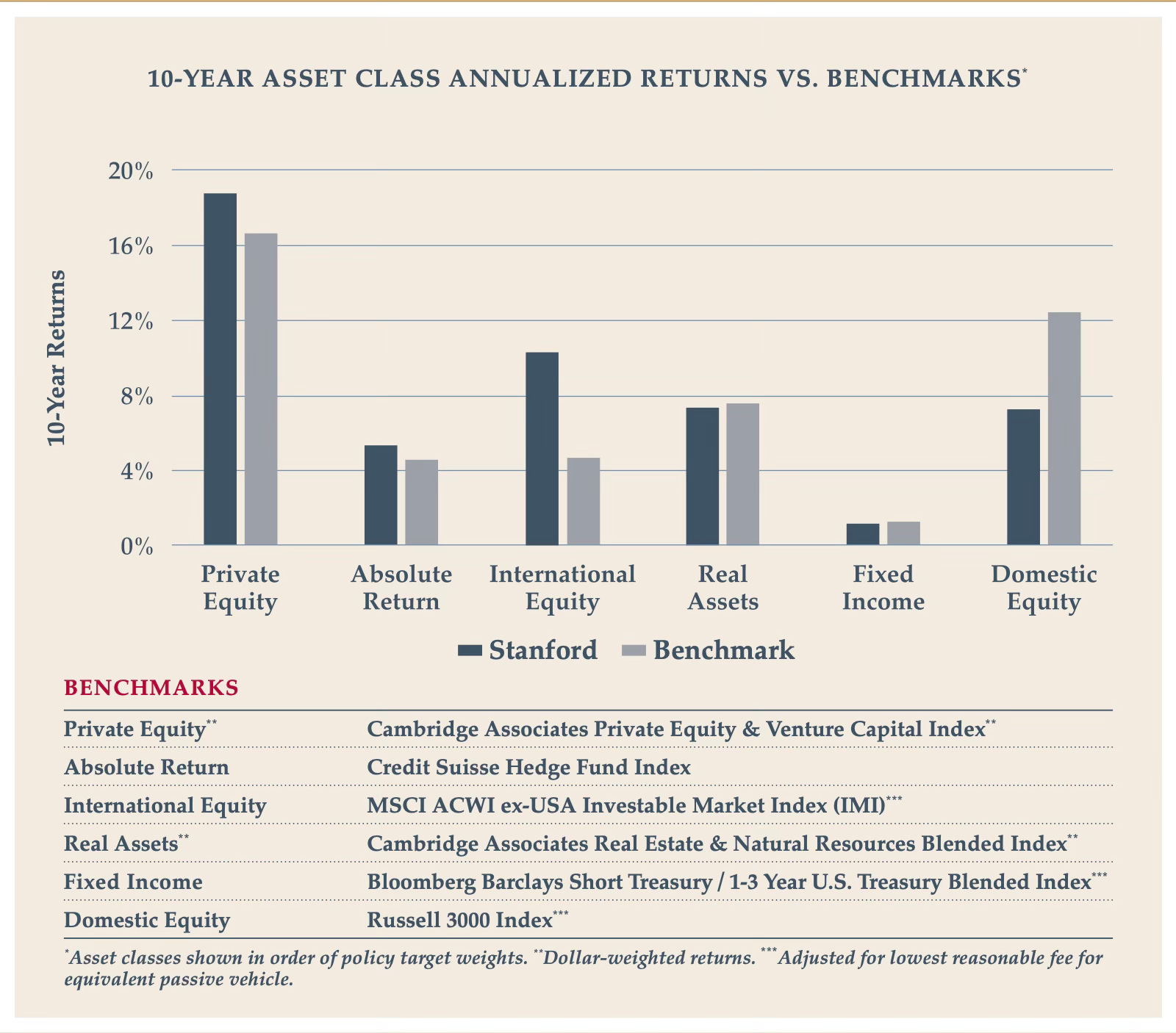

And the driver of these returns has been private equity and venture capital, which have been returning 16-18%/year over 10 years!

Of course returns like these suck everyone in, and the endowment allocation to private equity has been steadily growing over time.

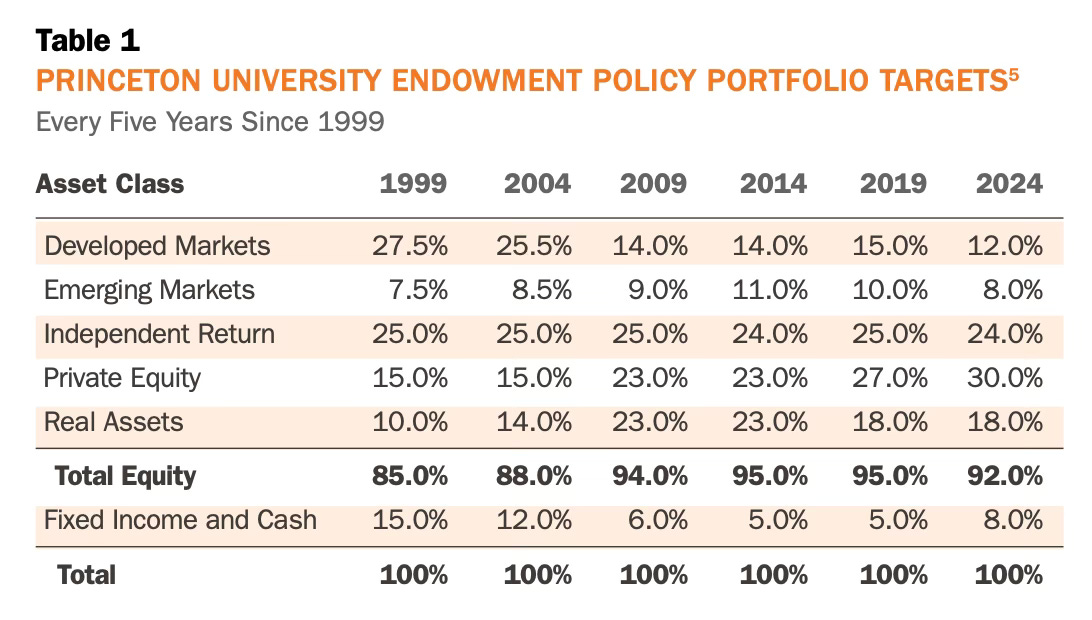

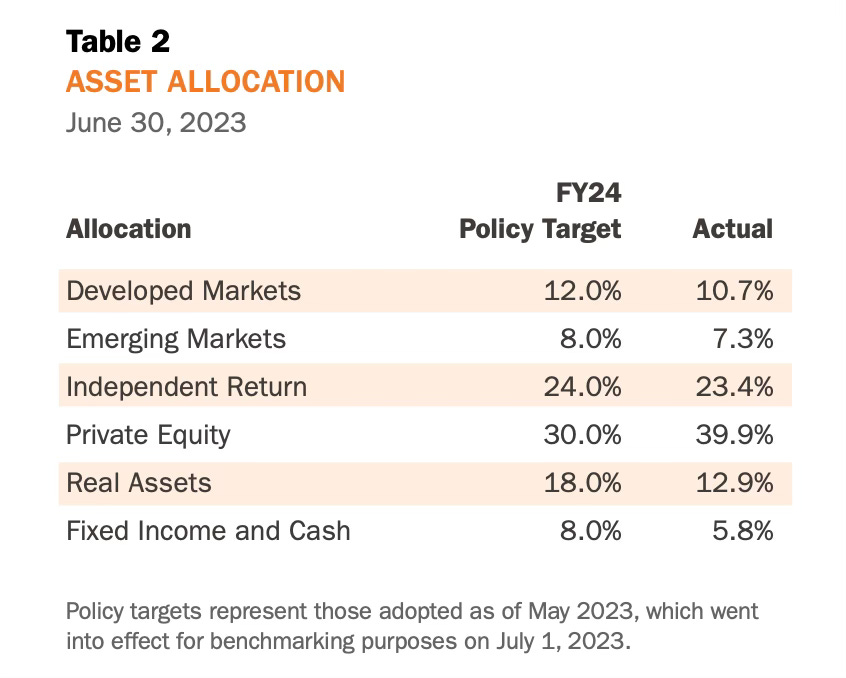

Princeton has the best chart on this. In 1999 they had 15% in Private Equity. By 2024 it was 30%.

But it wasn’t really 30%. Actually, it was 40%.

30% was just the target.

Princeton was the most explicit about how the PE bucket had outgrown it’s target allocation, but mentions to this affect were in several fund commentaries. The usual accompanying statement was that the fund would try to manage this exposure down to the target allocation over time, but this would depend on private equity realisations and prior fund commitments which had not yet been exercised.

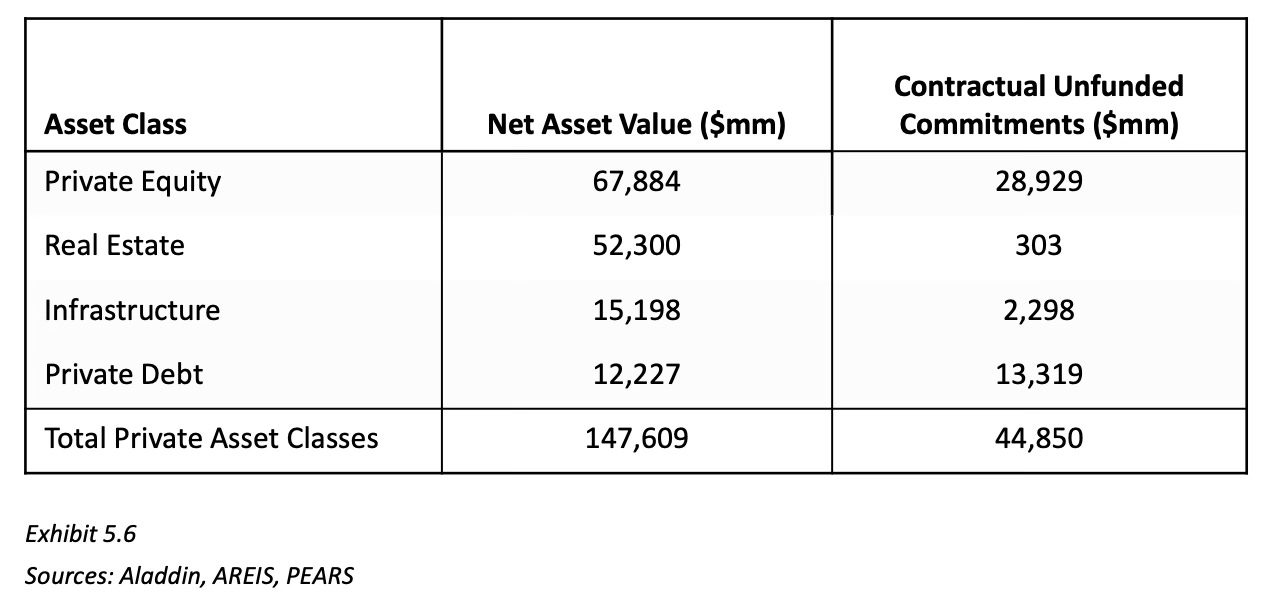

The size of these unfunded commitments can be surprisingly large and we just get glimpses of it from the public pension funds, which have better disclosure.

Alaska Permanent Fund for example, has a PE portfolio of $15.4bn with $4.2bn in future commitments.

CALPERS has a $67bn PE portfolio with $29bn in unfunded commitments.

Now let’s get to what surprised me.

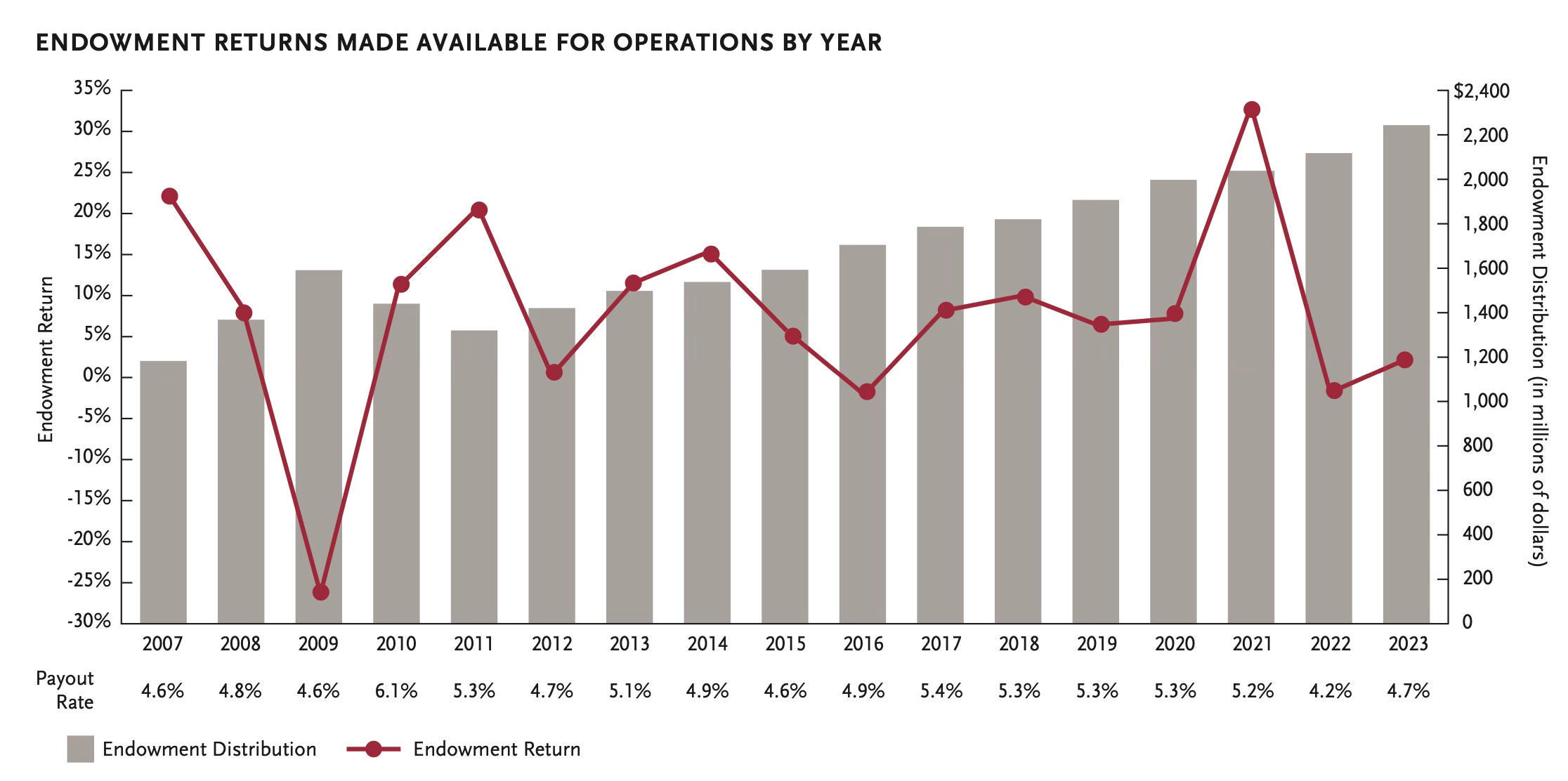

Each year these university endowments make a contribution to the operating budget of their university.

This contribution is been between 4-5% of the endowment AUM every year, and has been steady over the last 15 years.

Harvard had the best chart on this, but the others had similar numbers (3-5% every year).

Look at the small number at the bottom labeled ‘payout rate’. That’s how much of the Harvard endowment is paid out to the university each year. Call it 5% on average.

What surprised me was the endowment payout has had no benefits of scale. I would have thought with 10% p.a performance that as a % of the fund this payout would have dropped to maybe 2-3% of AUM by now. But no.

A helpful YWR reader alerted me to the fact private endowments are required to payout 5% of AUM each year. This is the 5% payout rule.

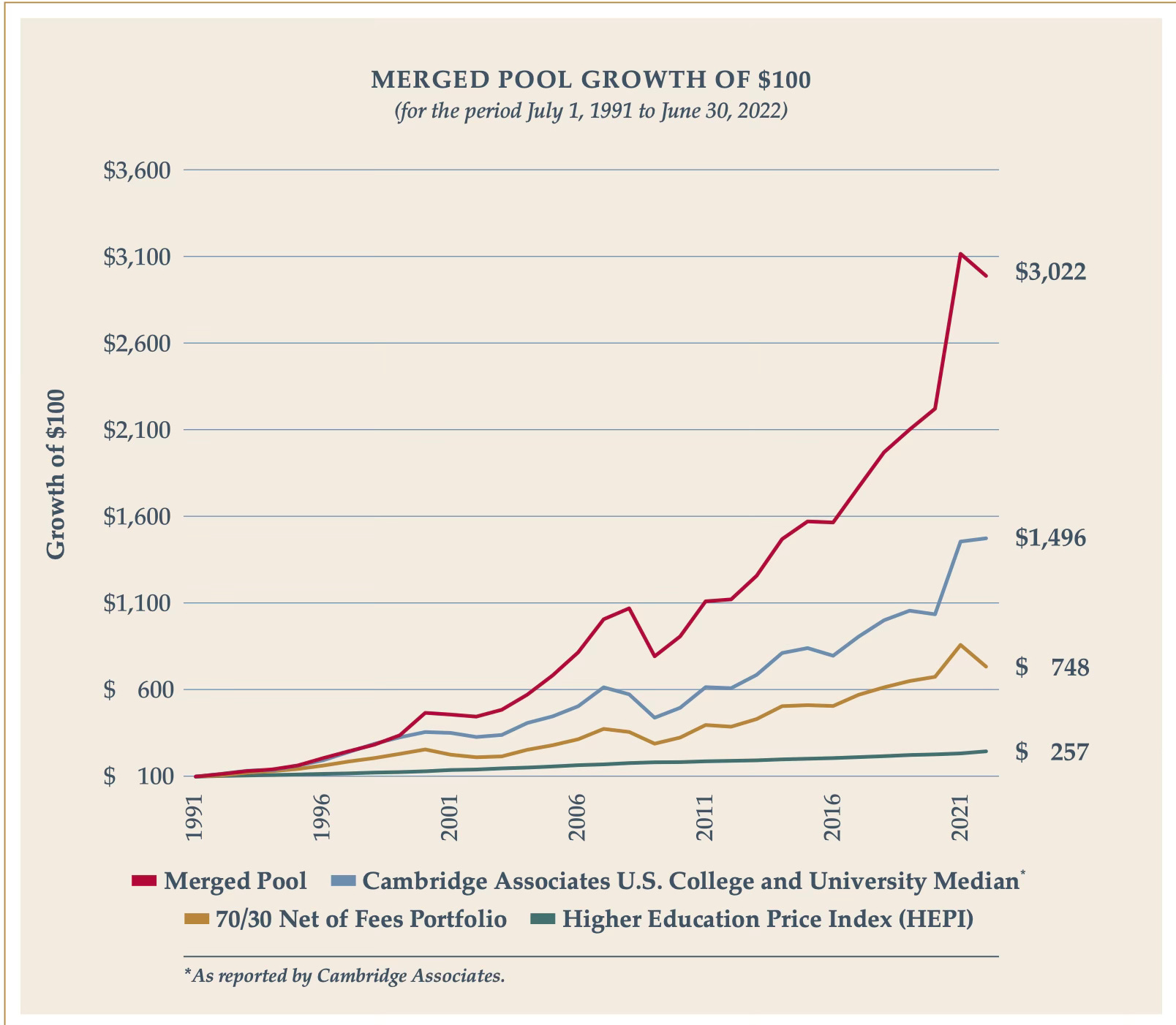

When you look at the nominal growth of the endowment (actual change in AUM) you see it is growing at 7-8% over time, not 10%. 10% is the headline performance number. 7-8% is the net number after the drag of paying out to the university each year.

In 2019 the Stanford endowment was 27.7bn. By 2023 it was 36.5bn or a CAGR of 7.8%. In 2013 the Harvard Endowment was $30bn. In 2023 it was $50bn. That’s a CAGR of 5.2%.

Putting it together, the payouts to the university are growing at 4-5% per year and the endowment AUM is growing at 7-8%.

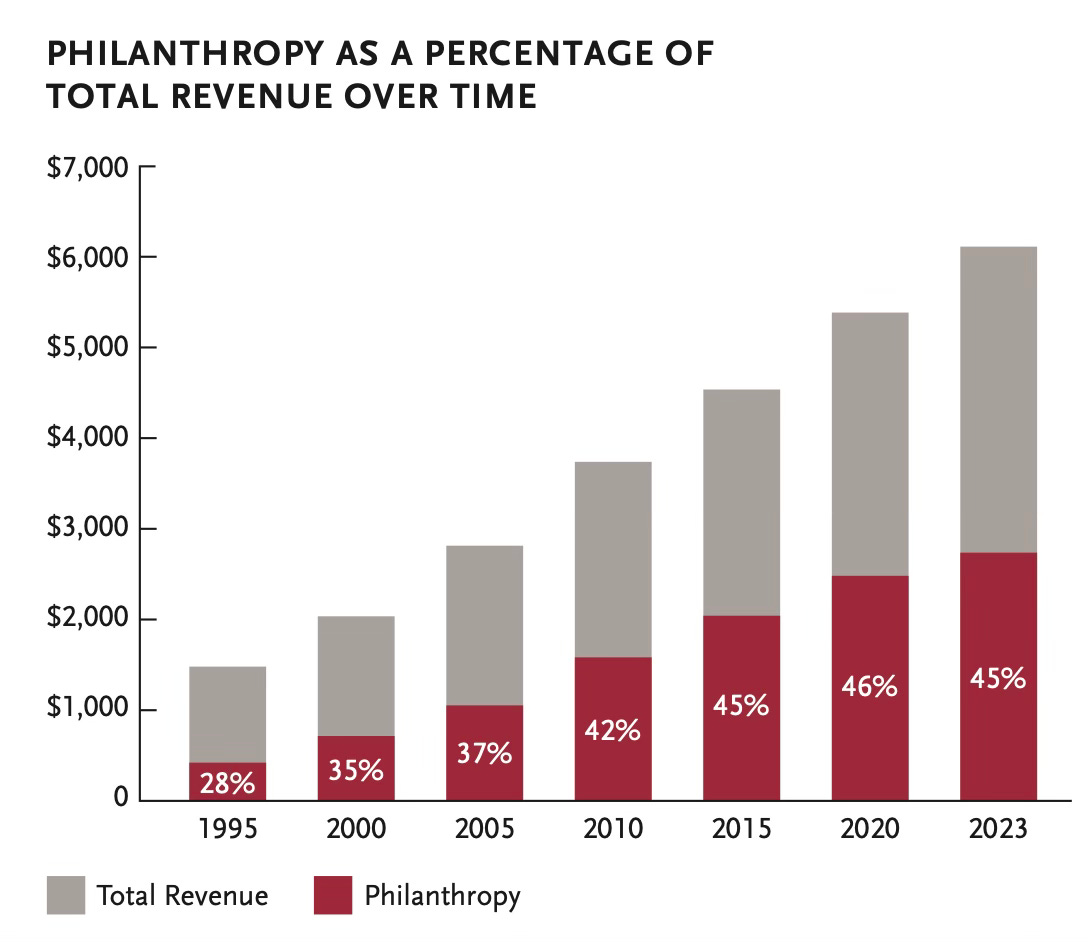

In the financial reports you also find the universities are highly dependent on these payments from the endowment. Endowment contributions are roughly 25-37% of university revenues. This high level of endowment support is why the Ivy League universities can say their admissions are ‘need blind’.

In the chart below the ‘philanthropy’ contribution to Harvard’s annual operating budget is the endowment contribution ($2.2bn in 2023 or 37% of operating revenues) and alumni gifts ($486mn or 8% of revenues). ‘Philanthropy’ is almost all from the endowment.

The endowment is funding 37% of university revenues and that number has grown in both absolute terms as well as a % of revenue contribution.

Put another way, the university is milking the positive PE/VC returns from the endowment.

Ingredient #1. Universities highly allocated to high risk, illiquid asset classes. PE + VC + Real Estate + Infrastructure are 30-50% of the endowment.

Ingredient #2. The universities have grown their expenses in line with the returns of the endowment.

Now let’s look at the setup from a meta level.

Everyone has grown their Private Equity allocation and is over allocated relative to their policy target.

The endowments want to manage their PE/VC exposure down, but they have also made significant prior fund commitments. Where does the money for this come from?

So the endowment is under pressure to see some private equity realisations in their portfolio so they can:

A. pay for their operating budget requirements,

B. offset the additional commitments they promised to invest in the past.

Net, net, everyone needs liquidity and wants out. Which is why PE/VC fund raising is falling.

Ingredient #3: Hard to find new bag holders

If the major funds over allocated and want out, what does that do to future returns?

The easiest way to exit a PE investment is to sell it to another PE fund flush with a new collection of greater fools. But how do you exit your investment if there is less money coming into the system, or even worse, it’s an outflow?

And what happens if PE returns have already benefited from 15 years of multiple expansion?

Ingredient #4: Valuations are high.

What if the virtuous PE/VC cycle of new money coming into the asset class which leads to rising valuations and liquidity is about to go in reverse?

Could PE investments lose money? Can that even happen?

As I see this playing out the major endowments will put pressure on the PE firms (KKR, Carlyle etc) to do deals and generate some realisations. The liquidity needs mean they will pressure the PE firms to do deals, even if the prices aren’t great. They will also try to negotiate themselves out of their fund commitments.

And could this pressurised selling lead to a decline in valuation multiples? Kind of like what has happened to value stocks over the last 10 years as money went into index ETF’s?

If PE multiples start to soften, then the returns also look bad. This means less new money coming into the space, further exacerbating the liquidity problem. The virtuous cycle turns vicious.

For the endowments there is also the problem of paying the exorbitantly high annual contributions the Ivy League university has gotten used to. These numbers are built into their budget. They can’t go in reverse.

So now the endowment has to sell whatever it can, which is cash, bonds and public equities.

Over time, if this situation persists, the endowment finds that as it keeps selling bonds and stocks to pay the university, it has a greater % of the remaining fund allocated to illiquid PE investments it can’t get out of.

This is the train smash. And it happens gradually over time.

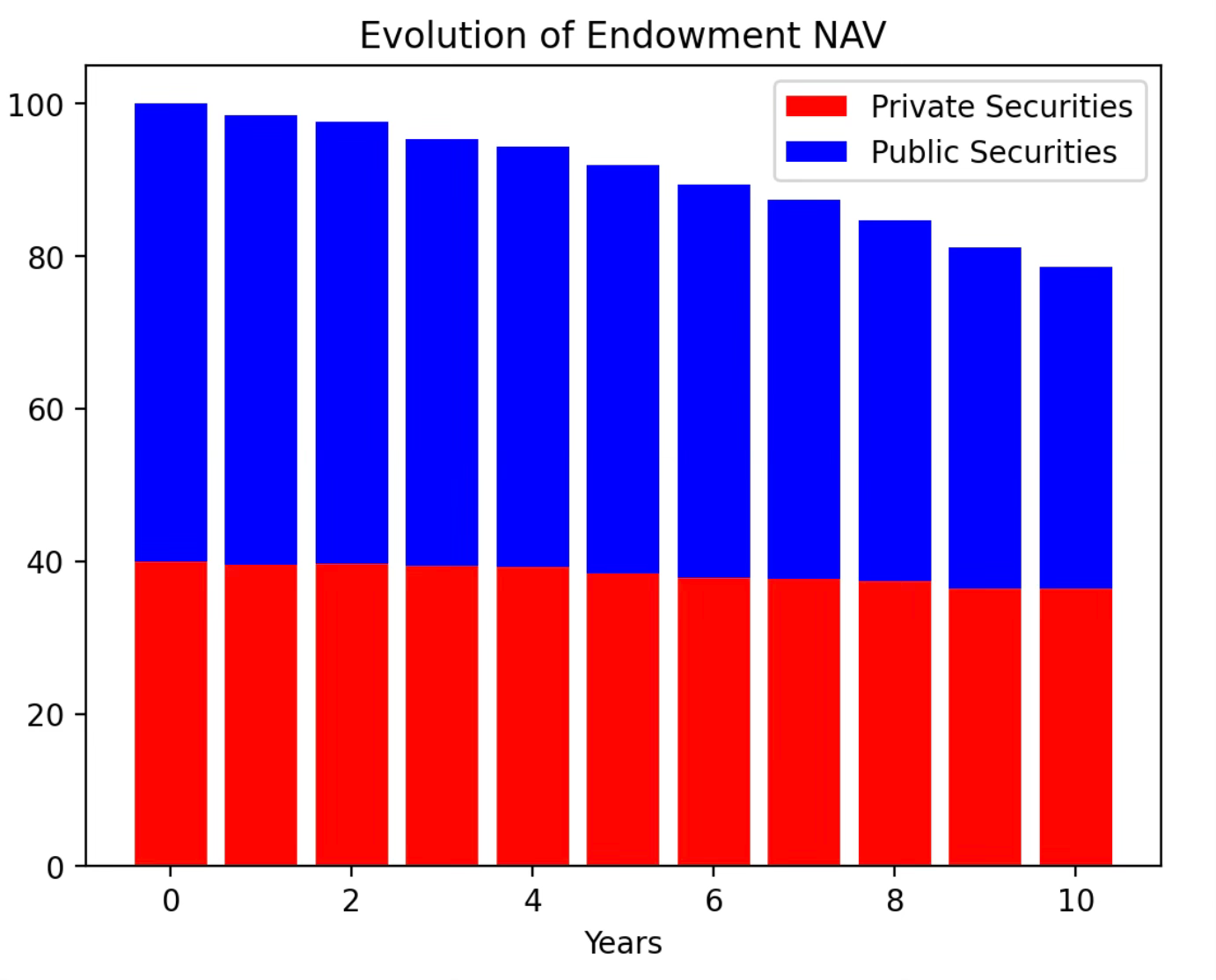

I built a simulator app (link below) so you can model it out with your own assumptions.

But here is what happens with the following settings:

Time frame: 10 years

Simulation: 100 simulations using randomly generated investment returns (with mean and standard deviations indicated below).

Private assets allocation: 40% (PE + VC + RE + Infrastructure)

Private investment returns: 2%/year. Maybe it actually should be negative, but assume the PE firms will give you positive marks even if you can’t have your money. Note this asset class return includes real estate which is another reason 2% might be generous.

Private equity return standard deviation: 7%. This can definitely be higher, but assume PE funds are good at managing the marks.

Public Market returns: 5%. Assume 4-5% on cash and bonds and the same in public equities.

Public market return standard deviation: 5%. This is a mix of bonds and equities so let’s keep it low.

What % of the fund is paid to the university each year? 5%

Annual inflation of the payment: 2%. Assume the university can managed expenses slightly and only grow their budget by 2%, instead of the usual 5%.

How much of the university payment is out of private asset realisations? 20%. Assume some PE/VC sales which are used to pay the annual university contribution. Remaining 80% each year comes from selling equities, bonds and cash.

Year 10 NAV: 78.7

Year 10 PE Allocation: 46.2%

Annualised return -2.4%. A big difference from the 10%/yr of the past.

How I could be wrong: Maybe US pension funds increase their private asset allocations by another 5% which relieves the liquidity stress (new bag holders) and bails out the endowments. Maybe Middle East SWF’s invest more too. Maybe the PE investment managers are also good investors and offset any possible EV/EBITDA multiple contraction with good idea generation and underlying economic growth. In the end returns aren’t amazing, but still 5-10%/year.

Implications of an Endowment Train Smash

If you are an endowment try to not put more money into PE/VC, but I understand if it’s too late. Notify the finance department that they will need to cut costs and reassess financial aid packages. Let them know the problems are structural and will last 10 years at least. MIT has already done this. Maybe there is a superfluous new department which can be cut from the budget.

If you are a private equity fund manager try to get more money out of US pension funds, but that might be a struggle. Also do more sales trips to SWF’s in the Gulf. I heard ADIA is allocating more to PE (15% up from 12%). Convince them they need to go to 20%. Also grow your Asia business. Asia funds, Asia sales people, etc. The US market is tapped out. I know it’s not the US and seems small, but grow the Asia business over time.

For the rest of us, how do we make money?

Our value stocks are probably fine and we have the buybacks to protect us. Otherwise, it might be a slight negative if large institutional funds are selling down their public equity exposure, but then again they’ve already been doing this for years so maybe it doesn’t matter.

Endowments will also likely reduce their hedge fund exposure because it’s also liquid. This shouldn’t affect us much because hedge funds are super overweight tech (How Consensus is your hedge fund?) and don’t own value.

These headwinds in the US make me think international equities could be a relative out performer within public equities, especially China. Nobody is allocated to China, there is no overhang, they have savings, they are under allocated to equities, and there are inflows. This fits with our Cash Dragons trade and general positivity that Chinese markets will surprise positively (The #1 Trade).

Below is a link to the YWR Endowment Investment simulator app if you want to try your own assumptions. But please don’t put a negative return in for private equity.

That has never happened and would break the computer.