YWR: We need to talk about Barclays.

Disclosure: These are personal views only. These are not investment recommendations or advice. For that seek professional help.

We need to talk about Barclays. Boring Barclays.

One the one hand it looks like nothing’s changed.

For the last 6 year’s the Barclays share price has been bouncing around under £2/share.

Back in 2014 it used to trade at £2.5/share.

It seems like nothing has changed, but under the hood everything has changed.

The bank has cut 47,200 staff!

Exited 12 countries (Africa and Europe).

Run-off or sold £93bn in credit exposure (RWA’s).

Increased the Tier 1 ratio to almost 14%.

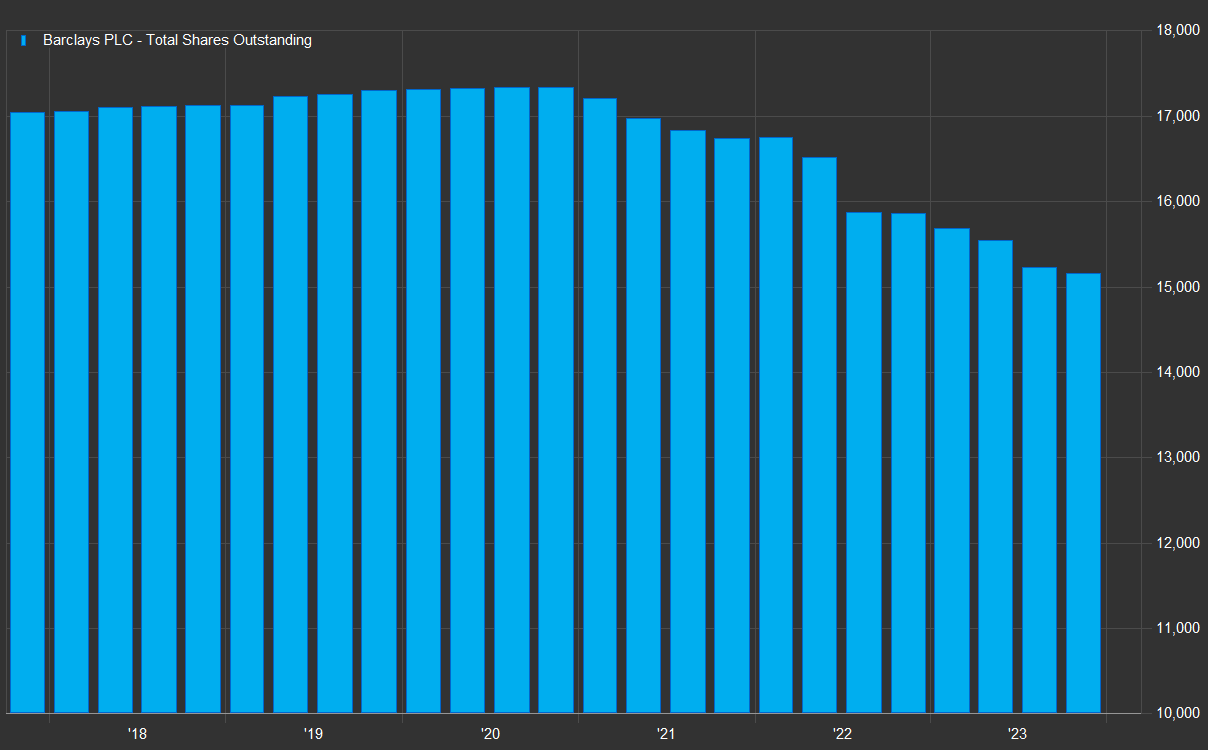

Bought back 2 billion shares.

And it shows in the financial results.

An ROE which used to bump around between 0 and 5%, has been 10% for 3 years in a row.

Capital returns of are now routinely £2-3bn/year with management guidance to return £10 billion over 2024-2026 (£3.3bn/year) and this could be the low end.

And yet…. despite a more consistent, higher ROE business which is funding buybacks, and a Tier 1 ratio close to 14% (ample/over capitalised), Barclays is trading at historic lows in terms of price to book.

It doesn’t seem right.

We first talked about Barclays back in October (£1.5/share) when everyone was worried Barclays would lose deposits, have massive loan losses and see falling interest margins.

We argued none of that would happen and actually Barclays (like other Banks in Europe) was at the start of a multi-year upturn in earnings and share prices (The Upside everyone is missing in European banks).

Unicredit, Santander and Commerzbank are moving, but Barclays and the other UK banks have lagged. This is the opportunity.

The Path to £3/share (+70%) and beyond.

Here are the catalysts.

Upgrades to earnings forecasts. They are too low.

Rebound in investment banking revenues after 2 year downturn.

UK driven profitable growth strategy

Share buybacks.

Share price rerates to £3/share or 7x 2025 earnings and 0.7x book.

Earnings estimate are too low

The sell side EPS estimate of 31p for 2024 looks too low. I’m at 38p. For 2025 the street is at 38p and I’m at 44p.

Note, in 2023 ex £927mn in Q4 restructuring costs the bank earned 32p/share, which was a positive surprise. So the sell side is implying no growth in 2024.

The sell side was positively surprised by the stable net interest margin in Q4. CFO Anna Cross had been guiding for a decline. That’s one of the reasons the stock popped on the results. Anna had to apologise during the call that she had been too negative in her guidance. Pricing pressure on deposits wasn’t as bad as they anticipated. I expect this pattern of positive net interest income surprises will repeat itself in 2024.

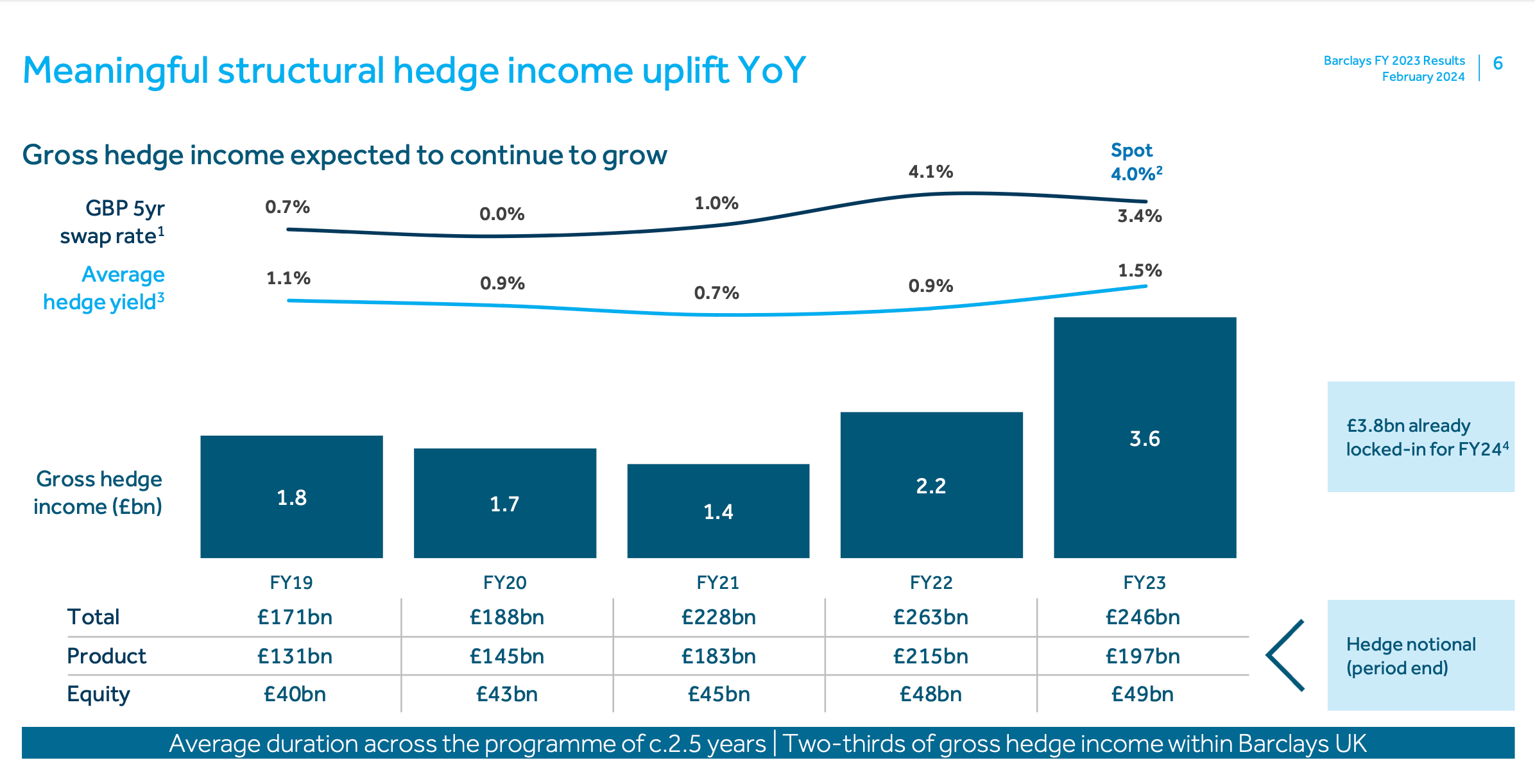

I forecast net interest income will be higher than £12.7bn (2023) as the £246 billion hedge book continues to reprice from 1.5% to 3.5-4%. My view is deposit pricing pressure is basically done. Those that have moved have moved. I’m also more optimistic on asset growth and think the bank can grow assets 4% (vs 0% guidance).

Full disclosure, my estimates for net interest income have declined from what I was expecting 5 months ago, but I am still far ahead of consensus. Reality is turning out to be somewhere in the middle.

On the other hand it appears we are all being overly conservative on credit costs, which so far have been the dog which didn’t bark. I have forecast the loan loss charge to increase in 2024 from 50bps to 60bps, despite the fact 2023 included a large $1.8bn provision to build reserves in the US credit card book. This 60bps estimate gives Barclays room for continued large charges in US credit cards (but down from 2023) with room for a pick up in losses in the UK. However, I can also see why loan losses might be down year on year if the UK remains as it is. This gives us a potential cushion in case I am being too positive on net interest income.

Investment banking rebound

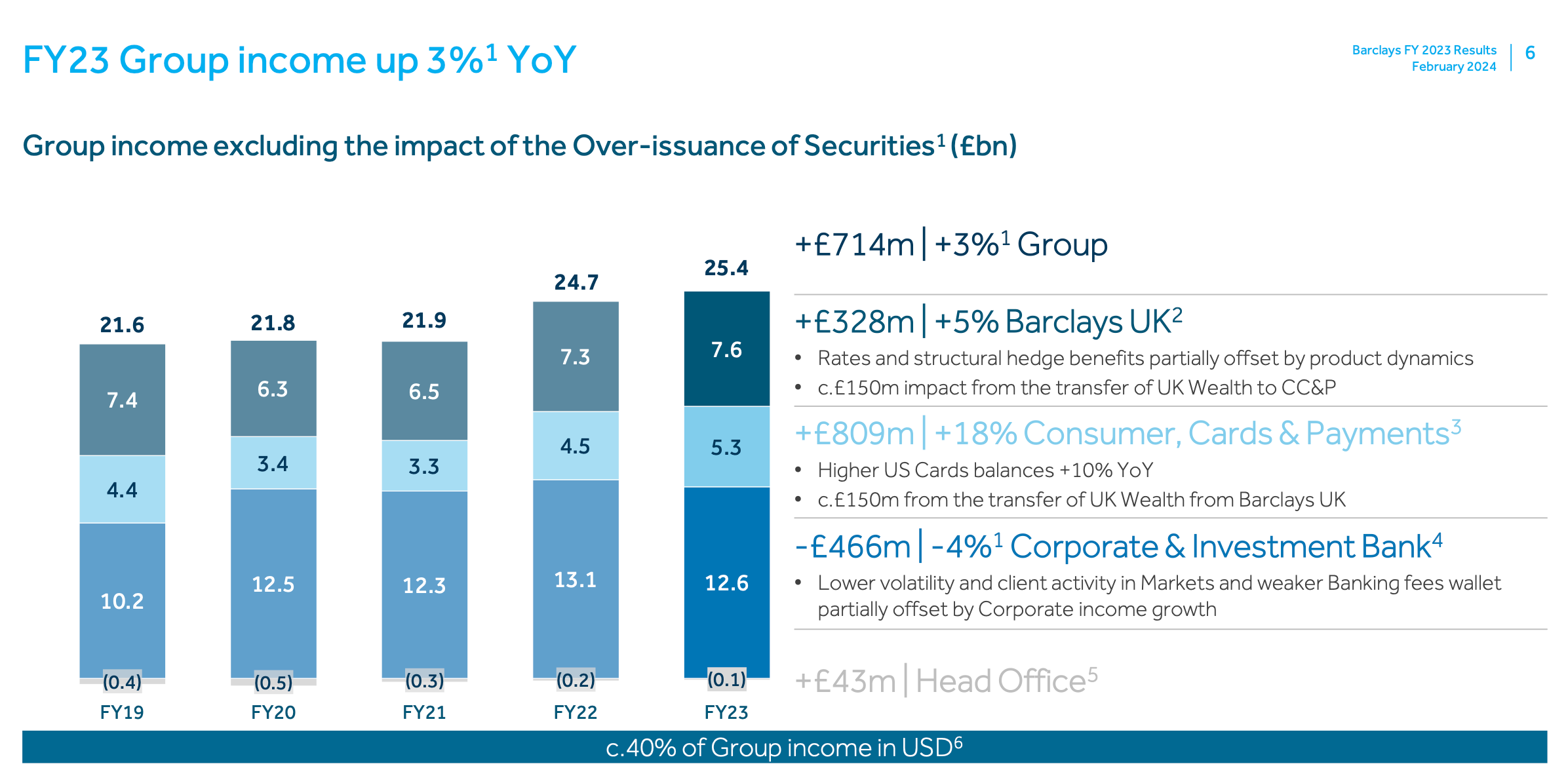

Another kicker for Barclays will be a rebound in investment banking fees. Corporate & Investment banking is 50% of revenues and declined 4% yoy in 2023. It was a drag on the group and part of the reason Barclays didn’t perform well last year (along with the CFO giving crappy guidance that turned out to be wrong).

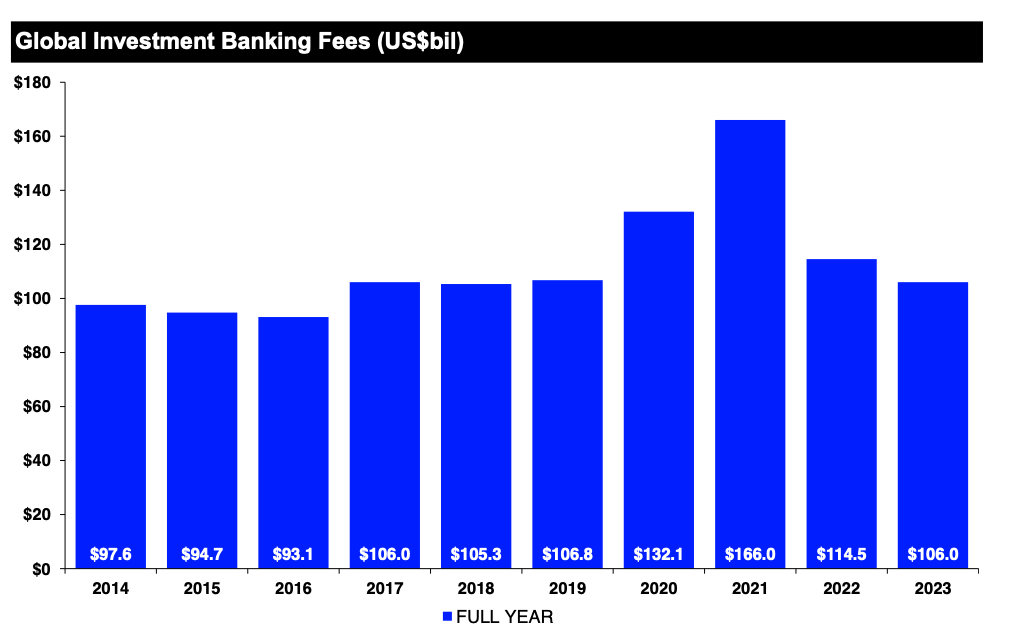

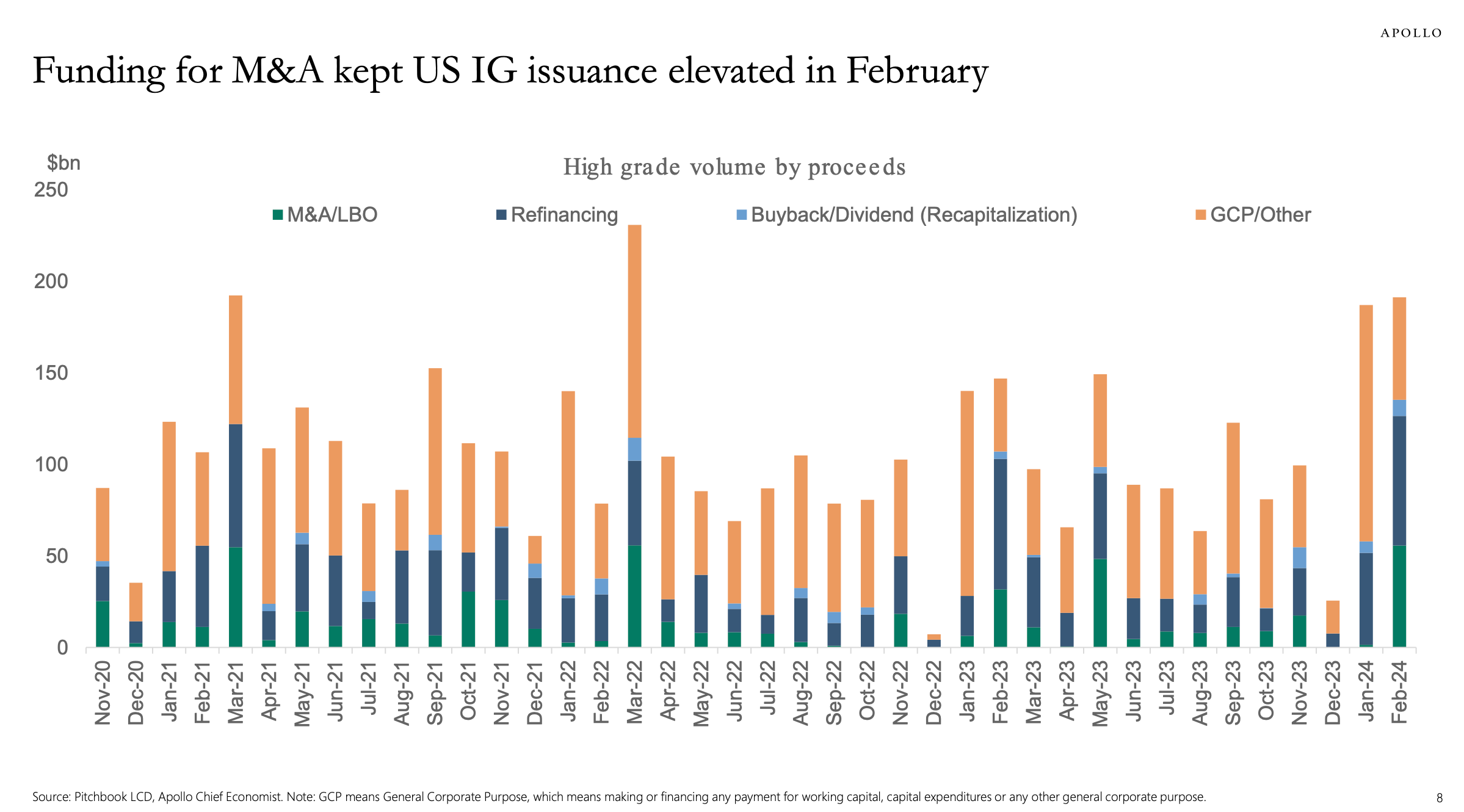

Investment banking fees are on the lows, but 2024 could surprise positively. There is a lot of high yield debt which needs to be refinanced. Issuers have been waiting for the predicted drop in yields, but maybe the view will shift. Issuers will see yields aren’t going down and realise they better act now to take advantage of low credit spreads. We could also see a pick up in M&A and IPO’s. I’ve put in 4% fee and commission growth for the group in 2024 which I think is conservative. Another cushion for our numbers.

It’s just 2 months so far ,but 2024 is off to a strong start for M&A and IG issuance.

More of a focus on the UK where ROE’s are higher

The new strategy is a continuation of what Barclays has been doing since 2014 (without realising it). The are refocusing more and more back to the UK where they are dominant and profitable. They will sell the Italian mortgage business and the German consumer finance business and buy Tesco’s retail bank in the UK.

Management likes the BarCap business and think it is at scale in fixed income. Now they need to grow it profitably with more emphasis on recurring financing income.

Barclays are also building out a specialty in US credit cards. The book is up to £32bn. Growing US cards is fine with me. Barclays has been in the credit card business forever with Barclaycard and managed it well.

All of this leads to a more consistent business, with less volatility and higher ROE’s. Which is why Venkat can stand up and promise to return £10bn in dividends and share buybacks through 2026 At the time of the announcement it was almost 50% of the market cap (current MCAP is £26bn).

Boring but Good.

I know this is a boring UK bank. It isn’t AI, and it isn’t semi-conductors, but it’s a money machine generating over £5bn/year in profits with minimal balance sheet growth, which means they have to return it to you.

The biggest challenge is you need to sit and do nothing for 2 years owning a UK bank while exciting things are happening all around you. It’s the same thing I said about Commerzbank. The hardest thing will be to do nothing (Commerzbank’s cash flow pile up).

So close your eyes and imagine it is March 2026. CFO Anna Cross gets up to the podium to announce Barclays has just reported full year earnings. The bank has earned over 40p/share in 2025 and is on track to 50p/share of earnings in 2026. Despite £1.5bn of share buybacks every year (3 years consecutively) the book value per share continues to climb and is now £4.7. The ROE on that book value is up to 9.7% (on stated equity, not tangible equity).

The analysts at Morgan Stanley, Goldman and UBS still think Barclays is boring, but begrudgingly they will accept that Barclays has improved a lot and deserves to trade at £3/share or 7x 2025 earnings.

You are happy, and glad you were patient. You know the bull case isn’t over and the next stop is £4/share maybe even £5 (10x earnings). In 2024 and 2025 you reinvested the dividends to accumulate even more shares.